Participation of Women in the Workforce and Advancing Progress

There is more poverty in this world than many of us realize and would like to comprehend when confronted by the facts, and this is also true with India.

Recently, I visited several villages in Tiruvannamalai District in Tamil Nadu State on behalf of Angry Meta Traders to survey household capital formation, wage growth and labor market dynamics. To my astonishment, in many homes, people still use rice and palm oil purchased through ration shops. The important observation is their consumption basket appears narrow and heavily dependent on subsidized essentials. I saw simple aluminum utensils in kitchens, when higher income households often use silver-plated utensils. Things that many middle-class families consider normal like energy drinks, snacks, or packaged foods were often absent.

What struck me even more was the number of women managing families alone. In some households, the husbands had died due to excessive alcohol consumption. Children attended government schools and depended on nutritious meal schemes provided by the State.

Growing up, I have seen people wear torn uniforms in school because their family could not afford new uniform every year. Some did not wear shoes, and many students stood outside the class because the fees in private schools in India are several times higher than what government schools would charge and their families could not pay on time. Yet, through education and perseverance, many people have succeeded.

However, the poverty I witnessed in Tiruvannamalai District is different. These observations reminded me of a study published in the Lancet Regional Health Center. Researchers followed 251 children in Vellore District (closer to Tiruvannamalai District) and found that poor children living in urban areas were often exposed to calorie-rich but nutrient poor food environments.

If such conditions exist in parts of Tamil Nadu State, one of India’s more developed states, then we should think carefully about the situation across the country.

Another Transformation is Taking Place

For generations, many women carried the burden of childcare, household work, elder care and agricultural labor simultaneously. In many families, they sacrificed their own aspirations for others. Are women born to carry everyone’s burden?

Interestingly, across the globe especially in Southeast Asia, education and economic opportunities have expanded women’s choices. Researchers such as Stanford University’s visiting Professor Alice Evans argue that many women choose marriage only when their partner’s own goals align with their own. If not, remaining single becomes a reasonable choice for them

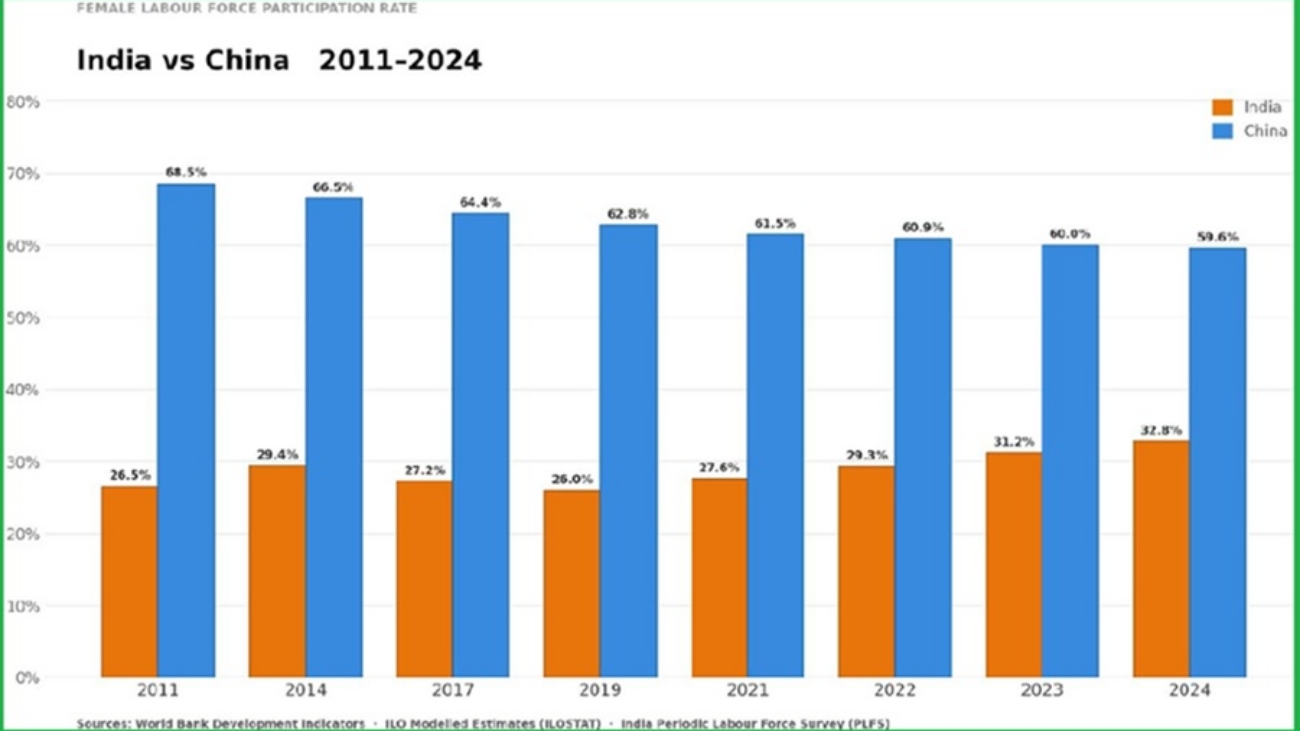

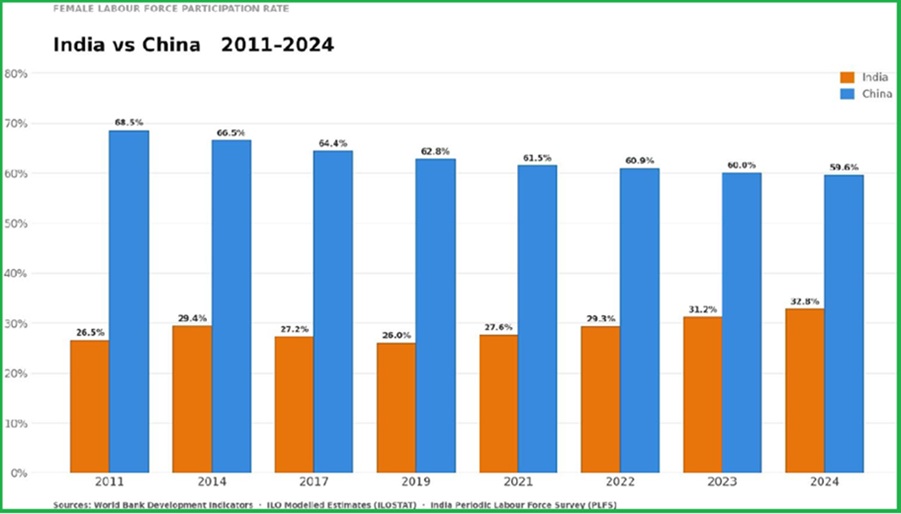

Female Labor Participation Rates Comparing India and China from 2011 to 2024

As shown in the above chart, India has certainly made progress, but female participation in the workforce remains below that of many East Asian economies. A society that fully allows women to participate in economic life is likely to become more prosperous and productive.

Economic realities are also shaping family decisions. Housing is expensive. Job markets are uncertain. Inflation remains a challenge. Asset prices have risen significantly.

Yesterday, a college friend called me. He recently built a new house in his town. He is 33 years old, unmarried, and works in Oman. Years of overseas employment and remittances have helped him to achieve his goals. I sometimes wonder whether the same outcome would have been possible had he stayed and earned entirely in India, especially outside the software and technology sectors.

India still has demographic advantages, but a demographic does not bear fruit automatically. It requires healthy, educated and economically secure citizens.

We often speak about India becoming a developed nation. However, the real question is whether growth can and will improve the lives of ordinary people, especially women, children and underprivileged. Growth matters, development matters even more.