India Insider: Macro Stress a Capital Flow Problem, Not a Trade One

Editor’s note: This article was originally written in January 2026. It has been updated to incorporate developments through February 2026, including the U.S – India interim trade agreement and subsequent capital flow data.

India is currently experiencing what can best be described as macro stress. By macro stress, we mean pressure across the broader economy that shows up simultaneously in the currency, financial markets, and capital flows, rather than a problem limited to one sector or company. In India’s case, this stress is visible in a weak rupee, persistent foreign investor outflows, and rising concerns about equity valuations.

This stress is often misinterpreted as a trade or export problem. In reality, the pressure on the Rupee and the growing fragility in equity markets stem primarily from the capital account, not from collapsing exports or remittances. Even as the U.S Dollar softens – helped by Federal Reserve rate cuts and renewed trade tensions under U.S President Donald Trump, India continues to struggle to attract foreign capital, exposing a deeper structural imbalance.

Source: NSDL (FPI Equity Flows): Reuters and author’s calculations.

Recent weakness in the USD would normally support emerging market currencies and risk assets. This time, however, the response across emerging markets has been uneven. Capital has flowed toward economies linked to artificial intelligence, semiconductors, and commodities, as well as toward markets where valuations have already adjusted. South Korea, Hong Kong, Chile, and South Africa have all benefited from this rotation. India has not.

The Rupee’s weakness reflects this divergence. USD/INR continues to trade around ₹91.5–91.6 despite the absence of a sharp deterioration in India’s trade fundamentals. Services exports, particularly IT services, remain resilient, and remittances continue to provide a steady source of foreign exchange. This brings us to the current account.

The current account represents a country’s net trade balance with the rest of the world, including goods, services, and remittances. India runs a current account deficit, meaning it imports more than it exports. While this deficit persists, it is manageable at present, supported by stable services exports and remittance inflows.

The real problem lies in the capital account, which tracks investment flows such as foreign investors buying or selling Indian equities and bonds. When foreign capital flows into the country, it helps finance the current account deficit. When it flows out, pressure builds quickly on the currency and financial markets.

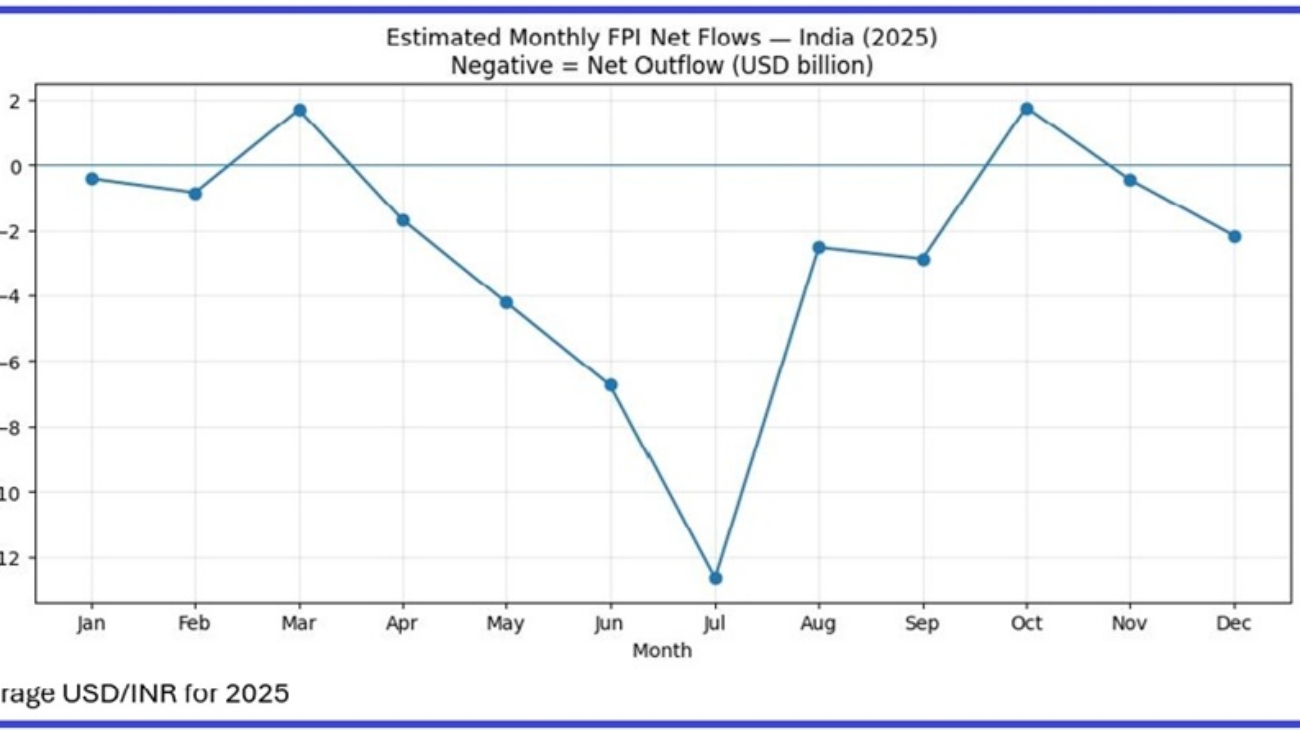

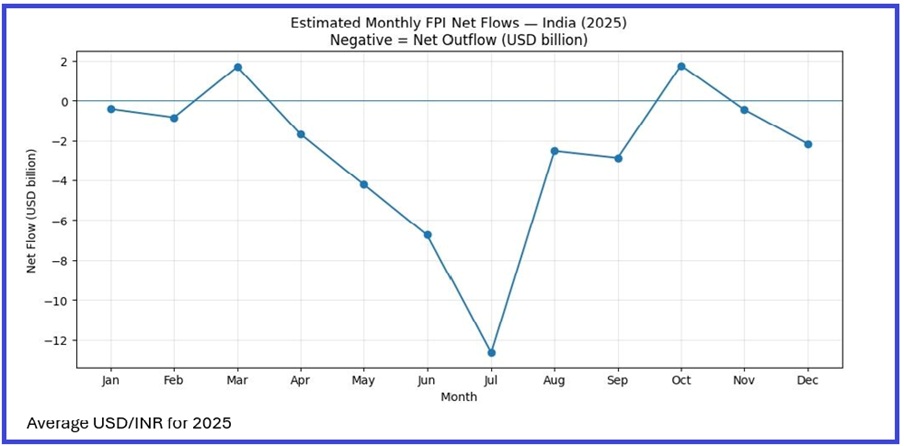

Foreign capital is neither entering India in sufficient scale, nor remaining invested. Portfolio outflows have become persistent, and this has emerged as the dominant driver of currency pressure. In calendar year 2025, foreign portfolio investors sold approximately USD 19–20 billion worth of Indian equities, marking one of the largest annual equity outflow episodes in recent years. Importantly, this selling has been sustained rather than episodic, pointing to a structural reassessment of India’s growth outlook and valuation premium rather than a temporary risk off shock.

Crucially, this capital flight is not the result of a collapse in exports to the United States. Despite tariff concerns, the U.S remains India’s largest export destination. Between April and December 2025, Indian exports to the U.S rose to roughly $65–68 billion, compared with $60–63 billion during the same period last year. Trade flows, for now, are holding up better than sentiment suggests.

The effects of capital account stress are most visible in financial markets. Indian equities are failing to attract foreign inflows as growth momentum weakens. Market leadership has narrowed, with headline indices supported by a small group of large-cap stocks, while consumption-sensitive sectors such as FMCG remain under pressure.

This dynamic fits squarely within the balance of payments framework described by Professor Michael Pettis. He described, “a country cannot sustainably run a current account deficit without stable capital inflows. When capital inflows weaken, the adjustment shows up through a weaker currency, tighter financial conditions, and pressure on asset prices.”

Indian equities now trade at some of the highest valuation multiples globally, supported largely by domestic retail and mutual fund flows. However, domestic capital is structurally constrained, while global investors can freely reallocate. As Bloomberg’s Andy Mukherjee recently noted, Indian cement stocks now trade at higher valuations than Hong Kong Tech stocks showing the exuberance of Domestic equity capital chasing local themes.

At a deeper level, India’s vulnerability reflects a structural imbalance between savings and investment. Domestic savings are insufficient relative to the economy’s long term investment needs, and the financial system lacks the institutional capacity to consistently channel savings into productivity enhancing investment. As a result, growth has become increasingly dependent on mobile foreign capital – capital that is cyclical, return sensitive, and easily reversible. It is this dependence, more than any near term trade shock, that leaves the Indian rupee vulnerable when global capital flows turn cautious.

Update: The US–India Interim Trade Agreement (February 2026)

Since this article was first written, a significant development has reshaped the near-term outlook. In early February 2026, the United States and India reached an interim trade agreement. As part of the deal, the US lowered its reciprocal tariff on Indian goods from 25% to 18%. President Trump also signed a separate executive order removing an additional punitive 25% tariff that had been imposed as a penalty for India’s purchases of Russian oil, meaning the effective tariff burden on Indian exports had, at its peak, approached 50% before being brought down to 18%.

The announcement acted as an immediate sentiment catalyst. The rupee, which had been trading in the ₹91.5–92 range under stress conditions, strengthened on the news, touching ₹90.30 before settling near ₹90.70. Foreign portfolio investors, who had spent most of 2025 as relentless net sellers, turned net buyers in the first week of February 2026, purchasing approximately $897 million worth of Indian equities.

These are meaningful moves. After 18 months of persistent underperformance relative to other emerging markets, India’s excessive valuation premium has moderated toward historical averages, which may create better entry points for global capital going forward.