Indian Households Face Rising Expenditures for Hospitalization and Critical Care

Many households in India face unexpected hospital expenses that have become almost routine in today’s environment. Rapid urbanization, unclean drinking water, poor air quality due to carbon emissions and industrialization have hit low and middle income homes harder than upper income families. These households are increasingly exposed to diseases that require critical treatment, but the government institutions are ill-equipped to handle the growing patient loads. As a result, many Indians are forced to seek treatment in private hospitals, where costs are significantly higher.

Consider that a middle income household in Madurai earns roughly between 15,000 to 20,000 Rupees per month per person. This per the Periodic Labor Force Survey 2023-2024 Annual Report. So if two people are working in a family, it means empirically, we can estimate the income between 35,000 to 40,000 per month. We need to compute the family’s expenditures – if one member is hospitalized for critical illness or gets hospitalized treatment in private and public hospital.

Even if the income range for this family is better than median estimates, their capacity to absorb medical shocks are limited due to high baseline consumption and minimal household savings.

In the case of hospitalization in a government facility, out of pocket expenditures such as medicines, diagnostics, transport, and wage loss can amount to 12,000 to 40,000, effectively deducting one to two months of household income.

In other words, families need to spend out of pocket by borrowing to finance these gaps for consumption and medical expenses.

However, if a family is forced to take treatment in a private hospital, they would be spending 100,000 to 500,000 Rupees in critical cases, their total spending as a higher percentage of net income and is close to 1,250% in extreme cases.

The Role of Savings and Informal Safety Nets

As observed during Covid-19 and other crises, Gold has often acted as a financial buffer for Indian households.

Families that save during stable periods are able to pledge or sell gold in times of distress, helping them to manage medical expenses without relying entirely on high cost borrowing.

In contrast households without many buffers, often turn to informal lenders or personal loans, where interest rates can range between 36 to 60% compounding the financial distress.

Looking at Government Data for Clues

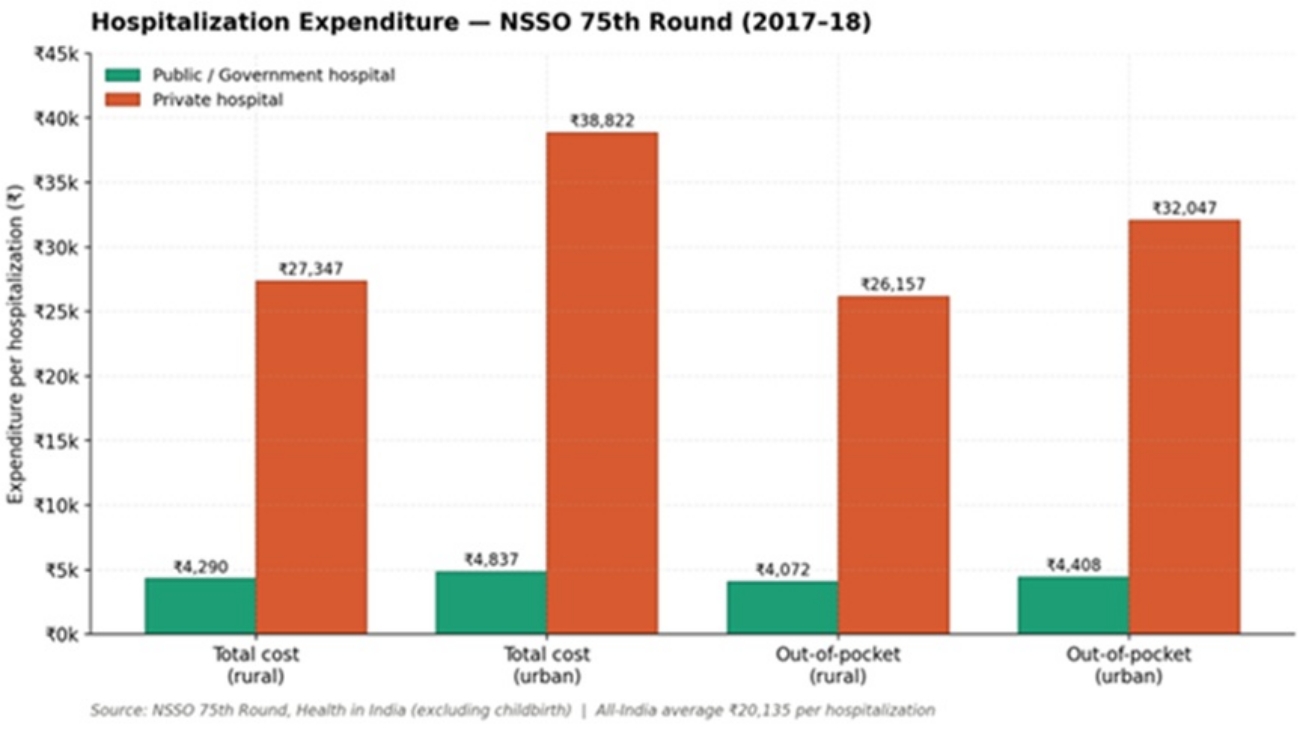

The most authoritative survey on household expenditures on hospitalization comes from National Sample Survey Office’s (NSSO) “Health in India” (2017-2018), and it showed the costs for those hospitalized in private facilities were eight times costlier than government facilitys.

An average hospitalization (excluding child birth) cost 4,290 Rupees in a rural government hospital, and 4,837 in an urban government hospital. The same scenario in a private hospital cost 27,347 in rural India and 38,822 in urban India. Out of pocket expenditures – the amount families pay themselves, follows the same pattern with families having to pay out about 4,000 Rupees in government hospitals, versus 26,000 – 32,000 Rupees in private ones.

Hospitalization Expenditure by Hospital Type and Sector, NSSO 75th Round (2017-2018). Source: MoSPI, Ministry of Statistics.

These were already catastrophic figures for a typical household in 2017-2018. A single private hospital admission cost more than a month’s wages for most Indian families, and it is getting worse.

Seven Years of 12-14% Medical Inflation

Since 2018, the cost of being hospitalized in India has risen at a pace that outstrips almost every other category of spending: Millman’s 2025 medical inflation report pegged the rate at 12% in 2024, more than triple the general CPI inflation of 4.2%.

An urban private hospital admission that cost 38,822 Rupees in 2017-2018 now is in a 76,000 – 91,000 price range, this while real wages are stagnant and not growing. Recent RBI Household surveys conclude that Indians absorb higher debt in order to manage their household expenses.

Critical Illness Can Wipe Out a Household’s Future

Critical illness like heart attacks, a cancer diagnosis, renal failure, kidney transplants costs even more in India – and the problems grow unbearable for Indian families after they are forced to take on more debt. For example, a heart angioplasty with stent that costs 100,000 in 2018 now costs between 200,000 – 300,000 Rupees in private hospitals. A kidney transplant which costs 400,000 – 600,000 a decade ago now costs 1 million to 1.5 million Rupees. A full course of chemotherapy ranges from 250,000 for early stage diseases to 2.5 million Rupees for advanced cases requiring targeted biologics.

Cost ranges for major critical illness in India, 2024-2025, green bars show public hospital costs, orange bars show private hospital costs. Sources: ACKO India Health Report 2024, HCG Oncology, Hospital Quote Data from Apollo, CARE and others.

Where the Indian Household Stands

As per periodic labor force surveys, the median Indian worker earns 10,000 Rupees a month. The Economic Survey in 2024-2025 recorded average monthly earnings of 13,279 for self-employed workers, 20,702 for salaried workers, and 12,750 for casual laborers. Crucially, only the top 22% of the India’s labor force earns more than 15,000 Rupees per month.

Monthly household income distribution, rural vs urban India (2023-2024). Sources: Periodic Labor Force Surveys, Azim Premji University Income Distribution Study 2019-2024.

Statistically, the household we have taken for the reference is not a poor household by national standards. It is comfortably above the rural and urban median, sitting in the top fifth of the country, and this is what makes the rest of the story so troubling. If this household cannot afford a critical illness, almost no household outside the urban upper middle class can afford rising hospitalization costs.

The Insurance Gap

The government of India has expanded insurance schemes for low income households since 2018 via the Ayushman Bharat PM-JAY with 500,000 Rupees coverage. But the scheme which was set many years ago, does not match the current medical costs scenarios. Income eligibility is an another problem where a majority of people who earn in the middle, slip out of the government insurance schemes and have to take private insurance to cover their health risks. Health insurance penetration in India is low at 3.7% of GDP, well below global statistical standards of 7%.

Across much of India, a single critical illness can effectively destroy years of household income accumulation and trigger debt dependence. In the absence of stronger public healthcare delivery, and without deeper insurance penetration at affordable costs providing better claims services, and lacking robust risk sharing mechanisms – escalating medical costs could act as a drag on India’s economic growth trajectory by weakening household balance sheets.

Notes: 1 USD = 93.24 INR