Predicting the Federal Reserve and President Trump's Rhetoric

Financial institutions have grown accustomed to the rather fierce rhetoric from President Trump in the early days of his second term. Financial institutions have also become quite used to the recent overly cautious statements from the Federal Reserve. This Wednesday the Fed’s FOMC Statement will be delivered and there will be no change to the Federal Funds Rate. The current ‘main’ borrowing rate offered by the Fed is 4.50%.

This Wednesday Fed Chairman Jerome Powell will speak about the recent CPI and PPI numbers which came in below expectations. This typically would be a good signal regarding weaker inflation. And Powell might also mention that energy prices in the U.S have started to erode. WTI Crude Oil is now trading in a sustained manner below the 70.00 USD threshold, and this will influence the potential of less inflation. It is a good development for the U.S and Federal Reserve.

However, Powell is unlikely to express the unease and anxiousness the Federal Reserve has regarding President Trump, this because the Fed certainly doesn’t want to get into an open confrontation with the White House.

The U.S Treasury is now being run Scott Bessent who was selected by President Trump. Bessent ran the Key Square Group and is well respected in financial circles, which includes vast experience in top financial institutions. Powell though perceived as pragmatic by many analysts, may not be within President Trump’s trusted inner circle like Bessent and Commerce Secretary Howard Lutnick, the former Chairman and CEO of Cantor Fitzgerald. Lutnick is perceived as a workhorse who get things done and is smart.

The Fed’s likely cautious FOMC Statement will not be enough to appease President Trump this week. While some may think Trump’s attention will be elsewhere, those who have come to understand Trump know his capability to react quickly to events should be taken seriously.

What will Bessent and Lutnick think about the Fed’s FOMC Statement and stance? Powell is not a trained economist, do Bessent and Lutnick trust Powell? One thing for certain is that Janet Yellen who served as the Fed Chairwoman before Powell, and the Treasury Secretary before Bessent is not part of the inner circle in the White House.

Powell’s loyalties may be questioned, and eyes should be kept on Trump later this week to see how the President responds to the rather cautious Federal Reserve. The Fed will certainly not want to say aloud it is waiting like everyone else regarding the effects of tariff negotiations and their implications. Powell wants to keep his job. Trump certainly wants lower interest rates. Bessent and Lutnick certainly want lower interest rates too, but like Powell these two may prove pragmatic and know inflation needs to erode further. The Treasury and Commerce secretaries may want to test chicken and egg questions. Will these two gentlemen push Trump to proactively push for lower interest rates in a louder fashion?

Day traders will have to wait to see how financial institutions react to tomorrow’s FOMC Statement – which has already been accepted as being a ‘no interest rate cut event’. And it is probably being discussed in the White House that the Fed may want to wait until early this summer – June? – to consider another interest rate cut. Which means the Fed may not be cutting interest rates mid-term, while the ECB and BoE may have to be more dovish and remain active via interest rate cuts if their economies continue to show recessionary trends.

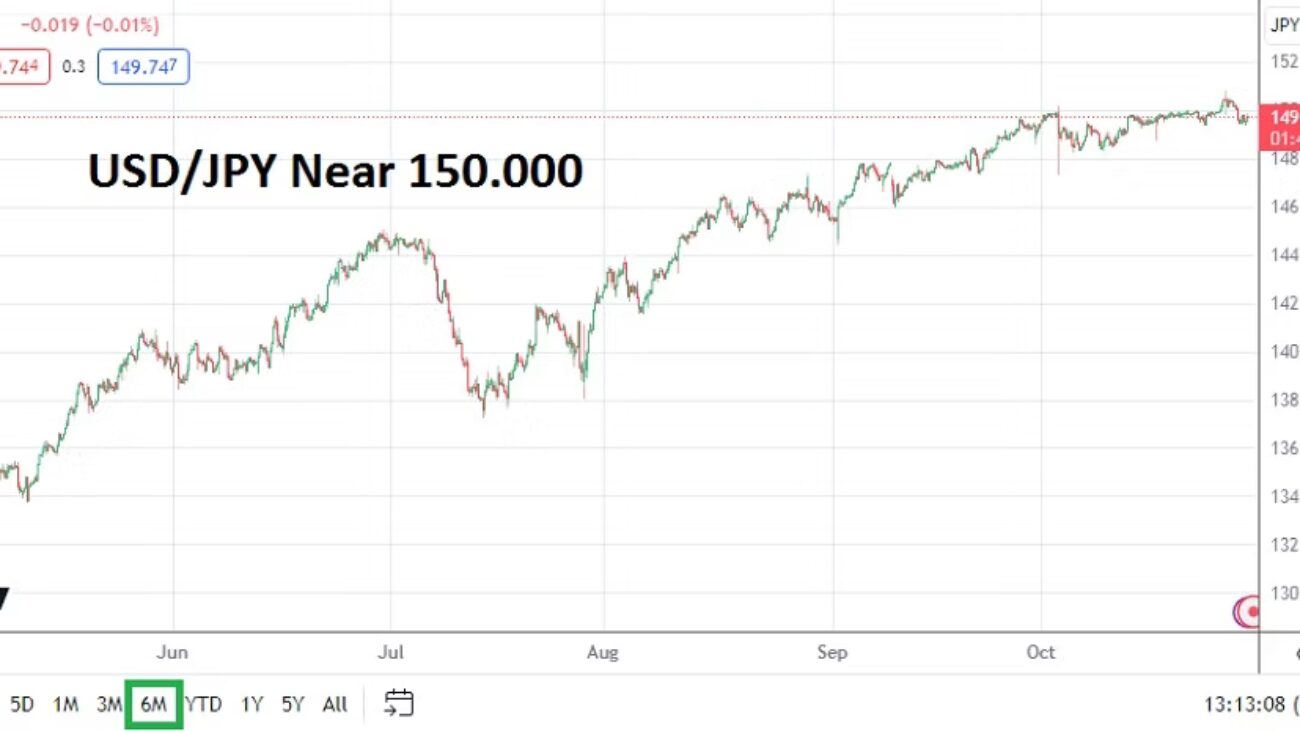

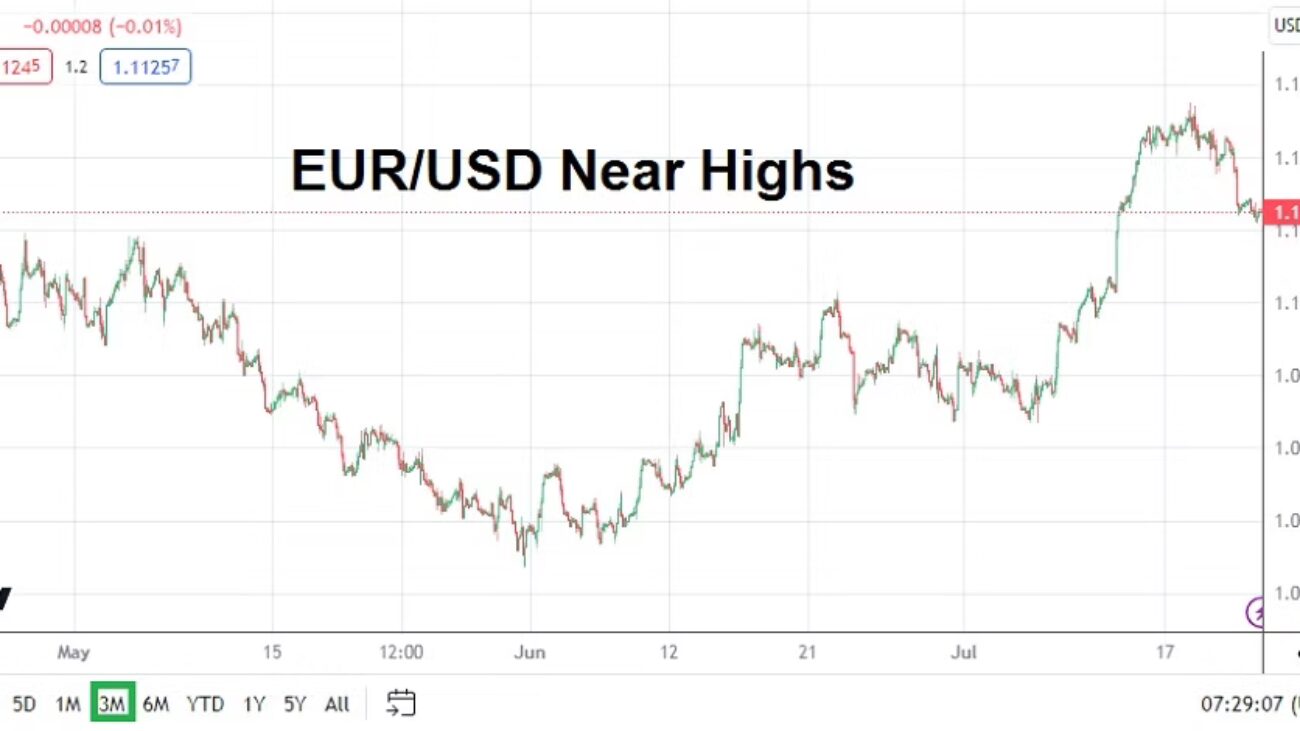

Meaning that risk premium which was factored into the stronger USD centric buying since the Trump election on the 5th of November until the peaks in mid-January and early February, and have now reversed lower – needs to be watched technically and weighed in combination with behavioral sentiment.

Intriguingly the US Dollar Index is around levels it stood at on the 5th of November (Election Day 2024). It is also near values seen on the 15th of October. (Did financial institutions start to bet on a stronger USD around this time because of a more cautious Fed outlook and the potential Trump was going to win the election?) Raising the question, if financial institutions envision the USD can technically be weaker and attain values seen in late September and early October when the US Dollar Index was testing support levels which have held since April of 2022. The US Cash Index which stands around the 103.070 level now, was trading near 90.00 in the spring of 2021.

Trump wants lower interest rates, the Fed wants to wait on cutting the Federal Funds Rate until they have clarity regarding the results of tariff negotiations. There will be a collision between Jerome Powell and Donald Trump, the only question is when it will happen. The US Dollar Index has been lower historically. Trump, Bessent and Lutnick may not want to say it out loud, but a weaker USD in the global economy would help U.S exporters. A weaker USD may not convey the strong populist rhetoric of MAGA, but it may be economic hardware the Trump administration actually seeks. To sustain a weaker USD, inflation levels will have to erode, and interest rates will have to be lower (and another myriad of complex events have to happen), until then rhetoric and risk premium will factor into USD Forex trading for financial institutions and speculators.