Reserve Bank of New Zealand Expected to Cut 0.50 from Rate

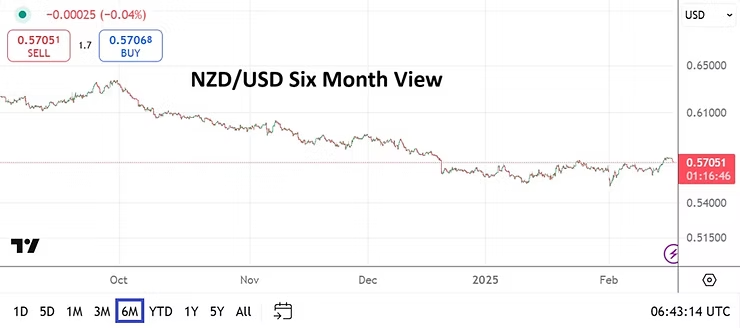

NZD/USD Six Month Chart as of 18th February 2025

NZD/USD Revival Mid-Term Coming? Reserve Bank of New Zealand is expected to cut its Official Cash Rate by 0.50 on Wednesday. N.Z govt is being proactive as they try to ignite the economy. The RBNZ also cut by 0.50 basis points in November. The central bank is expected to continue to remain aggressive tomorrow and suggest further cuts will be seen, perhaps via 0.25% afterwards.

The NZD/USD was trading around 0.63600 in late September of 2024 after gaining in correlation against the USD with the broad Forex market, via a bullish run which began in July. The NZD/USD is still traversing within its lower realms and it is logical to assume many financial institutions feel that support levels around the 0.56000 vicinity will prove rather durable going forward.

Day traders who believe the mid-term holds an optimistic bullish run for the NZD/USD may be correct, but speculators cannot be overly confident about a sustained surge higher quite yet. Conservative leverage is urged while looking for upside while betting. Speculators also need to remember tomorrow’s expected interest rate cut from the RBNZ has already been factored into the currency pair.

The rate cut is important for Wednesday, but it is the stance the Reserve Bank of New Zealand takes via its Monetary Policy Statement that affect behavioral sentiment among financial institutions. If the RBNZ sounds cautiously aggressive, meaning they suggest further cuts are being strongly considered this could help firm the NZD/USD and create more optimism regarding the potential for a move higher.

Yes, the shadow of the U.S White House administration looms over the Forex landscape. Decision making will remain tentative via financial institutions, but it is reasonable to suspect large players would treat clarity from the Reserve Bank of New Zealand with a positive Forex stance.

Monday’s trading provided a solid oversight for day traders to observe market conditions in commodities, Forex and equities. Financial institutions appear to be leaning towards a belief the U.S Federal Reserve will have to become more dovish, but financial institutions and other large players are worried about shadows being caused by inflation concerns and timeframes which are likely sparking nervous wagers.

Via the commodities, results saw Gold come down from highs on Friday which approached the 2,380.00 USD perch, and drop to lows around 2333.00 yesterday. The precious metal remains within sight of record values, this as questions persist about USD direction, and speculative forces bet. WTI Crude Oil meanwhile climbed from a selloff late Friday and into yesterday’s opening while challenging the 77.75 USD vicinity, and as of early Tuesday is now over the 79.00 mark again.

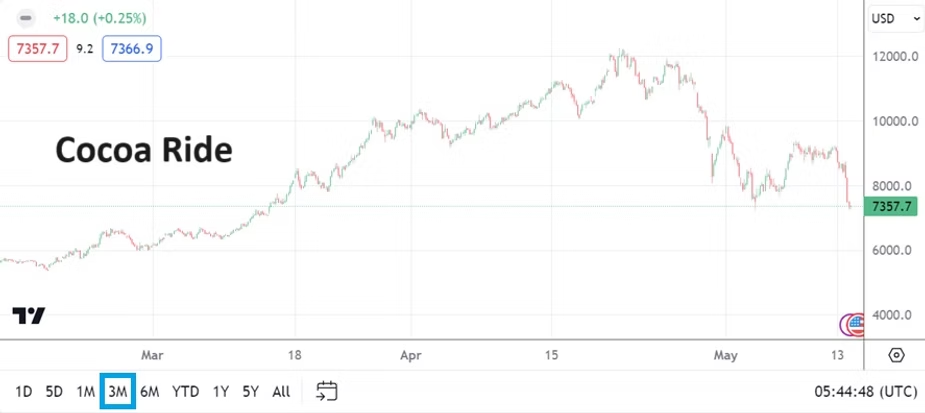

Also within the volatile world of commodities it needs to be mentioned that Cocoa which regained a portion of its higher price values last week and finished Friday above 9,000.0 USD per metric ton, fell swiftly in yesterday’s trading session and is now traversing 7,357.0 USD. Cocoa has enjoyed a spectacularly wide ride of maneuvering via market forces. The commodity is still valued within loftier heights when compared to its historical averages, and demonstrates the speed and danger (and opportunity) of price velocity.

Cocoa Three Month Chart on the 14th of May 2024

Further signs of risk appetite and fragile notions are being exhibited via U.S equity indices, which produced sideways price action yesterday as important economic data awaits and will certainly churn short-term and mid-term perspectives. The S&P 500 is again within sight of record levels, while investors of it and the Dow Jones 30 and Nasdaq 100 all brace for this week’s data which will affect their risk outlooks.

S&P 500 Index Three Month Chart on the 14th of May 2024

Monday, 13th of May, New Zealand Inflation Expectations – yesterday’s quarterly result came in slightly below the previous report. The decrease of inflation concerns likely helped the NZD/USD spark Monday’s climb above 0.60300 briefly. This morning’s early trading is seeing sideways action as U.S inflation reports are anticipated and the currency pair ebbs around 0.60180.

GBP/USD Three Month Chart on the 14th of May 2024

Tuesday, 14th of May, U.K Average Earnings Index, a gain of 5.7% has just been posted. This result will make GBP/USD traders nervous because it highlights that inflation remains sticky in Britain. While last week’s GDP numbers from the U.K showed an improvement, the growth certainly was not spectacular. The range of the GBP/USD remains choppy and bullish day traders targeting higher ratios on the belief the currency pair remains in oversold territory need to consider their timeframes and bias. While the 1.26000 may look like a logical target, it will take weaker U.S inflation and USD centric price action to get there.

Tuesday, 14th of May, U.S Core Producer Price Index – last month’s core report matched expectations. However, the PPI numbers occasionally spell trouble in Forex. Higher inflation results from the U.S would certainly kickstart volatility for all major currency pairs today.

Wednesday, 15th of May, U.S Consumer Price Index – this reading could prove to be the prime mover for financial assets this week because of its potential affect on behavioral sentiment. The Federal Reserve watches this number because of the influence it has on the American public. Forex will react to this report and if it is weaker than anticipated this would create weaker USD centric price action. The U.S will also report Retail Sales and the Empire State Manufacturing Index statistics on Wednesday.

USD/JPY Three Month Chart on the 14th of May 2024

Thursday, 16th of May, Japan Preliminary Gross Domestic Product – last month’s report came in with a gain of 0.1%. This GDP data carries an expectation of minus -0.4%. Traders who like fundamentals should pay attention to revisions within the statistical pages. The Bank of Japan remains in a curious and suspicious predicament. After two interventions, the USD/JPY has climbed incrementally once again. The BoJ is certainly keeping their eyes on the USD/JPY and know financial institutions are still wagering against the Japanese Yen.

Day traders should be extremely cautious with the USD/JPY because the BoJ has the ability to strike with a massive blow when not expected. Risk management is essential for speculators wagering on this currency pair. Evidence of speculative interest in the USD/JPY correlates to the notion that while the USD has been weaker against many major currencies recently, the Japanese Yen remains within a weaker and elevated price range.

Friday, 17th of May, China Industrial Production and Retail Sales – economic dark clouds continue to cascade on Asia’s largest economy. The industrial numbers will be watched by investors certainly, but the overall health of Chinese consumers will likely be the focal point. The USD/CNY remains within bullish terrain, but the Shanghai Stock Exchange’s SSE Index has done well since its lows in the first week of February.

AMT Top Ten Miscellaneous Sunrays for the 23rd of February

10. Word of the Day: Abeyance – the state of suspending something until another issue is resolved. Can you say, “Central Banks”……we knew you could.

9. South Africa: National election is scheduled for the 29th of May. Will the disdain the ANC and EFF have for the ‘West’ be addressed by voters or will the masses elect the usual suspects?

8. China and Germany: New Home Sales prices dropped again in China per data released this morning, Germany’s GDP data published today shows negative growth and recessionary pressures growing.

7. Nvidia: Their quarterly earnings report this week showed Artificial Intelligence isn’t a mere marketing tool, but a moneymaker opening a new era for technology.

6. South Carolina: Nikki Haley apparently will lose the Republican Primary in her home state tomorrow, but likely stay in the presidential race hoping that Donald Trump implodes via his own ego or legally.

5. Don’t Touch that Switch: AT&T believes yesterday’s widespread phone outage was caused by human error, not a hack.

4. U.S Equity Indices: Timeframes and patience remain crucial for investors amidst daily gyrations, this as the S&P 500, Nasdaq 100 and Dow Jones 30 explore record values.

3. New Zealand: Will the Reserve Bank of New Zealand go against the grain and actually raise its Official Cash Rate next Wednesday to fight stubborn inflation, or capitulate to the wait and see approach of ‘others’? The NZD/USD should be watched.

2. Caution: Forex remains choppy, U.S Treasury yields have crept slightly upwards, gold is hovering near 2020.00 USD. AMT’s #1 may be the reason why.

1. U.S Data Next Week: Preliminary GDP will be published on Wednesday, and Thursday will present the Core Personal Consumption Expenditures Price Index. The results could create massive impetus in all financial assets.