New Year's Thought on AUD/USD Potential Intervention by RBA

AUD/USD One Year Chart as of 1st January 2025

1 year chart of AUDUSD showing decline and lows as rumors swirl about the Reserve Bank of Australia contemplating intervention due to weak Australian Dollar.

AUD/USD and AMT thoughts: Australia’s govt is led by the Labor party which is socialist based, so it would be no surprise if they and the Reserve Bank of Australia believe (wrongly) they can intervene to help the strength of the AUD, when actually they should work on improving the fundamentals of their economy with solid fiscal policy. But being socialists they don’t know how to do that. Labor is going to lose big in the next Australian federal government election.

Cautious Trading as Key Data and Outlooks Await Impetus

The start of trading this week could prove to be slightly adventurous for speculators as financial institutions return to the markets and start to take positions for their clients. Having survived the past two and a half weeks of holiday season trading, market action will now focus on immediate, mid and long-term goals and outlooks depending on time frames and targets. Slightly nervous trading was on display last week, but some traders may believe their is plenty of room for more optimism and may be suspicious of the results delivered.

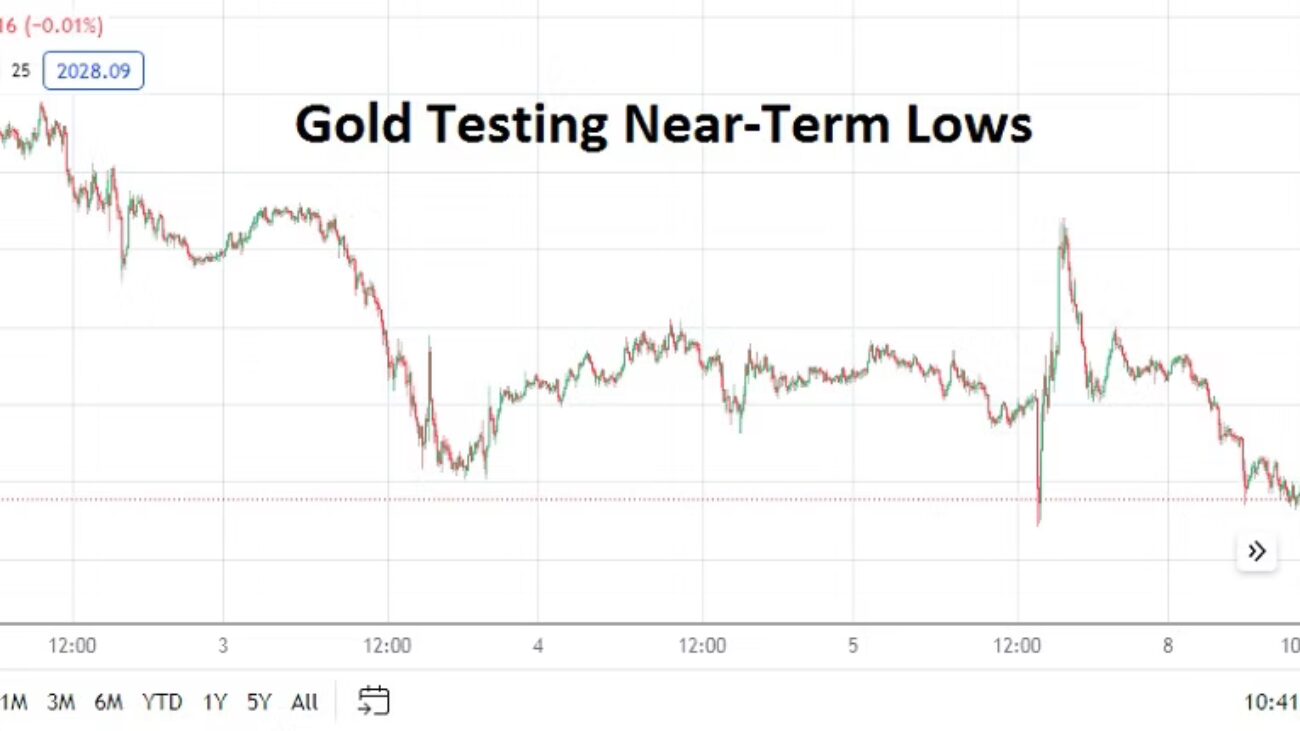

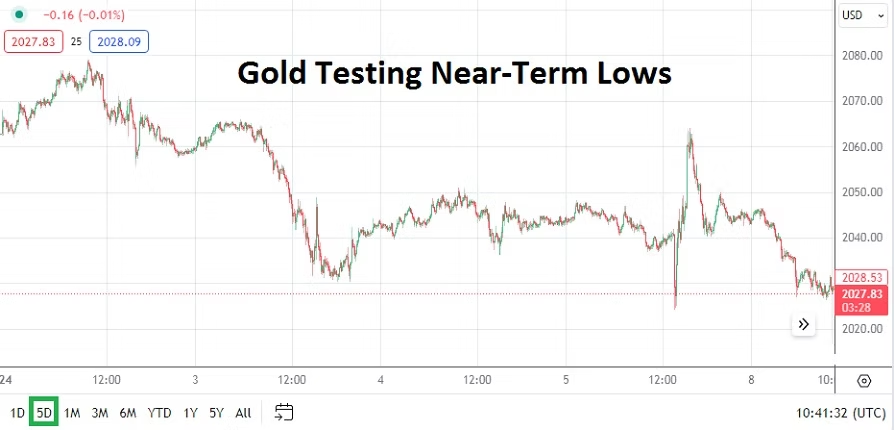

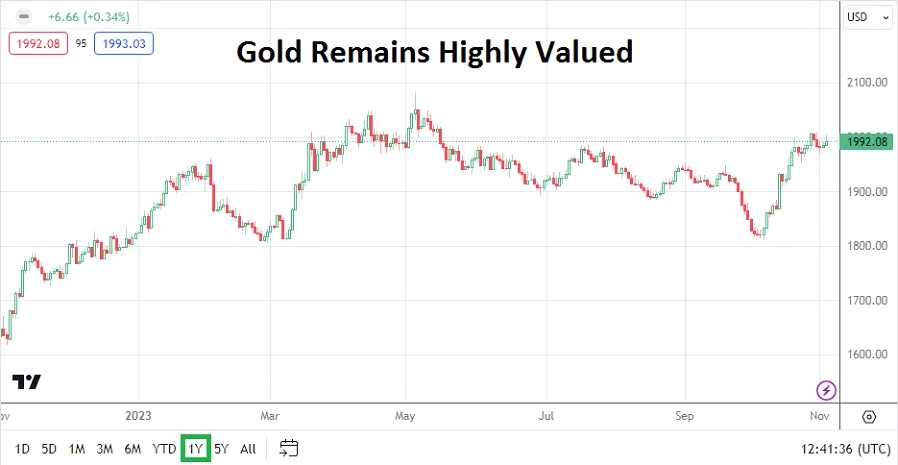

Gold Five Day Chart as of 8th of January 2024

Day traders should look at some barometers before they participate in the near-term. Gold has come off highs seen late last week, but remains within the higher elements of its six month price range. Its selloff from apex values last week perhaps correlates to U.S equities and USD turbulence which has also been experienced.

Last Friday’s reaction to the U.S jobs numbers was fascinating. The numbers delivered an initial shock to folks who wanted to react quickly. Hiring the last month increased more than expected, which might have caused the momentary bullish surge in the USD. Only to be confronted swiftly by further investigation of the jobs data which showed previous months statistics had been revised downwards. This acknowledgement set off selling of the USD and technical whipsaw results.

Day traders participating in Forex this past Friday likely experienced a range of emotions. If the market correlations are correct regarding the USD and the reactions seen, trading in gold also seemed to mirror the price action. Interestingly, gold touched a low of nearly 2024.00 USD on Friday in the wake of the jobs report, surged higher to around 2064.00 and then reversed lower again.

The notion that gold is trading within sight of Friday’s lows is interesting for both the precious metal and trying to understand where USD sentiment will lean early this week.

Behavioral sentiment remains rather optimistic, however nervous headlines during the holiday season may have caused cautious shadows to grow darker, particularly as light trading volumes affected results. Today and tomorrow will prove interesting in the broad markets, this as financial institutions return in full and as they brace for U.S inflation numbers later this week.

S&P 500 One Month Chart as of 8th of January 2024

Nervous short term trading is likely today and tomorrow as price equilibrium is sought. U.S equity indices have backed away slightly from their flirtations with all-time highs, but even as selling developed the past week highs are still in sight and are likely still being dreamed about by many institutions. U.S Treasury yields will also be a good indicator for Forex traders early this week regarding how comfortable financial institutions are with their current outlooks.

Monday, 8th of January, Germany Factory Orders – a slight gain of 0.3% was reported today, which was below the 1.1% expectation. The German economy is starting to show signs of economic growth, but has major hurdles to still climb. The lackluster German numbers may keep the ECB in a rather neutral stance for the mid-term. Which might help a bullish EUR/USD outlook if the U.S Fed is seen as the first major central bank which will have to cut interest rates.

AUD/USD Three Month Chart as of 8th January 2024

Tuesday, 9th of January, Australia Retail Sales – the anticipated climb of 1.2% is significantly higher than the negative -0.3% result from last month. A good outcome via the Retail Sales could help the Australian Dollar reignite some positive momentum. CPI data will come from Australia on Wednesday, which will certainly affect the AUD/USD too.

Wednesday, 10th of January, U.S Ten-Year Bond Auction – though day traders may not be too involved regarding the sale of U.S Treasuries, the results from the auction will have an affect on Forex. U.S Treasury yields should be monitored.

Thursday, 11th of January, U.S Consumer Price Index – a slew of CPI results will get the attention of financial institutions. The inflation data is expected to show a slight decrease in the Core CPI result, but show a slight gain in the broad number. This will likely be the most heavily traded day since the third week of December. There will be a reaction from the inflation reports. If the numbers come in around the estimates this may help the bearish mid-term outlooks for the USD. If the results are shockingly stronger, the USD would turn bullish. Day traders need to be careful in the midst of the Consumer Price Index publications because volatility is expected.

Friday, 12th of January, China CPI – a decrease is expected from the Asian giant. Deflationary concerns are shadowing China’s economy. The expected number of minus -0.4% would actually be an improvement compared to the last reading which was minus -0.5%. The USD/CNY has been rumored to have been experiencing some ‘hands on’ management from China. Investors continue to be nervous about China’s economic outlook and would like to see signs of improvement.

Friday, 12th of January, U.K Gross Domestic Product – a gain of 0.2% is being anticipated. Any growth from the U.K GDP would be welcomed considering the recessionary data which has been lingering. The GBP/USD will react to the results and bullish momentum in the currency pair could be sparked by a better than anticipated number.

To Risk or Not to Risk that is the Speculative Question

Last week U.S equity indices demonstrated a rise in value. The highs achieved in the Dow Jones Industrial Average, the NASDAQ Composite and the S&P 500 by the end of last week only touched values seen in the middle of October. And while their ratios remain below the highs of early August and falling values seen in September, the move upwards was certainly welcome by financial institutions and day traders who hold optimistic viewpoints.

U.S Treasury yields declined last week. While incremental decreases were made through Thursday, the U.S Non-Farm Employment Change and Average Hourly Earnings reports both coming in below expectations on Friday, created a stronger dose of lower yields. The 5, 7, 10 and 30 year U.S Treasuries are now trading near mid-September values. The 2 and 3 year notes are moving around early September numbers.

Gold One Year Chart as of the 5th November 2023

The USD grew weaker in slight movements against many major currencies last week, but upon the weaker jobs numbers found increased selling price velocity. Gold however remains suspiciously strong, which brings up the notion that risk adverse ‘insurance’ is still being held closely by investors who remain nervous.

The Middle East crisis is ongoing in Israel against Hamas and to a limited extent Hezbullah, but financial institutions have seemingly been able to digest the news and remain tranquil and vigilant. Another sign of calm coming into the global financial markets is the price of WTI Crude Oil which finished the week under 81.00 USD per barrel.

Economic data will be relatively light this coming week, and behavioral sentiment appears to be the potential larger factor until Friday regarding impetus for day traders and financial houses. Certainly loud global developing news could suddenly erupt and cause nervous investors to falter, but last week’s trading results showed signs of improving risk appetite.

The U.S Federal Reserve met expectations last Wednesday and didn’t raise the cost of borrowing. The mid-term seems to indicate interest rates will remain high, but that the U.S central bank will not raise the Federal Funds Rate anytime soon. The lower than expected inflation report via the Average Hourly Earnings before going into the weekend helped highlight this thinking, although it remains a consideration that is still speculative.

Officials from the major central banks including the BoJ, BoE and Fed will be speaking this week and could cause turbulence with their rhetoric. However, no major surprises will likely come from their mouths. Although the Bank of Japan may rattle the prospects of intervention to keep USD/JPY traders on their toes.

Monday, the 6th of November, Germany Factory Orders – the result is expected to be negative and highlight the nation remains within recessionary conditions. The Sentix Investor Confidence reading will also be released slightly afterwards for the European Union and a worse number than last month’s outcome is anticipated. But the EUR/USD is likely to remain mostly USD centric, even though these reports could cause momentary fluctuations.

AUD/USD Six Month Chart as of the 5th November 2023

Tuesday, the 7th of November, Australia Cash Rate – the Reserve Bank of Australia is expected to raise its interest rate by 0.25% to 4.35%. Will the RBA take a gamble and not raise the interest rate due to other major central banks holding their rates in place, or will the increase go ahead to fight stubborn inflation while trying inspire some confidence in the AUD? A hike seems to be the direction the RBA will decide upon, having said that, the Australian central bank have surprised financial institutions before.

Wednesday, the 8th of November, U.S 10-year Bond Auction – the results from this sale and the yields that develop within U.S Treasuries will have an affect on Forex. Lower yields than anticipated could signal a weaker USD. However, risk adverse elements will need to be calm for the bond auction to produce tranquil results.

Thursday, the 9th of November, China CPI and PPI – the data from these inflation reports will be watched closely. Chinese economic numbers has shown some signs of stabilization the past few weeks, both of these publications are expected to have negative outcomes. Concerns about the financial pressures domestic consumers are facing regarding housing market values in China and the way in which they spend due to lackluster prospects are concerning. The USD/CNY will be affected in the wake of these statistics, and the USD/SGD could see momentary volatility too if the results prove to be a surprise.

GBP/USD One Month Chart as of the 5th of November 2023

Friday, the 10th of November, U.K Gross Domestic Product – last month’s number came in with an unexpected positive gain of 0.2%, this GDP report is anticipated to show no change. The GBP/USD jumped in value on Friday and financial institutions will be geared towards behavioral sentiment most of this week, but the British GDP data could cause a reaction before going into the weekend.

Friday, the 10th of November, U.S Preliminary Consumer Sentiment via the University of Michigan – the reading is expected to be slightly below last month’s outcome. U.S consumers remain a strong point of light for the U.S Federal Reserve. American consumers have remained spenders, although they have seemingly curtailed purchases of large ticket items such as cars and big appliances. If this data comes in weaker than expected it could propel more selling of the USD. A stronger number than anticipated could spook financial institutions and cause a slight surge in buying of the USD.

Nervous Outlooks and Short Term Fixes Creating Anxiousness

A U.S government shutdown has been avoided, but the resolution highlights that an important year of political games is getting fully underway in Washington. Short term fixes via congressional agreements do not hide the fact the U.S government continues to bleed money and is adding to its deficit as yields on U.S Treasuries remain high.

Gold Five Day Chart as of 2nd October 2023

The price of gold has sank substantially in the past week, which shows the USD continues to be strong, and that speculative short-term games within the precious metal must always be kept in mind by day traders. Long term fundamental beliefs regarding the value of gold cannot stop momentary volatility.

GDP results from the U.S last week came in slightly below estimates, but the ability to still sustain growth also creates the suspicion the U.S economy remains stubbornly strong, which effectively puts the U.S Federal Reserve in a rather difficult place. Crude Oil prices have remained high, and this week’s coming jobs data will be important for short and mid-term market participants as they position themselves while nervous behavioral sentiment continues to be evident.

U.S stock markets are near three month lows and trading conditions choppy, this as yields on U.S Treasuries are elevated and create a tough road for speculators to navigate in the short-term.

Monday, 2nd of October, U.S ISM Manufacturing PMI – a reading below 50 is anticipated which would mean sentiment remains negative regarding the U.S economy, but Core Durable Goods Orders came in better than expected last week. Thus, the result of this manufacturing report could play into short and near-term USD trading and cause a ripple as financial houses anticipate the jobs numbers later this week.

Tuesday, 3rd of October, Reserve Bank of Australia – the RBA is expected to keep its Cash Rate in place. If the RBA cooperates with financial institutions and does not change its key borrowing rate , the RBA Rate Statement will come into focus. However, the AUD/USD is still within the shadows of U.S Federal Reserve like most other major currencies.

Wednesday, 4th of October, U.S ISM Services PMI – the outcome from the Services report is expected to fall below last month’s outcome. The slight miss in the GDP numbers last week was noteworthy, but the better than expected Core Durable Goods results will make this report of interest and provide a bit of impetus to the USD and U.S indices before Friday’s key jobs data – particularly if the Services reading is better than anticipated.

GBP/USD Three Month Chart as of 2nd Oct. 2023

Thursday, 5th of October, U.K Construction PMI – while not considered a major publication by many analysts, the ordering by purchasing managers in Britain may prove relevant as an indicator regarding outlook. The Bank of England held their interest rates in place a couple of weeks ago and this was based on the belief the U.K economy is slowing. The Construction PMI report is expected to come in slightly below last month’s outcome which could set the table for slight choppiness in the GBP/USD which has continued to trend lower.

Friday, 6th of October, U.S Non-Farm Employment Change and Average Hourly Earnings – the combination of these two reports will impact USD trading before their publication and afterwards for several hours. Financial institutions will examine these statistics carefully. If there is a hint of weakness in the U.S jobs market and wage inflation is tame, this could make the USD weaker. However, if jobs hiring remains firm and there is a slight uptick in the costs employers are having to pay workers, the USD could get stronger.

Lack of Big U.S Data this Week but Fed Officials to be Heard

There will be an absence of large trading volume in many markets today, because of the U.S and Canada Labor Day holiday celebrations. Results from forex markets should be considered with a healthy dose of skepticism by day traders. If you choose to participate today, using entry price orders may protect you against the possibility of price volatility due to quiet markets having the ability to create sudden jolts.

Day traders are advised to be on the lookout for potential surges to develop on Tuesday. U.S financial institutions returning to the markets in full could possibly react to economic data from the States that they may not have acted upon yet, this as outlooks may have been reconsidered over the Labor Day weekend. Equities and indices, U.S Treasuries, and gold should get plenty of attention this week as summer trading comes to an end.

EUR/USD Three Months Chart as of 4th Sept. 2023

Monday, 4th of September, E.U ECB President Christine Lagarde – the ECB chief will be speaking in London later today. The ECB President might get the attention of EUR/USD traders who may still be scratching their heads regarding last week’s decline in the EUR and trying to figure out why it happened.

AUD/USD Three Months Chart as of 4th Sept. 2023

Tuesday, 5th of September, Australia RBA Cash Rate – the Reserve Bank of Australia is expected to hold its ground and make no major changes to interest rate policy. The AUD/USD is trading at lows the RBA has acknowledged are troubling. However, there seems to be little the RBA can really do except to wait out the U.S Federal Reserve’s rhetoric to change. As a note, GDP numbers will come from Australia on Wednesday.

Wednesday, 6th of September, Canada BoC Overnight Rate – the Bank of Canada is expected to keep its interest rate policy steadfast without any changes. The USD/CAD could react momentarily to the Bank of Canada’s Rate Statement.

Thursday, 7th of September, China Trade Balance – economic statistics from China have been troubling over the mid-term and there is no reason to think they are suddenly going to turn optimistic. China is receiving plenty of negative attention from ‘Western’ analysts, but the concerns expressed could be legitimate. Slumping growth, real estates problems, and the shadow of deflation are issues in China.

Thursday, 7th of September, U.S Federal Reserve Officials – several high ranking members from the Fed will be speaking at various conferences across the States. Following the lackluster economic data published in the U.S the past couple of weeks, comments from the Federal Reserve members should be given attention to see if they begin to acknowledge interest rate policy should turn more dovish. USD traders will certainly have the ability to spark Forex on Thursday if rhetoric from the ‘officials’ starts to change tone.

Friday, 8th of September, Japan Final GDP – the Gross Domestic Product numbers could prove interesting for USD/JPY traders. Growth is expected to show a gain of 1.4%. The GDP Price Index results should be watched and are expected to match last month’s number with a gain of 3.4%.

Saturday, 9th of September, China CPI and PPI – the inflation numbers will be of interest to investors. These data reports could prove more important than the Trade Balance results released earlier in the week. The USD/CNY should be monitored in the wake of these inflation (deflation) results.