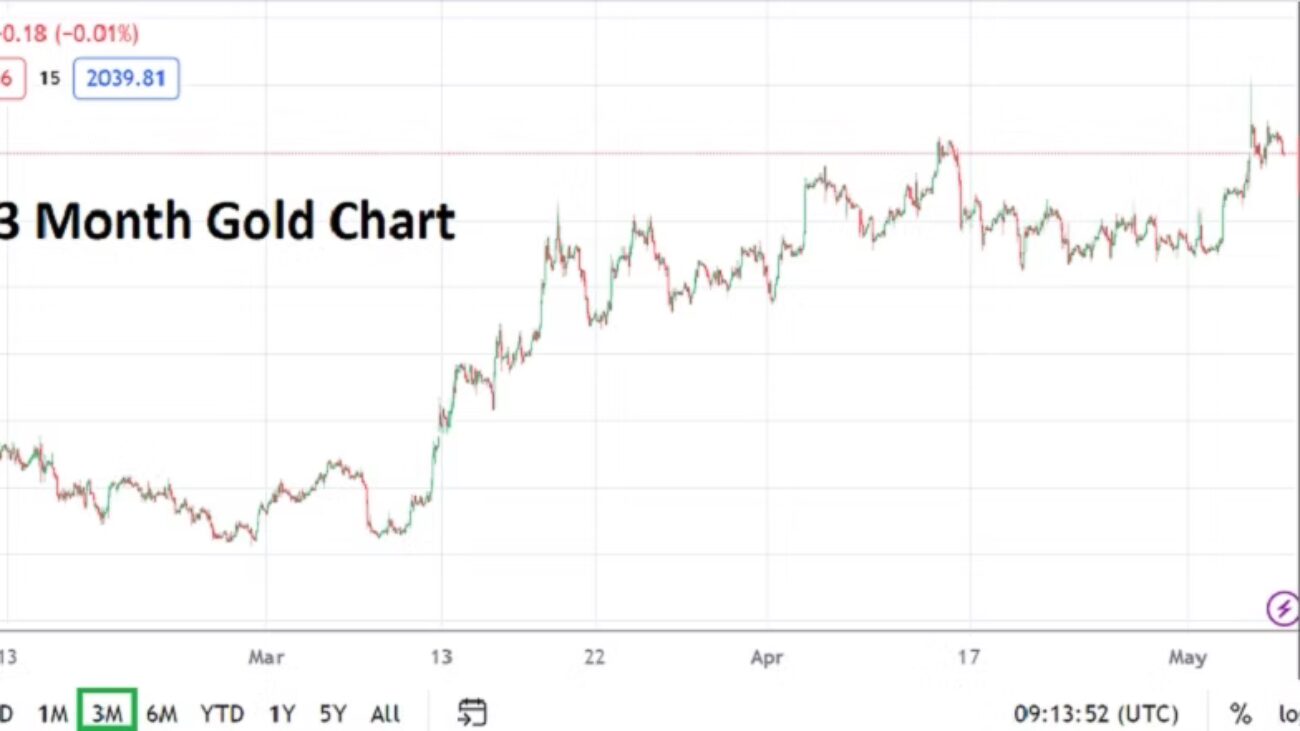

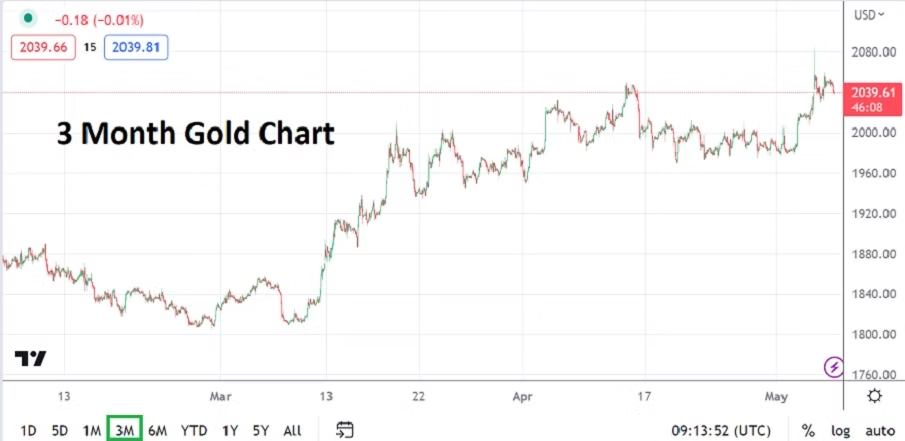

Nervous Contradictory Trading Winds for Behavioral Sentiment

Behavioral sentiment in the broad financial markets is nervous, and mixed results in the major asset classes are likely causing retail traders to feel uneasy. Most day traders try to perceive which direction they should lean based on price momentum while looking for fast profits. The current state of the broad markets are making decisions difficult for retail traders.

A healthy dose of nervousness at this moment might be a good thing for speculators and keep them conservative. Swirling results in Forex and commodities are causing plenty of problems for traders who instinctively like to pursue buying positions because of the human tendency to be optimistic.

Federal Reserve Causing Headaches for Smaller Banks and Forex

Forex markets have been choppy since the beginning of February 2023, when the U.S Federal Reserve surprised many people with continued aggressive rhetoric. The U.S central bank has backed up its ‘tough’ talk as it ‘fights’ inflation with more interest rate hikes. Clarity regarding a potential June hike from the Fed remains problematic with no certain answer yet. For the moment there seems to be a belief there will be a genuine pause, which may be fueling better returns for U.S equity indices, but there are no guarantees. Behavioral sentiment remains fragile.

The detrimental effect from higher interest rates on mid and small size banks in the U.S remains harmful. Mid and smaller corporate banks continue to struggle with the increased Federal Funds Rate. Bad business decisions within these banks have made it difficult to make profits in an environment when money is no longer ‘free’, this as many of their depositors look for better returns.

A six month chart of the EUR/USD below shows how the EUR started to climb in the fall of 2022, but then began to run into headwinds when financial institutions started to reconsider the seriousness of U.S Federal Reserve policy earlier this year. Analysis regarding the timing of the Federal Funds Rate forecast to actually start becoming dovish has proven problematic.

While the EUR/USD still maintains plenty of its gains, the current price of the the currency pair is below early February highs. The EUR/USD was trading near 0.95700 in late September of 2022, and the price as of today near 1.07800 is a vast improvement for the EUR. However, the choppiness of the Forex market the past few months has not been easy for day traders who have suffered from sudden reversals frequently in many of the major currency pairs.

EUR/USD Six Month Chart as of 19th May 2023

The KRE regional bank index below shows the dramatic drop in value of the mid and small size banks in the U.S the past year, and the sector certainly still has financial concerns and shadows which are causing pressure on their corporate share values. Stubborn inflation remains and the desire of the U.S Federal Reserve to attack rising costs with higher interest rates remains a serious concern.

KRE Regional Banking Index One Year Chart as of 19th May 2023

Stock Markets Suddenly at One Year Highs as Investors Seem to Return

Is the S&P 500 a harbinger of things to come or are investors in the index being too optimistic? Day traders likely stay away from the S&P 500 many times because they are mostly trading the index via CFD’s and this can prove expensive regarding transactions, they are not long-term investors – meaning they do not like to make bets that take awhile to materialize. The results from the past year and a half in the stock markets have made speculators nervous regarding bets on equities.

However, institutions and long-term investors buy and hold the S&P with a vision towards the future; they also reap the rewards of its dividends. The ability of the S&P to be trading at nearly one year highs is curious. The improvement in equity values in the indices may be a sign that ‘smart money’ continues to invest in the stock market for the long-term, even during what is perceived as a fragile period of behavioral sentiment. Financial institutions may also be betting on the U.S Federal Reserve having to become more dovish regarding interest rate policy in June and looking forward.

S&P 500 Index One Year Chart as of 19th May 2023

Results on the NASDAQ 100 may be surprising to many and the index is trading at one year highs, and though like the S&P it is still under all-time highs from late 2021 and early 2022, investors have shown a taste for investing in the ‘hi-tech’ index again. While this may contradict the behavioral sentiment of Forex and the results in the mid and small size banking sector, the NASDAQ 100 does point out money is still being invested and might be an indication that day traders need to be more patient, more optimistic about the coming months and year.

While a recession might be looming, large companies have started to lay off workers and scale back on bonuses in an effort to fight against reduced profits. The narrative from the media may be negative in many cases, but many long-term investors tend to look at more conservative fiscal policy in companies as a good practice and a sign they should invest.

Perhaps the market is going through a needed case of the jitters and the U.S indices are showing that brighter days are ahead, even if there are storm clouds that still must be dealt with regarding inflation and possible recession.The long-term horizon tends to always be more optimistic. Day traders may not be able to take advantage of quick hitting trades, but what about changing perspective and looking for more patient results by being more conservative as a speculator? Or maybe investors in the stock market are wrong and another violent selling surge will return into equities, but what if it doesn’t.

NASDAQ 100 Index Five Year Chart as of 19th May 2023

There is a fear among mid-size brokers that trading volumes in many sectors are dropping. Showing cautious investor sentiment on the retail front – which may be a healthy reaction in many respects because it is hard to read momentum right now. Day traders tend to get killed by the daily gyrations of Forex and equities in choppy markets because they are using too much leverage. However, historically when retail traders have turned cautious, this is when institutional trading houses have tended to do remarkably well. Investment houses can take on more risks in markets that are perceived as nervous and fragile, because they have a longer time horizon and more cash to absorb momentary losses.

Commodity prices are also intriguing because after hitting highs nearly one year ago in May and June of 2022, the ratios of many broad commodity indices have come down and values are traversing near late 2021 levels. Which brings us to the consideration that global demand for physical resources are limited because corporations are not making large purchases of commodities, this as they wait on better manufacturing demand for their products. This may appear contradictory and create nervous behavioral sentiment for traders, but cautious business practices are a way to make sure there is enough money for the future when conditions turn optimistic again.