10. Fusion: The U.S Senate presented legislation yesterday which creates guidelines allowing the Nuclear Regulatory Commission to authorize commercial investment and research of fusion energy. Significant strides are being made in the technology and the U.S government is preparing for the newest developments.

9. Cup of Joe: Your cafe is going to get more expensive. Robusta and Arabica coffee both remain at higher values having hit apex prices respectively this Wednesday and Thursday. And Cocoa remains ‘comfortably’ above 11,000.00 USD per metric ton this morning.

8. United Arab Emirates: The UAE has been hit by heavy weather, suffering its biggest rainfall in 75 years. It was reported that over 14 centimeters of rain fell this Tuesday in Dubai, which is the equivalent to one and a half year’s worth of typical accumulation in the city.

7. India Elections: The vote in the world’s biggest democracy has begun as millions decide on the the Lok Sabha. The election process will take place for nearly a month and a half with the results formally being presented on 4th of June. The Bharatiya Janata Party is expected to win a majority in the House of the People, thus likely re-electing Narendra Modi as the country’s Prime Minister.

6. Gold: The precious metal remains within sight of record values with the price around 2,388.00 USD per ounce. Today’s earlier ratios touched the 2,420.00 vicinity.

5. Cone of Silence: Israel and Iran have remained mum on military counterstrike action scuttlebutt, which was heard this morning throughout global media. The silence from the two nations did not stop the Nikkei 225 Index from dropping over 1000 points upon the news.

4. Bitcoin Halving: A coding change is anticipated to occur soon in Bitcoin which will affect ‘mining’ parameters for the digital asset. The code change will double the amount processing needed to create one BTC, making it twice as expensive for Bitcoin operators. Day traders tempted to wager on BTC/USD over the next couple of days need to be careful. BTC/USD is near 64,560.00 at the moment of this report.

3. Fear Factor: Price of WTI Crude Oil is near 82.70 USD per barrel. Large energy traders continue to show they are experienced in geopolitics, remaining relatively calm as Middle East concerns are being brandished.

2. While Flag: U.S Fed Chairman Jerome Powell conceded that inflation remains stubborn earlier this week. Stagflation is not being discussed openly by the Fed, but it is likely raising concerns among global central bankers. The USD has returned to very strong levels as financial institutions brace for the possibility of U.S interest rates remaining high into the late summer.

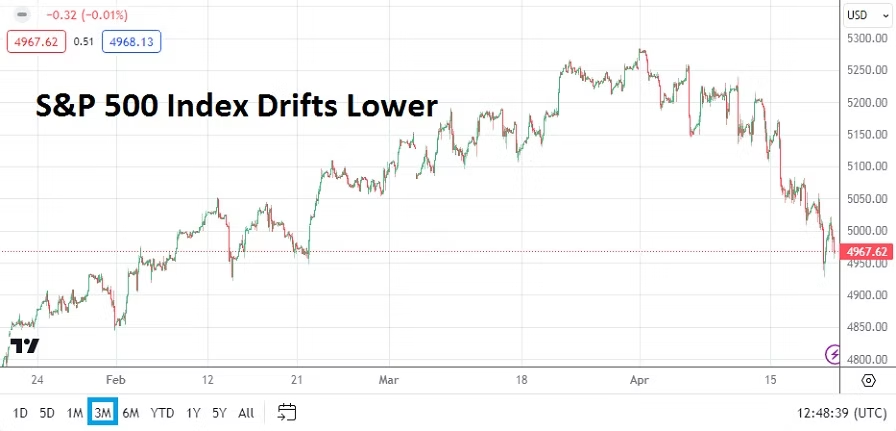

1. Behavioral Sentiment: Equity indices, Treasury yields and Forex are within the midst of nervous seas as central banks and geopolitical concerns create storms. Speculators should make sure they pay attention to the waters they traverse with their bets, which could prove dangerous to navigate in the near-term.