Central Bank Capitulation led by Federal Reserve

The 21st and 22nd of September were potentially important signals for traders as the Federal Reserve admitted they remain reactive to inflationary pressures, and other global central banks countered with acts of their own.

While it is difficult and often foolish to believe the markets can be timed, this past Wednesday may have been an important moment for speculators in Forex. Many traders may have veered off into cryptocurrencies or into equities as day traders the past few years, but FX still remains a place that offers volatility and where wagers on price direction can be made.

The Federal Reserve raised their interest rate 0.75% again, and importantly issued a loud admission that the U.S central bank is caught in a reactionary mode. Other global central banks have begun to protect their own currencies too. Jerome Powell, the U.S Federal Reserve Chairman, said he believes the current interest rate is likely at the low end of the spectrum regarding where it has to be to have an affect on current inflationary pressures.

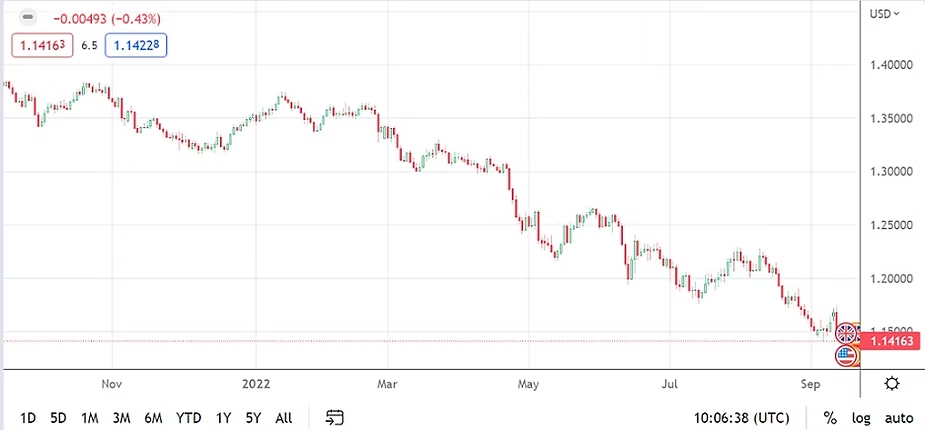

The USD has been strong against many major currencies with a rather unforgiving bullish trend. Raising the Federal Funds rate from 0.25% to 3.25% the past year in the U.S has made short term purchases of U.S debt attractive to many financial institutions. On Wednesday, Jerome Powell made it clear other hikes will be delivered and it is not farfetched to believe the U.S is looking at a potential rate of 4.50% and higher in the spring of 2023. This doesn’t mean the Fed’s policy is correct, it is simply an outlook for the potential Federal Funds Rate based on rhetoric.

A Federal Funds Rate in the U.S of 4.00% is likely by early this winter, per the Federal Reserve’s interest rate outlook.

Global central banks have reacted to the U.S Fed’s recent interest rate hike, by enacting methods to try and safeguard the value of their own domestic currencies.

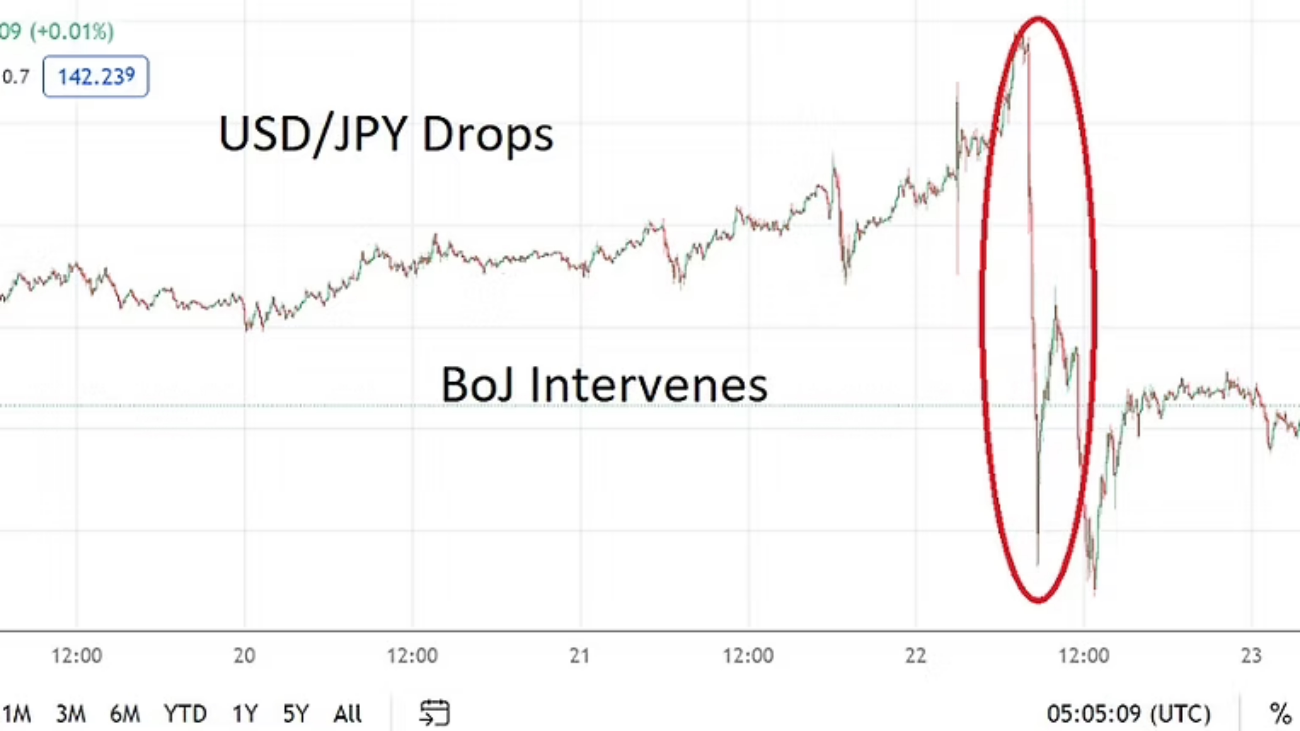

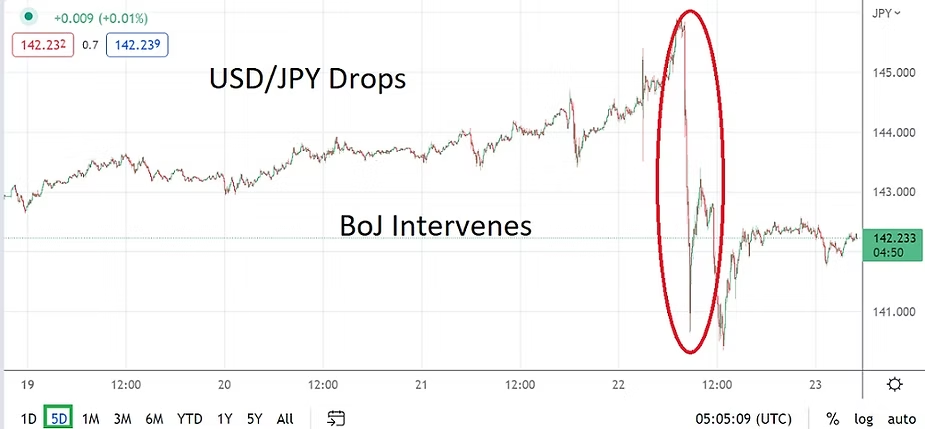

The USD surged ahead slightly before the rate announcement from the Fed, while many other currencies lost value. However, on Thursday the Bank of Japan intervened by starting to buy Japanese Yen against the USD. The Bank of Japan said it will not raise interest rates yet, but its action showed it clearly does not want the JPY to lose additional value to the USD, via the USD/JPY Forex pair. Whether the BoJ’s actions work mid-term remain to be seen.

Global Central Banks feel they must counter the U.S Federal Reserve’s Actions

Other central banks started to act too. The Bank of England and Swiss central bank both raised interest rates yesterday. Speculators who have been watching the USD dominate Forex the past year, may now have to consider that the last two day’s of action via global central banks is a signal an attitude change has taken place, which may begin to affect Forex long term. Traders need to understand opportunity also means there are risks.

Inflation remains high and governments have reached a point where they have had to admit they will have to risk slowing their economies and potentially suffer recessionary pressures to curb price increases. Many central banks likely feel they have to match the hike increases by the U.S Federal Reserve within their own systems to protect the value of their currencies.

BoJ Intervention on the 22nd of September

End of the Dominant USD Bullish Cycle in Forex?

While Japan for the moment refuses to raise borrowing rates, the BoJ’s buying of JPY effectively signals the USD has become too strong and is starting to hurt the Japanese economy. The the Bank of Japan will be interesting to study long term, to quantify if Japan’s lack of raising rates proves to actually be correct in the current environment.

Philosophical differences and central bank maneuvering is complex and has a long history of debate. Having said that the Bank of Japan has been largely scorned by many other central banks the past three decades for its methods, but while Japan has never recaptured the growth numbers it attained in the 1970’s and 1980’s, the nation remains one of the world’s richest.

The action of the BoJ and other global central banks means that speculators may want begin to look at Forex and tinker with the notion that the bullish trend of a dominant USD may start coming to an end. The cycle has been strong and again, it is difficult to say today is the day. Timing the market is often proven wrong, but the messaging from global central banks that they will start to shadow and react to the U.S Federal Reserve’s actions may mean that they will try to curtail the decreasing values of their own domestic currencies with more robust methods.

Day Traders need to understand a Complex Puzzle is Ahead

Forex markets can produce dramatic changes of value abruptly and cause costly losses to traders who bet wildly. The use of too much leverage and a lack of efficient risk management frequently destroys value quickly. However, now may be the time to contemplate testing Forex with the notion the USD may start to incrementally loss value. A lot has to happen. There are plenty of risk events ahead which could lead to wildly unforeseen results. In other words there are no guarantees.

Global equities led by the U.S indices appear very fragile and if the major stocks loss more value, this could also cause a stronger USD. Why? Because the USD would have to be purchased to buy U.S stocks by foreign investors who want a safe heaven. While it may seem contradictory to think U.S equities would be bought in downturns, this is what has historically happened when global financial institutions seek safe havens and believe other places are too dangerous to invest.

Remember financial institutions are not supposed to be day traders, they are supposed to be long term investment vehicles. Meaning if global equities suffer, even if U.S indices suffer too, the U.S is likely to remain the choice of investment houses as the place to seek shelter if they have to purchase equities as part of their mandates.

Yes, Forex will always be a complex puzzle for short term traders seeking to take advantage of the daily gyrations in the global markets. If a speculator insists on participating with wagers in the market place, they must consider that financial storms are always brewing because trading is seldom easy.