Gold: Not a Love Note but Recognition of Long-Term Importance

The U.S is now starting its second week of the government shutdown. Gold is near $4,190.00 as of this writing, which may be looked on as sign by some that some investors have bought into the precious metal because of a lack of faith in certain things. ‘Certain things’ being written in a way that points out the rather complex mix of perceptions that could quantify into all moving parts causing the bull run.

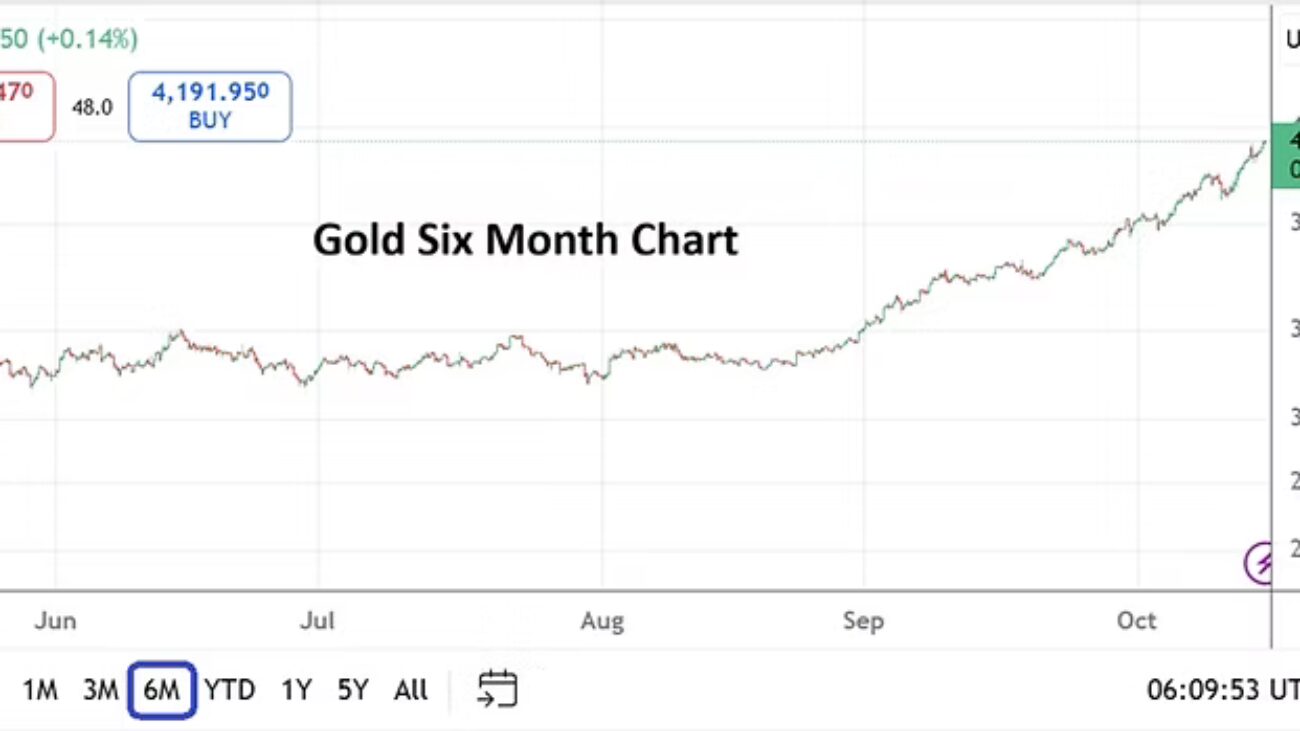

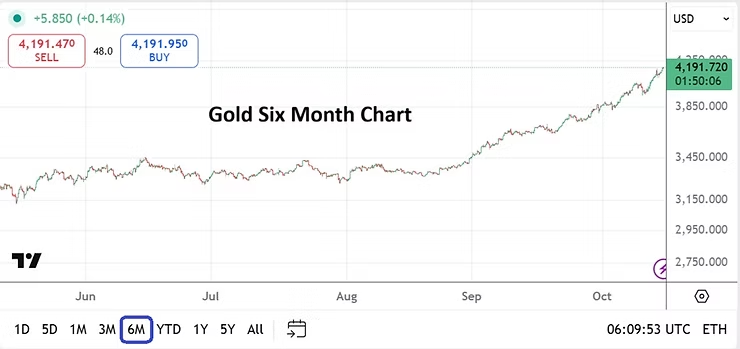

Gold Six Month Chart as of 15th October 2025

If you are a regular reader you will probably have figured out that I do not believe Gold is traversing higher because of a mere government shutdown. The precious metal has seen an upwards trend develop in earnest since the middle of October 2022 when it was trading around $1,640.00. Behavioral sentiment is important within Gold, and this has been the case for almost 6,000 years according to archeologists and historians.

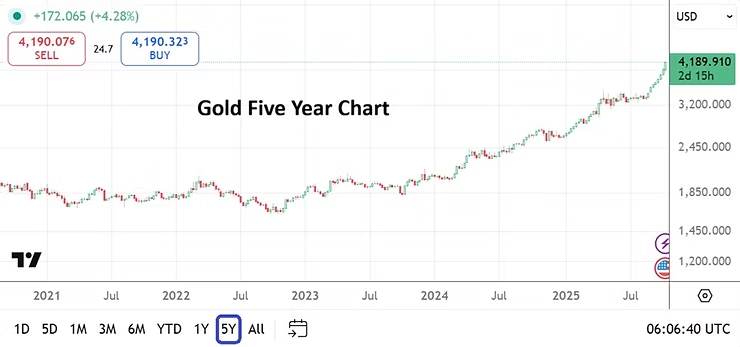

In August 2011 Gold was near $1,900.00. In December of 2015 the precious metal was back to almost $1,000.00. This is written to show that in a little more than a four year period Gold lost nearly half its value in the relatively recent past.

This doesn’t mean I am writing to warn Gold is going to lose half its value suddenly and will be testing $2,000.00 in four years time. It points out that even though the precious metal is considered a hedge against inflation, that speculative elements are fantastically strong when large players buy and sell in unison and can cause periods in which Gold becomes overvalued and then experiences downturns.

Gold Five Year Chart as of 15th October 2025

We have seen this bullish show in Gold before. Milestone numbers are significant in the minds of the public, which often causes the thinking that they should have bought some gold in the past when it was cheaper. But interestingly enough for Gold is that it is almost always considered expensive by the general public. The value of fiat currency is highly correlated to the value of Gold in an unflattering way. While this is an obvious statement for many, it is important to note that we are all looking at the value of Gold while using hindsight.

Yes, I can hear influencers singing in unison in the background ‘do not forget about Bitcoin’, but I ask permission to do so. Hindsight is not always comfortable and I have been proven wrong about the digital currency frequently. However, I still remain somewhat optimistic that my bet on Gold is a better wager compared to Bitcoin regarding value in the future. And by future I mean for all-time. There is not enough foresight to know what Gold will be valued in one thousand years compared to Bitcoin. Yet, I remain much more confident about Gold being around than BTC in a millennium.

People can speak about a debasement of fiat currencies, including the USD. Like it or not the USD remains the dominant go to currency of global enterprise and this is unlikely to change over the next decade. The USD and other currencies are plagued by a constant loss of overall value due to inflation caused by a myriad of reasons. Rising prices in goods are unlikely to suddenly disappear, the costs of commerce and consumer products may start to gradually slow periodically, but the price of things seldom grows cheaper over the long-term.

Yes, the case can be made that by owning Gold it does not serve the economy well, because it is not an asset that is easily spent, but that is an argument for Adam Smith, John Maynard Keynes and Milton Friedman to enjoy in heaven. In the meantime down here on Earth, Gold can be speculated upon, bought and sold, and treated as a precious metal that will likely always be valued highly.

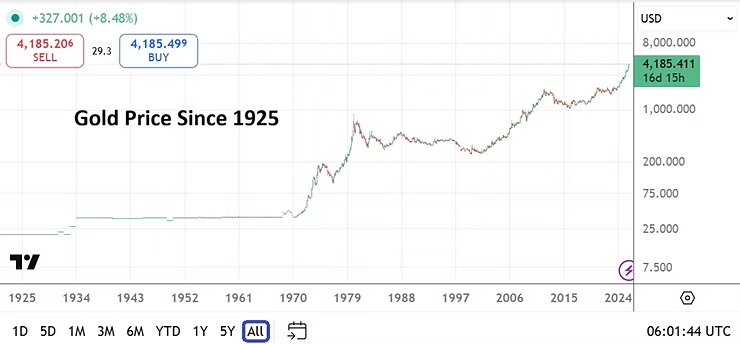

Gold Chart Prices since 1925

This is not a love note for Gold, it is meant as a way to say the precious metal is fairly priced considering the state of the world. $4,000.00 per an ounce of Gold could certainly turn into $5,000.00 in the not so distant future – like six months or one year depending on zeal. Speculative elements certainly aim for targets that psychologically please aspirations.

Day traders as always are faced with a dilemma. Looking for more upside and partaking in the bullish trend is a logical thought and perhaps even wager, but the use of leverage while battling the intraday and intraweek reversals in the marketplace make the ambition of profiting on Gold comparable to time spent at the casino. We know winners talk much louder about their money gained compared to the losers who vanish into the crowd and keep quiet.

So I write this as a warning, Gold may not be worth more one year from now than it is today. However, I will venture forth the notion that in ten years time Gold will be significantly valued higher than it is today. Will inflation suddenly be tamed globally, will confidence in fiat currencies emerge with a strong dose of optimism? No. Certain fiat currencies will do better than others via Forex. However, as a store of value Gold will likely remain an impressive asset to own.

Nervous? Central Banks Cautious, FX and Asset Equilibrium

Sometimes when looking for ideas regarding a risk analysis article it is difficult to find a timely subject. Exaggeration is often used to grab attention. This week and next will not be one of those times. Equities, Forex and commodities have produced nervous results since last Monday. The broad markets appear to be in search of equilibrium, but price velocity while higher than normal hasn’t produced a volcanic surge of pain. Financial institutions were presented less than inspiring jobs data this past Friday and day traders hopefully had their risk management working. Everyone will need to be paying attention this week too.

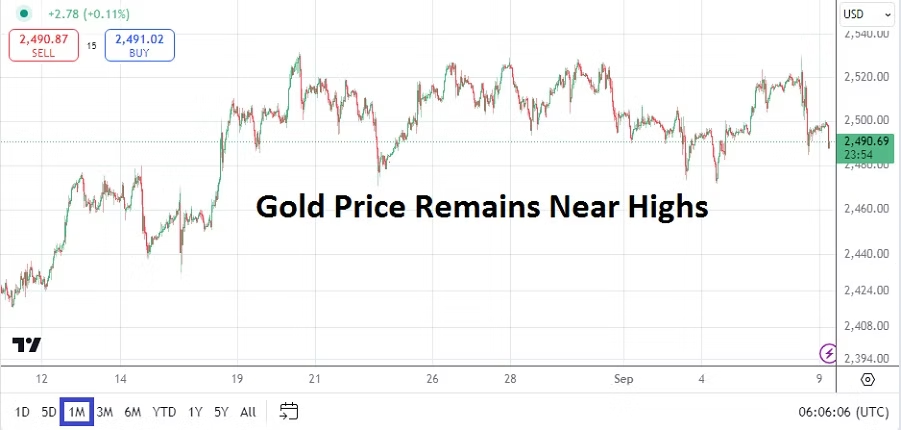

Gold One Month Chart as of 9th Sept. 2024

Gold has hovered around the 2,500.00 level and while it certainly is a short-term speculative asset for day traders, the precious metal also serves as distinct barometer of behavioral sentiment and long-term guidance regarding inflation. Recent economic data has created concerns in financial institutions about the potential for a stronger than anticipated U.S downturn. The volatility and sell off in equity indices last week is a clear sign investors would like the Federal Reserve to be more aggressively dovish.

This coming week is packed with a variety of risk events which will keep all market participants engaged. Long-term investors may feel calm as they rely on their outlooks which extend over a handful of years, but anyone who needs a firm grasp on short and mid-term viewpoints might not be comfortable. It is important not to cry wolf too often, but based on the trading results seen the past week it is worthwhile to point to the turbulent outcomes and issue a warning that more volatility could develop.

Nasdaq 100 One Month Chart as of 9th of Sept. 2024

Some analysts may apply the thought that what we have seen was profit taking, and this can certainly be debated. The coming two weeks have plenty of noteworthy events on the calendar. Besides the listed risk highlights noted below, the Fed will release its FOMC Statement on Wednesday the 18th, the BoE will follow on the 19th and not to be outdone the Bank of Japan will step onto center stage on Friday the 20th of September.

While long-term investors likely believe all variables will return to known price realms and that central banks sooner or later will fall into their proper places regarding monetary policy, day traders who are gambling on short-term momentum must try to figure out where behavioral sentiment is leaning. One of the ways speculators without deep pockets can put the odds in their favor concerning potential profits, is to make sure they are practicing rock solid risk management and not stepping into Forex trades, equity indices via CFDs wagers, and commodities bets when they are displaying rough conditions without being prepared.

Monday, 9th of Sept., China Consumer and Producer Price Index – the inflation reports from China both came in below their estimates earlier today. While some may believe that less inflation than predicted is a good thing, it isn’t when the economy is suffering from deflationary pressures. Lackluster spending from consumers in China continues to highlight negative sentiment about prospects for growth. The USD/CNY is near the 7.1125 ratio as of this writing.

Tuesday, 10th of Sept., U.S Presidential Debate – while not an economic data event, investors might want to pay attention to the answers given by Vice President Kamala Harris and former President Donald Trump. The race for the White House appears to be close according to various polling. It could prove interesting for financial institutions if Harris is questioned about her ideas regarding taxing unrealized capital gains.

USD Cash Index One Month Chart as of 9th Sept. 2024

Wednesday, 11th of Sept., U.S Consumer Price Index data – the inflation reports will certainly get the attention of financial institutions. If the annual CPI report comes in weaker than the previous outcome, this could spark more USD centric weakness in Forex. All asset classes will react to the inflation numbers because they are likely to play a major part in the Fed’s FOMC decision in one week’s time. The USD Cash Index is still lingering near lows, but for it too resume a more bearish trajectory, financial institutions will need to believe the Federal Reserve is going to become increasingly dovish.

EUR/USD One Month Chart as of 9th Sept. 2024

Thursday, 12th of Sept., European Central Bank Main Refinancing Rate – The ECB is definitely going to cut its prime borrowing interest rate, the question is how much of a haircut they are going to provide. A 0.25% cut has certainly been traded into the EUR/USD, but many financial institutions believe there is a possibility to see a 0.50% basis cut. Can the ECB and Christine Legarde be aggressive? The European Union remains under recessionary pressures and inflation data is starting to show signs of erosion. The amount of the interest rate cut from the ECB will also be a telltale sign regarding what will happen via the Federal Reserve on the 18th of September. The EUR/USD will react to the European Central Bank’s decision, and global assets in far off places may react too because behavioral sentiment among investors may shift according to the rhetoric provided. Prediction: The ECB will stay cautious and cut by 0.25%, while saying a November rate cut is likely if economic data remains under pressure. Having said the above, the ECB should cut by 0.50% this Thursday, if they do not – financial institutions will not be pleased unless ECB President Legarde sounds very dovish during her Press Conference.

Thursday, 12th of Sept., U.S Producer Price Index – more inflation data from the U.S will provide investors an other opportunity to glance into the Fed’s looking glass. But if these PPI numbers meet or are near the anticipated results, financial institutions may be reacting to the ECB’s rate decision more because they might believe it is a better clue regarding the Fed’s Federal Funds Rate decision which will come in a handful of days.

USD/JPY One Month Chart as of 9th Sept. 2024

Friday, 13th of Sept., Japan Revised Industrial Production – this number may not get much attention, but because the Bank of Japan will release its Policy Rate on the 20th, the outcome could impact existing sentiment in the USD/JPY. The Japanese Yen has continued its bearish trajectory and traders who are wagering on more downside should not bet blindly on selling positions because intraday trading remains very choppy. The USD/JPY is now touching values last seen in a sustained manner in early January of 2024, lower values were seen in December 2023, and lower ratios that traversed the 138.000 realm and proved choppy occurred in the spring of 2023.

Saturday, 14th of Sept., China New Home Prices, Retail Sales, Industrial Production – this parade of data from the nation will be important. Foreign investors remain concerned about China’s economic prospects. The deflationary winds that have been blowing in the Asian giant have been well documented. The results from these three reports are expected to be lackluster.

Speculative Notions: Gold and the USD as the Casino Lives

Notes on speculation via the prism of Gold and the USD, with questions about value as short-term wagers versus long-term investment are considered.

Speculative forces eventually run out of power, leaving investors and businesses to conduct their affairs via the assets they are using to proceed with enterprise as they judge fair market price.

Assets like Gold (commodities) the USD (Forex) and equities (corporate shares) are a battleground for those who are trying to make short term profits from price action movement (sometimes – volatility) versus those who are holders of the assets in order to run their lives (corporations, private businesses, finance).

Perhaps the speculative forces are not a Las Vegas environment completely, but it is a strange mix of risk management and gambling. And because of the price changes in these assets as supply and demand are transacted – the realization that the potential of hedging against sudden gyrations in price is used as insurance, but also as a dangerous speculative tool needs to be considered.

Futures, options and cash markets combine and are mixed like a stew consisting of trillions of USD value as global enterprise and financial casinos flourish.

Let’s take a look at Gold as an example. There is only so much physical Gold on the planet earth – a finite amount. There is only so much that can be taken out of the ground in a year. There is only so much Gold an individual can safely store in their home, before they have to use other secure venues. Central banks may have backed away from the ‘gold standard’ but they understand the importance of the precious metal as proven and tested by thousand of years of commerce. Gold can be used as the exchange of value for a good and this will likely remain the case for long time.

Gold One Year Chart as of 23rd April 2024

The price of Gold serves as a hedge against inflation. The value of Gold today roughly buys you the same things it bought you a thousand years ago, when compared to monetary units which fluctuate like the wind. Because cash in many cases throughout history becomes weakened, losing its value because of bad government policy which causes the people holding the ‘paper’ to lose confidence; and then creates the desire for the precious metal which has almost entered our conscious DNA as a source of value which doesn’t change.

We can speculate on what the Gold price will be today, tomorrow, next year, but we know the fluctuations will roughly equate into what our consciousness – logic – tells us what the main reserve currency that rules the land will be worth – in this case the USD.

For the time being, the USD acts as the reserve currency of the world and is weighed against the value of Gold – literally – remember Gold is valued per ounce in USD.

The ability of Gold to climb to record highs recently was put into question, because at the same time the USD was getting strong. This signaled to traders that a known speculative force in Gold was at play; yes, it could be said a speculative force was at play in the USD too, because of Forex and the Federal Reserve, but Gold rose the past month and a half dramatically while the USD also was gaining value.

USD Cash Index One Year Chart as of 23rd April 2024

Thus, suddenly the inverse correlation of Gold and the USD which are literally weighed against one another was suddenly off balance. The USD was gaining and gold was rising, and one of them was likely ‘full of hot air’ – an imbalance.

Meaning Gold had become inflated in value perhaps, because of speculative forces. While folks could point to geopolitics, and central banks such as China and Russia and maybe Iran wanting Gold because they are ‘angry’ at the U.S and want to signal they do not believe in the USD. There is only so much money these speculative forces have, and they hold the USD as a store of value too, which means if they bet too much on Gold they can find their positions – weight – imbalanced.

The USD remains the world’s reserve currency, and the value of the greenback particularly as the Fed has come under pressure, via the weight of inflation, and had to admit they cannot cut interest rates until inflation erodes has made the reserve currency stronger again. The use of the USD is easier than using Gold. There is not enough Gold in the world to transact business to business, person to person physical exchange everyday. Thus Gold becomes a ‘store of value’ via inventories not only in secure facilities but our minds too.

The past couple of days have seen Gold perhaps lose value again as the counterweights have come back into focus. It was bound to happen as long as the USD remains the world’s reserve currency in which value can be distinguished versus the commodity.

Speculative forces do run out of power, and now after Gold flirted with the 2,400.00 plus level recently, maybe Gold should return to its values which were seen in late 2023, which is where the USD Cash Index is essentially standing technically. Lets also remember where U.S Treasury yields were during this time, long-term bonds are a measure of interest rates and outlook via the Federal Reserve – used as an insurance and investment vehicle by those looking to lock in ‘returns’. Yes, Treasuries can be speculated on too, but their values coincide with USD legitimacy and the Federal Funds Rate.

It is a thought, a speculative notion, let’s see what happens. What should the speculative price of Gold be now compared to the USD? Should it be lower, closer to the 2200.00 to 2100.00 USD levels? The casino will give us the answers.

Impact: Powell's White Flag, Inflation Data, and the BoJ

Federal Reserve Chairman Jerome Powell’s waving of the ‘white flag’ last Tuesday, when he admitted that inflation was producing stronger than anticipated data had been essentially wagered on since the second week of March by financial institutions. Powell’s speech acknowledging the Fed will find it difficult to cut the Federal Funds Rate in the mid-term (and probably at best not until late this summer) simply verified Forex positions which had already been taken by large players who could afford to make mid-term wagers.

The USD Index has returned to early November 2023 values, and appears able to challenge late September and October prices if inflation data this week causes more volatility, which should put traders of major currencies like the GBP, EUR, JPY and others on full alert. After the USD spiked higher from the 10th to the 12th of April, Forex speculators have seen dynamic action incrementally flirting with stronger USD results the past week and a half.

USD Cash Index Six Month Chart as of 21st April 2024

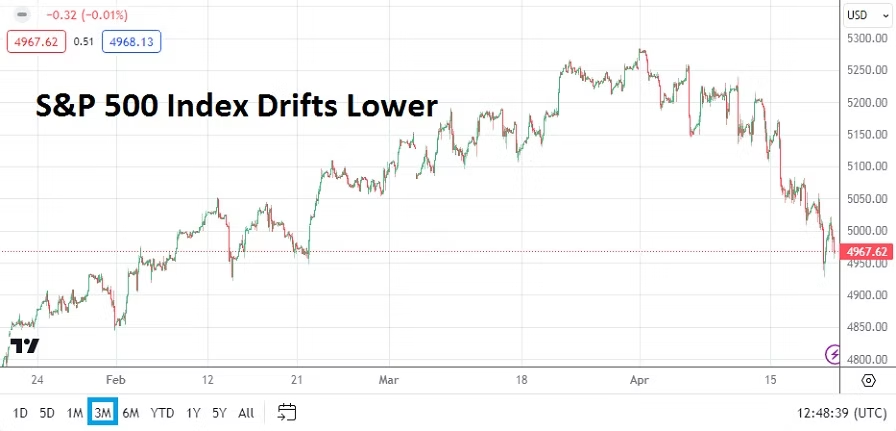

Nervous trading continues to be seen in U.S equity indices. The Dow 30 and the Nasdaq 100 are fighting near ratios they touched in the last week of January. And the S&P 500 is traversing ground from the first week of February.

S&P 500 Three Month Chart as of 21st April 2024

Content

Gold Six Month Chart as of 21st April 2024

Gold remains speculatively high as its hovers near 2,400.00 USD per ounce. The price of the precious metal has not given back its gains made since the start of March and this is intriguing because of the ‘known’ USD inverse correlation, which had proven to work well with the precious metal over the past couple of years but has been stopped in its tracks for the moment. Technically Gold may look overbought, but geopolitical concerns and the prospect that some central banks may be strong buyers could be fueling the rather incremental gains. Retail traders of Gold need to be careful because price action is likely to produce more surprises.

Forex has been turbulent the past handful of months as shifting behavioral sentiment has created choppy conditions. This coming week contains large fundamental risk events via data releases traders should monitor. USD/JPY speculators will also have to contend with the Bank of Japan.

Monday, 22nd of April, China Loan Prime Rates – borrowing costs are anticipated to remain at the current benchmarks. China produced slightly better Gross Domestic Product results last week, but Industrial Production numbers were weaker. Consumers in China remain burdened by decreasing home values and concerns about the economy.

Tuesday, 23rd of April, European Union and U.K Manufacturing and Services PMI – E.U results via the PMI readings are expected to show slight improvements. However the readings from the United Kingdom are anticipated to come in flat. The EUR/USD and GBP/USD will be affected by the results, but the currency pairs will likely remain focused on U.S data later in the day.

Tuesday, 23rd of April, U.S Purchasing Managers Index – the Manufacturing and Services sectors are expected to produce slightly better readings than the previous month. These results will be interesting taking into consideration the Empire State Manufacturing Index numbers last week were bad. The PMI statistics will provide some impetus to the broad Forex market.

Wednesday, 24th of April, Australia Consumer Price Index – inflation data is anticipated to be higher than the previous month’s results. While stronger inflation is not something that will make consumers happy in Australia, stubborn price results may keep the AUD/USD slightly steadier. The currency pair is traversing values last seen in the second week of November 2023 as of this writing.

Thursday, 25th of April, U.S Advance Gross Domestic Product and Price Index – these numbers are certain to have an impact on all financial assets. A decline in growth is anticipated in the U.S compared to the previous month’s result, but the Price Index is expected to show an increase. Jerome Powell having come out last week and said inflation is causing uncertainty within the Federal Reserve, may have a bit of inside knowledge regarding this GDP inflation number and ‘tipped his hand’. If this inflation gauge is higher than anticipated it could pour fuel onto the already volatile USD. All Forex traders need to pay attention to these results and be prepared with solid risk management.

USD/JPY One Year Chart as of 21st April 2024

Friday, 26th of April, Bank of Japan – in what has already proven to be a couple of weeks filled with drama for the USD/JPY, the BoJ will step into the limelight. During their last central bank meeting the Bank of Japan increased the Policy Rate to 0.10%. It was the first time the BoJ hiked interest rates in 17 years. The USD/JPY is trading at values last seen in June of 1990. The Nikkei 225 has come off of recent record heights, but the famed Japanese stock index is also trading within territory seen in January of 1990. Business activity via the Core Machine Orders and the Tertiary Industry data last week were stronger than anticipated.

The Bank of Japan may want to maintain a weaker USD/JPY equilibrium to continue fostering domestic growth. However, many financial analysts have been calling on the BoJ to become more hawkish regarding monetary policy. The interest rate decision is certain to cause immediate volatility before and after the Policy Rate is made public. USD/JPY traders need to be prepared for fireworks. A slight raise of the interest rate seems to be needed, but after the March hike the BoJ may prove conservative again. The 34 year lows now being seen in the Japanese Yen are astonishing.

Friday, 26th of April, U.S Core PCE Price Index, and Inflation Expectations – the data from the government, and the reading from the University of Michigan will close the curtain on a big week of economic statistics for all traders. The USD will react to these outcomes. It should be noted the previous Inflation Expectations data from the University of Michigan caused a storm in Forex when it came with 3.1% gain.

AMT Top Ten Miscellaneous Viewpoints for the 29th of Dec.

10. Book: Cargill: Trading the World’s Grain by Wayne G. Broehl, Jr., a book that folks interested in physical commodities may find interesting.

9. Music: A Night in Tunisia played by Charlie Parker and Miles Davis on The Complete Savoy & Dial Master Takes.

8. NBA: Detroit Pistons have now lost 28 straight basketball games. Will the team get a participation trophy at the end of this season?

7. Post-Quantum: While ‘Artificial Intelligence’ grabs headlines, ‘post-quantum cryptography’ is a phrase and reality that corporations will need to learn increasingly.

6. Behavioral Sentiment: Risk appetite has remained firm during this holiday week, which may spark additional optimistic trading banter in January as trends are wagered upon.

5. U.S Treasuries: Yields have continued to move lower, and dovish outlooks regarding the U.S Federal Reserve inside many financial institutions may increase speculative zeal.

4. Gold: The precious metal remains near highs and the price of 2100.00 USD is hovering above, will this level start to be challenged and penetrated?

3. JPY and NZD: Both currencies remain bullish as they recover from long-term USD strength, this while mid-term price realms are being firmly challenged. Technical traders with long-term outlooks may want to start examining one year charts.

2. U.S Equities: S&P 500 on the cusp of record highs, the Nasdaq 100 is at apex values – while the Nasdaq Composite remains bullish, and the Dow Jones 30 continues to create new heights.

1. 2024: A prosperous and peaceful New Year is wished for all.

AMT Top Ten Miscellaneous Shots for Friday the 3rd of Nov.

10. NBA: Welcome to Victor Wembanyama’s world. VW’s 5th game as a Spur was historic last night.

9. South Africa: The Springboks Rugby World Cup victory is helping unifying the nation and giving all its citizens a hope for better days.

8. Book: The Gulag Archipelago by Aleksandr I. Solzhenitsyn.

7. Crypto: Sam Bankman-Fried found guilty on all counts. Yet, Bitcoin is near 34,600.00 USD per coin.

6. Risks: Signs of appetite as U.S equity indices have moved higher, and U.S Treasury yields have declined.

5. Gold: The precious metal still lingering near 2000.00 USD and may attract bearish speculative positions.

4. Middle East: Global financial institutions appear to have dealt with the noise.

3. U.S Jobs Reports: Non-Farm Employment Change numbers and Average Hourly Earnings inflation data will be published today and shake markets.

2. Federal Reserve: The U.S central bank may have reached the end of it interest rates hikes cycle.

1. USD: The world’s reserve currency remains suspiciously strong and if it is a relatively calm today and this weekend, day traders may begin to embrace selling wagers.

Friday Barometer Regarding the BoE Decision and Gold Prices

The Bank of England’s rate hike of 0.50% cements the notion that global central banks remain steadfastly locked on inflation, and understand politically the implications on the public regarding higher consumer prices which are being experienced. The Bank of England ‘met’ before its Official Bank Rate announcement with corporate bank executives it was whispered, to discuss their concerns regarding the knock on affects of higher mortgage rates to come. However, this did not stop the BoE from being aggressive.

GBP/USD Three Month Chart as of 23rd June 2023

Is the BoE Move a Sign Regarding the Fed’s Next Decision?

The move by the BoE also is intriguing because the larger than expected hike puts into play the notion the U.S Fed may be raising the Federal Funds Rate in July. The reasoning is based on the idea the Bank of England wants to protect the British Pound from another interest rate hike from the Fed, thus ‘securing’ the value of GBP/USD Forex mechanics.

The U.S Federal Reserve, the BoE and ECB finally seem to have a grasp on import inflation implications. Although higher costs and dynamic pressures on exporting countries like China, India and others that face the gauntlet of these challenges remains critical, because these nations need to raise the costs of manufactured goods internationally when they sell.

Smart Money and the Value of Gold

Let’s talk about ‘smart money’ for a moment surrounding Gold – and please try to hold down your laughter – but the price of the precious metal is interesting and should be monitored even by folks who do not trade the commodity. Gold as of this morning is near the 1915.00 USD ratio.

Gold Six Month Chart as of 23rd June 2022

On the 4th of May the price of the precious metal momentarily challenged the 2080.00 level. On the 1st of June the price of the commodity was near 1985.00. Do you see a trend here? Please note, Gold isn’t going to zero.

The point to be made is that the build up in the price of the precious metal from the 22nd of November 2022 when Gold was around the 1625.00 USD per ounce level, until early May anticipated the U.S Federal Reserve was going to become more dovish regarding their interest rate polkicy. For consideration look at the price of the USD during this time too, against many major currencies – the value of the USD also started to come down.

‘Smart money’ is showing signs of nervousness certainly since the start of June that more hikes are feared from the Federal Reserve. However, the price of Gold and the USD are not correlating well at this moment. This is a potential sign that Gold and the USD are both within speculative trading zones in which financial institutions are seeking ‘true’ equilibrium and are not comfortable. Fragility in the financial marketplace is likely to be seen until the Federal Reserve Federal Funds Rate announcement late in July. Expect financial institutions to price in their outlooks respectively depending on their outlooks.

Gold and U.S Treasuries: Inverted Interest Rate Implications

Gold definitely fluctuates within daily trading conditions, it is a speculative commodity, but it is also a solid barometer of risk management among the elite. If financial institutions are in favor of buying items like U.S bonds because of their guaranteed short term interest payments (look at the fact U.S Treasuries are mostly inverted – meaning shorter term bond interest rates are paying higher returns compared to longer term bonds) instead of buying Gold as an investment tool.

The Gold and USD Forex dynamics tells us that investment institutions are still very nervous about the Fed potentially raising interest rates a couple of more times this year. July and late this year appear to be reasonable bets. This Fed consideration and concern remains legitimate while looking forward as long as inflation remains elevated in the U.S. However, the Federal Reserve must also feel comfortable they will not kill mid and small sized banks, which by now should have shifted their business practices allowing for slightly higher interest rates to be delivered.

Anticipated Federal Reserve Shop Talk to be Delivered Today

For what it’s worth, here is my prediction regarding what the Federal Reserve will do today. The Federal Funds Rate will remain unchanged in my opinion. The FOMC Statement may show that the vote actually was debated and not unanimous. The statement is likely to warn that inflation remains stubborn and potentially problematic, meaning the Federal Reserve continues to believe it may have to raise the Federal Funds Rate over the mid-term and again before the end of 2023.

The Forex market has seen the USD get weaker against many major currencies since late May. While financial institutions have seemingly positioned for no increase from the Federal Reserve today, this move has also likely been priced into Forex. Day traders need to understand institutional traders will not be betting on what took place the last three weeks, but are trying to anticipate what will happen into early July and beyond regarding their Forex positions.

GBP/USD One Month Chart as of the 14th June 2023

Many financial institutions may still be betting the Fed will remain more dovish than the U.S central bank wants to admit, but this is a dangerous perception and could prove costly. Financial institutions are concerned about the Fed because they know the central bank has painted itself into a corner it may not be able to maneuver freely within. The battle to conquer inflation while trying to fuel economic growth is not an easy one. Mixed sentiment abounds regarding the U.S economy depending on who is asked.

Talk of a soft landing and a small recession continues to be heard, this while some analysts warn about a hard drop and darker days ahead. Folks, it is all about timelines and their interpretations, experts warning about brighter or darker days ahead have a tendency to be vague regarding exact moments in time. Everyone has an opinion, and people often have more than one.

In my opinion – my one opinion, the Fed is likely to say that it is not going to raise rates today, but may have to do so in the mid-term. If these were normal times and economic conditions were not suffering from huge spending running amok in Washington and the corporate banking sector wasn’t fragile, the Fed may actually have raised the Federal Funds Rate today to continue to battle inflation deliberately. However, a pause for the moment seems like the logical choice, this while ‘hoping’ inflation continues to diminish. And hope is a key word here. Everyone seems to be hoping. The question financial houses and traders need to decide after the FOMC Statement takes place today is how seriously do they consider the Fed’s remarks.

If they believe the Fed will have to continue to remain neutral regarding its mid and long-term interest rate policy, the USD may soften and incremental selling might be demonstrated. Human instinct tends to be optimistic, which means financial institutions and maybe even the Fed wants to believe inflation will ebb lower. If this happens the USD would weaken further. However, the Fed may have to sound more aggressive than people want, but that would damper the mood of financial institutions – so look for optimistic interpretations to abound with rose colored glasses, even if they are wrong in the long-term.

Gold One Month Chart as of the 14th June 2023

For evidence of outside barometers, traders may want to look at Gold which has essentially traded between 1940.00 and 1975.00 with a few outliers since the last week in May. The price of Gold has seemingly situated within a consolidated framework the past few weeks. The precious metal may produce a strong move if the Fed shows more dovish behavior today, particularly if financial institutions show more optimism via behavioral sentiment in Forex – meaning if a weaker USD trend continues momentarily Gold could traverse higher.

My prediction and $1.00 USD may get you on a bus. As always caution will be needed if you are trading immediately before and after the U.S Federal Reserve’s rate decision. I advise using a seat belt today consisting of entry price, stop loss and take profit orders via solid risk management, but then again these cautious attitudes should always be practiced by day traders.