Summer Optimism as Forex and Equities Focus on Fall Outlooks

Fed Chairman Jerome Powell admitted the obvious at the Kansas City’s Fed’s Jackson Hole Symposium last Friday. The realization the U.S Federal Reserve is going to cut interest rates confirmed what many financial institutions had positioned their trading desks for via forward cash Forex contracts over the past month.

USD Cash Index One Year Chart on the 27th August 2024

The USD has been expected to grow weaker by many people because most knew the Fed would have to state a September rate cut would be delivered. The question that was also somewhat answered is the notion if the Fed will also cut in November. Though Powell certainly did not say a rate cut would happen in November, his rhetoric made it clear the Federal Reserve is considering a dovish perspective which could translate into additional cuts down the road.

The Fed has been criticized for being too passive and while Powell can be congratulated for his rather unemotional Federal Reserve leadership, he and the Fed can certainly be faulted for not reacting quickly enough to ‘transitory’ inflation and then not responding until this past weekend to the need for cutting interest rates with dovish rhetoric. Let’s also remember the U.S Treasury (government) is on the line to pay exorbitant costs for debt repayments because of bad U.S fiscal policy.

As an interesting related side note, the head of the Brazilian Central Bank, Roberto Campos Neto, made a strong appeal for governments to be fiscally responsible while speaking at the Jackson Hole Symposium this past weekend. While he could have been talking to any number of nations regarding spending, his points were obviously meant to highlight his disagreements with the Brazilian government led by Lula da Silva and the Workers Party. Roberto Campos-Neto stated that approximately 50,000,000 (yes, million) people in Brazil receive government allowances, while only about 43,000,000 people are earning money via employment and business enterprises. Traders who want to keep an eye on the USD/BRL this week may be entertained by the potential volatility within the currency pair which is trading a hair below 5.5000 before it opens today. The USD/BRL has certainly not been correlating to broad Forex USD centric weakness, and demonstrates the internal domestic fight between Lula da Silva and the Brazilian Central Bank regarding fiscal policy.

Jobs data from the U.S has continued to turn negative, particularly via revised reports which are being published rather ‘quietly’ as election season approaches. Yet, financial institutions have been aware of the weaker jobs numbers. While the poor jobs numbers combined with eroding inflation is good for USD centric weakness due to the knowledge the Fed will have to reverse from its rather high interest rates, the question becomes how much per the financial institutions selling of the USD has been acted upon in Forex. Is the USD oversold for the time being? It depends on trading timeframes certainly.

Weaker USD centric positions will need more impetus for further bearish trajectories to be seen near-term. Financial institutions may believe equilibrium is being approached, this because it appears interest rate cuts equaling a 0.50% decline seem to have been factored into Forex. Will the Federal Reserve be put into a position in which they will be able to cut by a full basis point (-1.00%) over the next six months?

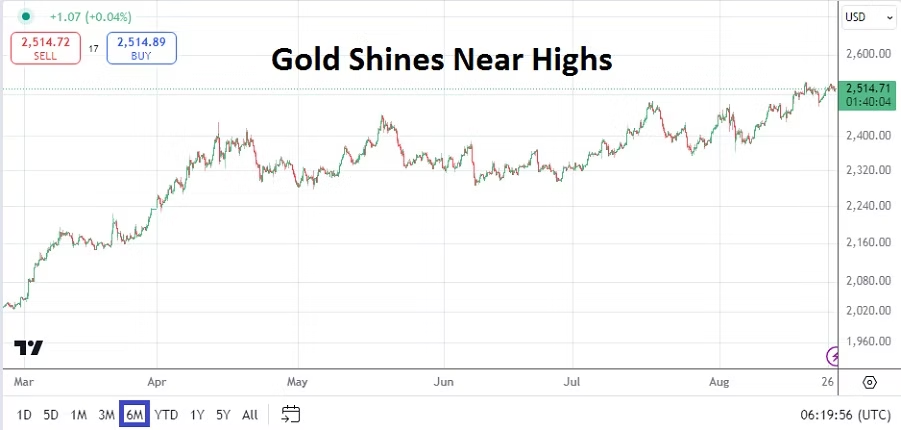

Gold Six Month Chart on the 27th of August 2024

Gold is trading near 2,500.00 plus at the time of this writing. Gold has touched higher levels in the past week and is getting a round of applause from its throngs of believers who proclaim the precious metal the ultimate safe haven against inflation and erosion fears via fiat currencies – including the USD. As a reminder, Bitcoin is highly speculative and doesn’t have the historical (thousands of years) track record that gold has acquired.

GBP/USD Five Year Chart on the 27th of August 2024

The EUR and GBP are traversing higher territories not seen in a while. The EUR/USD is near the 1.11700 level, which was last traded in July of 2023, and it has been since 2022 that sustained prices above this current realm have been traded. The GBP/USD is near 1.32000 and is within a value ratio last seen in March of 2022. Central banks will remain in focus as summer ends and the fall trading season gets underway. The ECB will release their Main Refinancing Rate on the 12th of September, the Fed will present the Federal Funds Rate on the 18th, and the BoE will follow suit with the Official Bank Rate on the 19th.

However, those September dates are still a few weeks away and financial institutions do have data this week which could stir Forex, equity indices and U.S Treasuries in the near-term. Day traders often do not have the ability to rely upon mid and long-term outlooks, and instead have to be content with trying to ride the momentum trends being caused by larger players. While the USD weaker outlook is tempting to rely upon, speculators who are looking for quick hitting wagers need to judge technical charts and try to grasp existing behavioral sentiment which can shift rapidly depending on lengths of time.

Traders should remember the U.S will celebrate its Labor Day holiday next Monday, which sets the stage for potential sudden volatility to flourish before big financial institutions in the States leave for their long weekend. The last week of August should be rather tranquil. Certainly most long-term investors feel as if they have more clarity regarding interest rates and will be able to relax. The hope is that the current calm is not the quiet before the storm due to lingering political issues in the U.S, France and elsewhere. And that escalation of the Ukrainian and Russia war, and the Middle East conflict do not cause sudden surges of bedlam.

Economic data events the remainder of this week that should be given consideration includes the U.S CB Consumer Sentiment reading today. Yesterday’s U.S Durable Goods Orders came in with mixed results as the Core number fell by minus -0.2%, but the broad number came in with a substantial gain of 9.9%.

USD/JPY Three Month Chart on the 27th of August 2024

The Bank of Japan has published their Core CPI data today and the outcome came in below expectations with a gain of 1.8% compared to the estimate of 2.1%. The USD/JPY is trading near 144.790 at the time of this writing as it continues to show bearish tendencies. The Bank of Japan which was heavily criticized in many circles may actually be achieving what they have planned, this as they have tried to stimulate stronger export and confront inflation. Their battle is not over yet.

Australian CPI data will be published on Wednesday. And on Thursday, German Preliminary Consumer Price Index numbers will be released. The EUR/USD could react to this report, but the European Single Currency remains highly USD centric. Which sets the table for the U.S Prelim Gross Domestic Product report also on Thursday. The growth number from the U.S could diminish selling considerations for the USD if the report comes in stronger than expected. However, the GDP Price Index and weekly Unemployment Claims from the U.S could also impact short-term behavioral sentiment and cause a bit of turbulence if negative results are published.

Friday will see more CPI numbers from Japan, CPI and GDP numbers from France, and GDP data from Canada. But before going into the long holiday weekend the U.S will present one more major report with its Core PCE Price Index and the monthly statistic is expected to show a slight gain of 0.2%.

China watchers will get Manufacturing PMI numbers early on Saturday. Recent China data continues to show signs of economic stress regarding foreign investment, domestic consumer spending, and deflationary results. Buyers beware.

Lack of Big U.S Data this Week but Fed Officials to be Heard

There will be an absence of large trading volume in many markets today, because of the U.S and Canada Labor Day holiday celebrations. Results from forex markets should be considered with a healthy dose of skepticism by day traders. If you choose to participate today, using entry price orders may protect you against the possibility of price volatility due to quiet markets having the ability to create sudden jolts.

Day traders are advised to be on the lookout for potential surges to develop on Tuesday. U.S financial institutions returning to the markets in full could possibly react to economic data from the States that they may not have acted upon yet, this as outlooks may have been reconsidered over the Labor Day weekend. Equities and indices, U.S Treasuries, and gold should get plenty of attention this week as summer trading comes to an end.

EUR/USD Three Months Chart as of 4th Sept. 2023

Monday, 4th of September, E.U ECB President Christine Lagarde – the ECB chief will be speaking in London later today. The ECB President might get the attention of EUR/USD traders who may still be scratching their heads regarding last week’s decline in the EUR and trying to figure out why it happened.

AUD/USD Three Months Chart as of 4th Sept. 2023

Tuesday, 5th of September, Australia RBA Cash Rate – the Reserve Bank of Australia is expected to hold its ground and make no major changes to interest rate policy. The AUD/USD is trading at lows the RBA has acknowledged are troubling. However, there seems to be little the RBA can really do except to wait out the U.S Federal Reserve’s rhetoric to change. As a note, GDP numbers will come from Australia on Wednesday.

Wednesday, 6th of September, Canada BoC Overnight Rate – the Bank of Canada is expected to keep its interest rate policy steadfast without any changes. The USD/CAD could react momentarily to the Bank of Canada’s Rate Statement.

Thursday, 7th of September, China Trade Balance – economic statistics from China have been troubling over the mid-term and there is no reason to think they are suddenly going to turn optimistic. China is receiving plenty of negative attention from ‘Western’ analysts, but the concerns expressed could be legitimate. Slumping growth, real estates problems, and the shadow of deflation are issues in China.

Thursday, 7th of September, U.S Federal Reserve Officials – several high ranking members from the Fed will be speaking at various conferences across the States. Following the lackluster economic data published in the U.S the past couple of weeks, comments from the Federal Reserve members should be given attention to see if they begin to acknowledge interest rate policy should turn more dovish. USD traders will certainly have the ability to spark Forex on Thursday if rhetoric from the ‘officials’ starts to change tone.

Friday, 8th of September, Japan Final GDP – the Gross Domestic Product numbers could prove interesting for USD/JPY traders. Growth is expected to show a gain of 1.4%. The GDP Price Index results should be watched and are expected to match last month’s number with a gain of 3.4%.

Saturday, 9th of September, China CPI and PPI – the inflation numbers will be of interest to investors. These data reports could prove more important than the Trade Balance results released earlier in the week. The USD/CNY should be monitored in the wake of these inflation (deflation) results.

Absurd Friday Forex Results? Suspicions as the Week Begins

This coming week may be an opportunity where speculators can test their conspiracy thinking, perceptions of technical and fundamentals in unison. Experienced traders who typically have a high degree of skepticism about markets (particularly when results don’t go in the direction they expected) may question late last week’s results.

EUR/USD 5 Day Chart as of 3rd of Sept. 2023

Without trumpets or too much hyperbole, was Friday before going into the weekend a ‘false flag’, this as the USD gained strength against many other major currencies. A lack of volume because of the Labor Day holiday coming in the U.S and Canada tomorrow may have affected the Forex landscape. While trading is largely done by computer programs in financial institutions, day traders should understand last Friday worked as a get away day to enjoy a long holiday weekend in North America.

Meaning financial executives largely escaped their offices because they have seniority and the ability to disappear while their ‘underlings mind the store’. Essentially senior management often tells the staff that has to stay behind, “monitor and not touch the system”. This could have left the door open for what appears to be a strange reaction in Forex upon what was in fact weaker data on Friday from the U.S via the Average Hourly Earnings which came in slightly below expectations, and less than stellar U.S GDP results on Wednesday the 30th of August.

Yes, also this past Friday the Non-Farm Employment Change numbers were fractionally better this month than anticipated, but the prior month’s results were actually revised downward. And yet the USD remained strong. Is this because senior analysts, chief traders and risk management officers were absent on Friday?

Tomorrow the same folks will remain largely away from the markets too, meaning results should also be viewed with suspicion. Which sets the table for an intriguing Tuesday and Wednesday for all the major and minor currency pairs teamed against the USD. Gold and equity markets will need to be monitored closely too.

Gold Cash Price Five Day Chart as of 3rd Sept. 2023

Some potential clues are that the price of gold stumbled slightly on Friday as the weekend approached, but this happened as the EUR/USD sank to a low for the week, and the GBP/USD came under renewed pressure. But again this happened in rather questionable circumstances. Important support levels technically may get tested tomorrow, but trading volumes should be examined. Gold in many respects held onto gains made earlier in the week.

Yes, there are reasons to be nervous in financial institutions, due to higher short-term U.S Treasury yields, concerns about the China economy, mortgage rate worries in the U.S and elsewhere, fears about credit availability for small U.S businesses. However, these troubles have not caused a massive meltdown in the most primal of trading venues yet – major stock indices.

September is a notoriously volatile month for equities and speculators who use CFDs to participate in the stock markets globally need to be careful. Correct, some well known ‘traders’ are talking about a coming selloff in the markets, but so far we have not seen a major decline in the NASDAQ, S&P 500 or Dow Jones 30 indices. Day traders should not and cannot underestimate the potential for volatility to occur suddenly. Successful speculative bets via limited funds often means having to practice patience and risk management.

Thus, as the week begins early this Monday, day traders should be careful. Please note that a lack of big trading volumes because of the absence of U.S and Canadian financial institutions will make tomorrow’s results questionable. Opening the door for the potential of reversals on Tuesday, which might be abrupt as a ‘re-balancing’ of sorts takes place as folks returning to their offices seek equilibrium perhaps with their adjusted outlooks.

Simply put the U.S Federal Reserve the past two weeks has seen the same lackluster U.S data as all global traders, and the U.S central bank is in no position to raise interest rates over the mid-term. It would be useful if the Fed voiced their insights regarding the weaker than expected U.S Gross Domestic Product results last week, and the lower than expected Average Hourly Earnings report seen before the weekend. However, do not count on the Federal Reserve to do the right thing.