Yesterday’s start for the week was slightly subdued as many nations in Europe enjoyed a long holiday weekend. In Forex the past few weeks the USD has taken on a weaker stance and this was reiterated by last Wednesday’s slightly lower U.S Consumer Price Index results. The outlook of investors and financial institutions has once again shifted and a more dovish U.S Federal Reserve is being anticipated for the moment.

However, while inflation data from the U.S did come in with lower marks via the CPI report last week, it should be remembered the PPI actually came in higher. While there is a natural instinct to always be optimistic, the prudent fact is that risk management remains important. A glance into the looking glass via the USD/JPY shows that all is not calm in the world of Forex.

However, if people want to look at the knock-on positive influence of the weaker USD, they can glance at the USD/ZAR which is near important mid-term lows. South Africa will be conducting their national election next week on the 29th of May, which is likely to cause some nervousness for the currency pair. Even though South Africa continues to suffer from a struggling economy caused by questionable government policy and faltering infrastructure, the USD/ZAR is experiencing solid bearish behavior. However, risks certainly remain for the South African Rand and at its current values, some financial institutions may view the currency pair suspiciously.

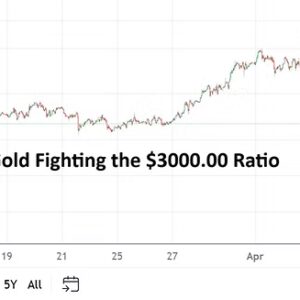

Gold remains within sight of record values achieved yesterday when the 2,440.00 USD plus levels were touched. The shift in behavioral sentiment towards risk appetite and a weaker USD centric attitude seemingly geared towards dovish Fed mid-term perspectives have helped the precious metal. Day traders should remain cautious with Gold and while the technical trend is enticing, it will be good to remember too much leverage coupled with blind betting can be dangerous. A clear warning sign that speculative zeal is high in Gold is that the current price of the commodity is 30.00 USD lower for the moment compared to yesterday’s highs. Price velocity can prove costly when a daily reversals goes against wished upon directions.

U.S equity indices and their ability to fight toward new highs is a clear sign risk appetite via outlooks within financial institutions and from investors remain strong. U.S Treasury yields should be monitored and if they continue to erode this will fuel optimism. One additional note for traders this coming week is that Memorial Day will be observed in the U.S next Monday, meaning there may be more impetus for some to buy U.S equity indices now instead of waiting out a long holiday weekend and coming back to markets which have gained. Yes, Fear of Missing Out could be a factor.

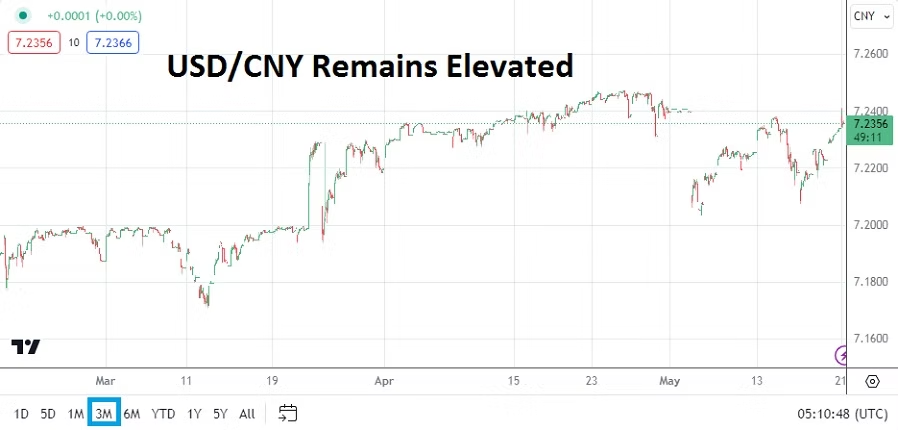

Monday, 20th of May, China Loan Rates – while banks kept their 1 and 5 year Prime Rates in place per the reports yesterday. Last Friday’s Retail Sales figures came in weaker than anticipated, and New Home Prices produced another decline. Industrial Production numbers were however stronger than expected before going into last weekend. China remains in a difficult position economically and the USD/CNY should remain observed because it is elevated.

Tuesday, 21st of May, Canada Consumer Price Index – inflation numbers from Canada will be watched carefully. The results will impact the USD/CAD certainly, but unless there is a surprise result which misses estimates wildly, the currency pair should return to a USD centric mode rather quickly.

Wednesday, 22nd of May, U.S Federal Reserve FOMC Meeting Minutes – while this report is not read by many people, and the Federal Reserve will have taken a cautious rhetorical tone, the report may offer some tidbits for consideration. However, the reality is that U.S economic data has been a mess for the past few months. GDP showed signs of decreasing last month, but the multi trillion dollar question is if inflation is now under control. Folks looking for answers will not find them in the Fed notes. They will have to wait like everyone else for more data in the weeks and months to come.

Thursday, 23rd of May, European Flash Manufacturing and Services PMI – the Purchasing Managers Index reports from European Union members and the U.K are anticipated to show signs of some improvement mostly. The U.S will also be publishing its reports, although the Services report from the States is expected to be slightly weaker. Investors will react to all of this data. Positive readings from E.U and U.K would likely have a positive influence on the EUR/USD and GBP/USD for bullish speculators.

Friday, 24th of May, U.K Retail Sales – consumer spending is anticipated to show a decline. However, the last Gross Domestic Product report from the U.K was stronger than anticipated. While the Retail Sales data is important for the GBP/USD, as long as the outcome meets expectations or comes in slightly stronger than estimated the currency pair could retain technical value.

Friday, 24th of May, U.S Revised Consumer Sentiment and Inflation Expectations – the University of Michigan numbers for sentiment came in weaker than expected last month. The anticipated outcome is slightly better for this report. However, the inflation numbers should be watched carefully via the U. of Michigan statistics. The tick higher in recent reports regarding where prices are expected to go by consumers is troubling for the prospects of the U.S economy.

If American consumers are not confident they will spend less. Yet, within the strange world of economic data and policy consisting of lagging and forward looking numbers, if consumers feel less optimistic this means the U.S Federal Reserve will be pushed to consider cutting the Federal Funds Rate, unless inflation actually does remain elevated. And again, traders should remember that a long U.S holiday weekend might add to the rather electric financial markets.