Paperwork Cyclones and Slow Pace Confront Indian Citizens and Corporate Investment

Almost every single day Indians are confronted by massive bureaucratic problems when they have to approach the government for basic services. When this will change?

For example if you apply for an Aadhaar card (which is used for proof of identity and address in India), birth certificate or ration card (used primarily for getting subsidized groceries in government run stores), or want an electricity connection or passport, you have to move through a myriad of unnecessary bureaucracy in many government offices.

Recently, I went to renew my passport which was authorized and overseen in a regional passport office in Tiruchirappalli of the Tamil Nadu State. To my astonishment, there were no single chairs or any other type of sitting amenities for visitors carrying their applications. Visitors had to sit down on the floor outside the passport office.

India Insider: A Giant Bureaucracy Needs an Urgent Reset

Also applicants inside the premises had no access to office drinking water or restroom facilities. And the waiting hours were too long. The authorities there treat people like teachers treating students, making normal people wonder why they have to apply for their passports by undergoing this giant bureaucracy as if it were a psychology test of some sort. Many people pour their anger and frustrations onto online forums complaining about the mistreatment.

Some of these people likely wondered how India despite showcasing it can send satellites to space and the Chandrayaan to the moon, doesn’t seem to have a stable, nor easier services for the day to day needs of the people regarding government affairs.

The government may argue that due to large numbers of people constantly applying for various forms and certificates, and a lack of adequate staff, things are more than a little complex in many overburdened government departments. But the fact the government seems to miss and a critical point people are driven to anger about, is that the nation collect taxes from its citizens to insure adequate services which are not fulfilled comfortably in most cases.

Indian citizens are not applying empty handed for a passport and expecting charity or miracles from the government, rather they pay an accepted fee to the passport office. Thus, it’s the duty of the government bureaucracies to be held accountable.

In government run local panchayats (rural government assemblies), there is always rampant corruption. An example can be given regarding the simple renewing of a business license. Corruption is a common thing. Vishalini (name changed) told me that she had to pay a 5000 Rupees fee ($51 USD) in 2019 in order to bribe a local panchayat to get her father’s death certificate

Imagine what would happen if some officers from the government or its employees, went to a restaurant and they were treated badly and charged $20 instead of $2 for a Dosa or Vada Pav. Would they silently pay the bill with cash not resisting, or would they fight back and ask questions?

As a former Forex broker working in the Indian financial markets and servicing retail clients, I have witnessed how this bureaucracy has worked. In April 2024, the authorities simply banned the exchange traded currency derivatives market that allowed retail speculators, small scale exporters and importers to hedge their exposure, wagering on the direction of the Rupee against 4 currencies – the EUR, GBP, Yen and USD. Many clients lost money, because they couldn’t sell at the available market price and some of the trades were liquidated by brokers’ risk management systems when the directive was put into force. The authorities neither compensated, nor took responsibility for these actions. The government action was decisive and swift.

Almost everyone in India knows that we have ‘missed the boat’ by making small manufacturing detrimentally hard due to red tape, poor infrastructure and giant bureaucracy. Free enterprise and entrepreneurship create innovation, less government intervention and greater economic freedom could allow small scale manufacturing to flourish.

Not Only Indian Citizens Suffer, So Do Investors

India has huge gaps to fill, but even if someone injects capital for an infrastructure project, makes money, and is creating jobs, there are still many things to be done about the burden of bureaucracy. The results of government inefficiency and corruption also creates hurdles and disadvantages for investors who would like to participate in India’s growth story with much needed foreign money.

India’s enormous bureaucracy needs urgent improvement and progress in order to facilitate and revitalize its approval system to receive Aadhaar cards, marriage certificates and even death certificate in a more timely manner. Everything can and should be digitized, so people don’t have to wait in long cues to verify or get new documents.

A lack of effective and transparent services in government offices have to be dealt with effectively. Standards need to be created, upheld and checked on regularly, a host of problems need to be eradicated. Indian citizens would benefit.

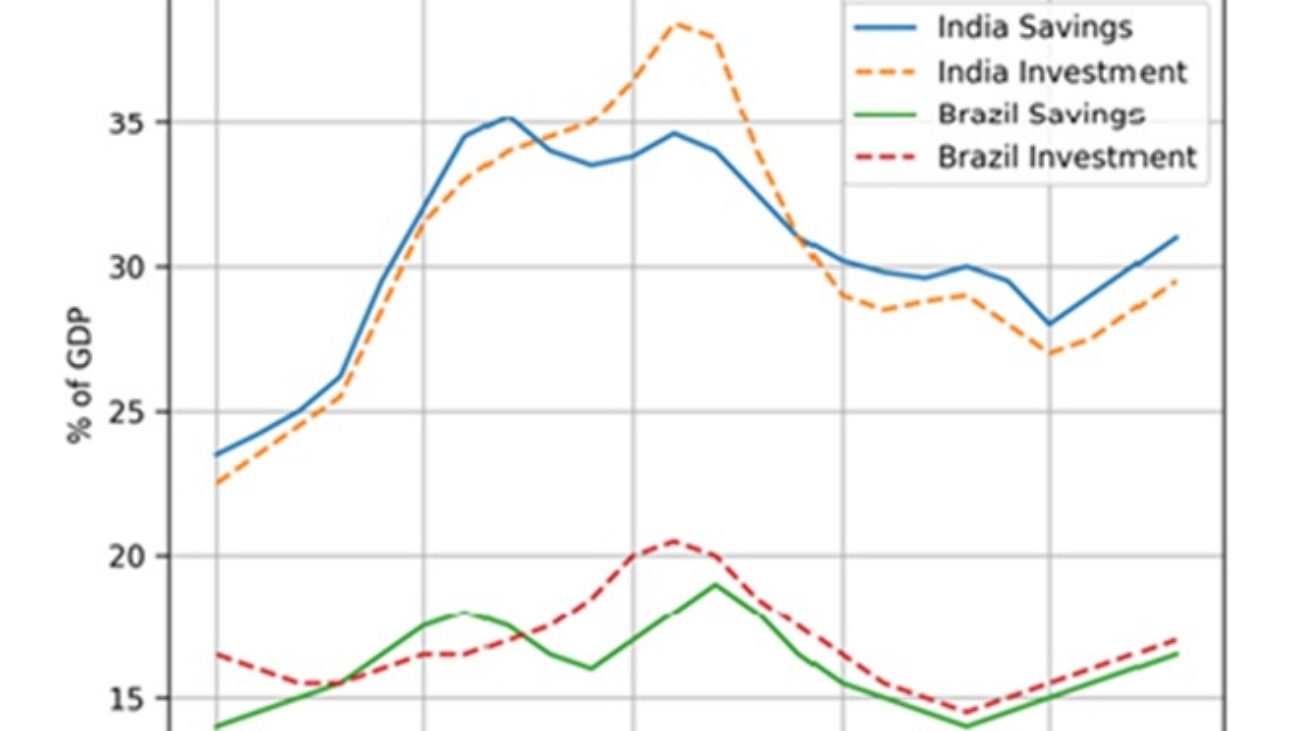

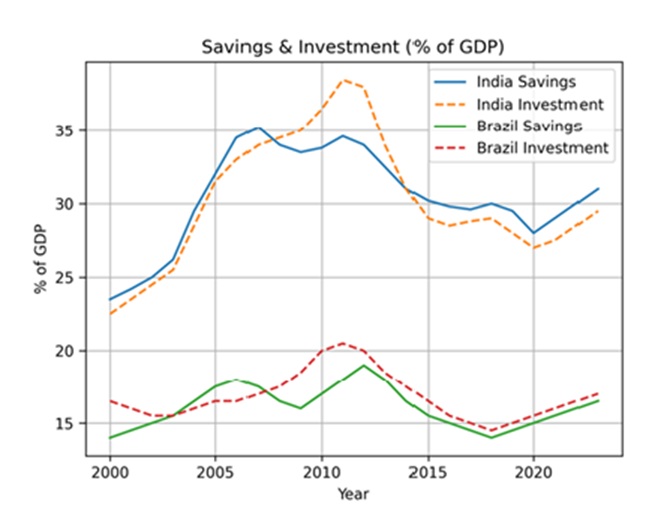

India is a current account deficit country and it needs foreign direct capital to help finance its deficit. Investment opportunities need to be made easier for financial institutions abroad to facilitate capital inflows into India so it is less reliant on its own domestic borrowing and savings. Weak frameworks and institutional voids create problems. For India to reverse the weakened foreign direct investment being demonstrated and attract meaningful capital, fundamental changes need to take place, we cannot rely on mere hope for more favorable diversification cycles from abroad. With better policies implemented by the government, India can attract global investment funds easier and help foster improvements for all.