AMT Top Ten Miscellaneous Ruminations for the 31st of May

10. Absence: Apologies for the truancy of AMT’s Top 10 the past handful of months. The staff has offered a myriad of poor excuses, but it accepts responsibility and has promised to try and meet the standards of our readers with timely publication once more. More coffee has been promised to the staff as a negotiation tactic by management, even though the price of the beverage is obscene.

9. Dim the Lights: President Cyril Ramaphosa, his staff and well known South African golfers attended a highly publicized meeting in the White House with President Trump. After surprisingly dimming the lights, a video mainly consisting of EFF radical Julius Malema’s threatening escapades was shown while Trump voiced concern about attacks on farmers. Not a lot is known about the outcome of talks which went on behind closed doors afterwards, but speculation abounds. The USD/ZAR is near 17.97000.

8. Anduril Industries: An aviation company, cofounded by Palmer Luckey who at a young age created Oculus VR, is receiving important attention. Anduril is a privately held company intent on building pilotless jet fighters, among other innovative technologies. Palmer Luckey is now 32 years old and appears ready to become a transformative tech entrepreneur perhaps in the vein of Elon Musk.

7. Bitcoin: Value of BTC/USD is near $103,600.00 at this moment. GameStop has announced it has purchased Bitcoin as a form of corporate treasury, apparently following the path of MicroStrategy’s foray as a Bitcoin proxy to the dismay of some and delight of others. The price of the world’s biggest digital asset was nearly $75,000 on the 7th of April 2025.

6. TACO: An acronym meaning ‘Trump always chickens out’, created by Robert Armstrong of the Financial Times, has caught the attention of many, including President Trump. While an amusing and pointed term, the context should be considered as a way to monitor the thinking of behavioral sentiment of anxious investors. Trump’s tough rhetoric and tendency to then issue a softer toned stance has been noted before by his backers as well as critics. As a means of accumulation while seeking value in assets perceived to be oversold, TACO may be a useful tool for those who agree with Armstrong’s thinking.

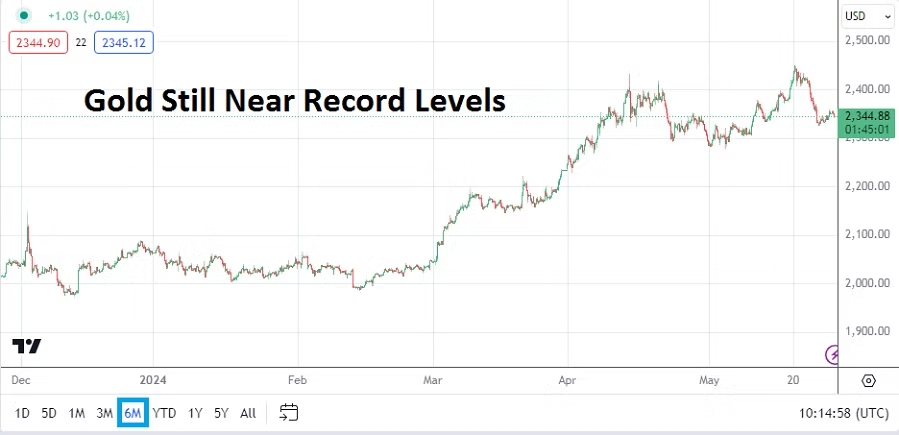

5. Values: Gold went into this weekend near $3,288.00. After achieving an apex around the vicinity of $3,500.00 on the 22nd of April, speculative fever has subsided a bit, but the commodity remains stubbornly in demand. Inflation in the U.S appears to be under control. Yesterday’s Core PCE Price Index met expectations with a monthly outcome of 0.1%. WTI Crude Oil’s spot price finished near $61.05 on Friday showing large traders remain convinced supply is strong.

4. Paralysis: The Fed remains steadfast and scared. While using the word ‘uncertainty’ repetitively – as if part of a rave song, Federal Reserve Chairman Jerome Powell must contend with official U.S inflation data which is starkly lower and a discontent Donald Trump, this while trying to explain the comatose behavior of the U.S central bank. The Fed should cut the Federal Funds Rate asap. And a 50 basis point cut by the end of this summer should be the discussed target.

3. Leviathan: The White House’s goal of reducing the deficit is running into tough political realities as budget cutting hopes clash with entrenched bureaucracy that swallows money like a hungry sea monster. U.S Treasuries yields remain elevated. The U.S has been cautioned again via rating services – highlighted by Moody’s recent downgrade of U.S bonds. To the chagrin of many fiscal conservatives, U.S government spending remains problematic.

2. Intimidation: Apocalyptic economic headlines attract viewers. Proclaiming global catastrophe creates attention and reactions in global financial markets. However, after the fierce selling seen in equities over the past few months, there has also been plenty of resilience and indices are now showing signs of coalescing as outlooks improve. Value and yields remain a prime motivator for experienced investors.

1. Pundits: Day traders have been battling volatile market storms since the election of Donald Trump, this as financial institutions have shown a tendency to shift outlooks as they react to pandemonium and cause whipsaw price action. Many speculators have experienced costly losses. Listening to self-anointed experts has not helped. Be wary of anyone who claims to be a market guru, and remember some call themselves gurus simply because spelling charlatan takes too long.