10. Formula One: The Miami Grand Prix race will be held on Sunday. Whispers have been heard that Red Bull driver Max Verstappen has been approached by Mercedes bidding an annual contract over 150 million USD, but that he has not accepted the offer. However, Adrian Newey, engineer and CTO of Red Bull Racing, has confirmed he is leaving the team after 19 years of leadership. F1 certainly needs more competitive racing, a shake up at Red Bull could deliver this for the sport.

9. De-movements: Desire for decolonization, decarbonization, depopulation, turned into delusion and dehydration for Columbia University protestors and the need for a glass of water per the request of a student leader. Perhaps de-escalation is next.

8. Geopolitics: The nation of Georgia is dealing with demonstrations as some citizens show disdain regarding feared political influence from Russia. Georgia has an approximate population of 3.7 million. The East European and West Asian country has seen civil disobedience on the streets of Tbilisi increase this week.

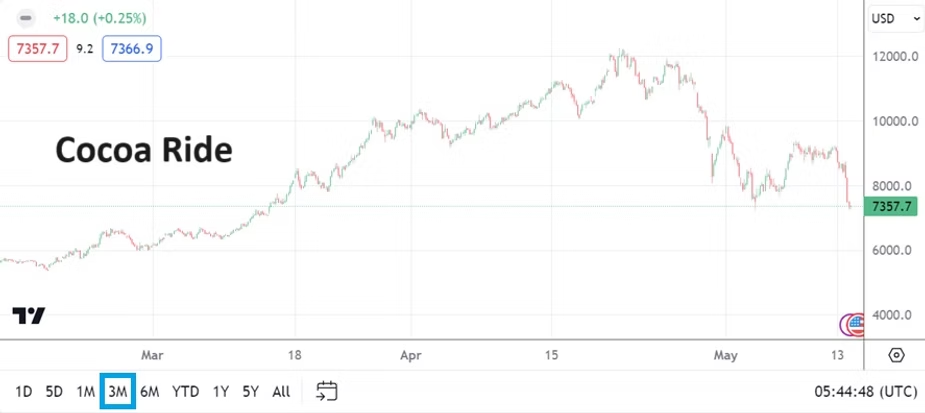

7. Lower Values: Cocoa is near 7,658.00 USD per metric ton as of this morning, on the 19th of April it traded above 12,000.00 briefly. BTC/USD is around 59,250 after having faced headwinds this week.

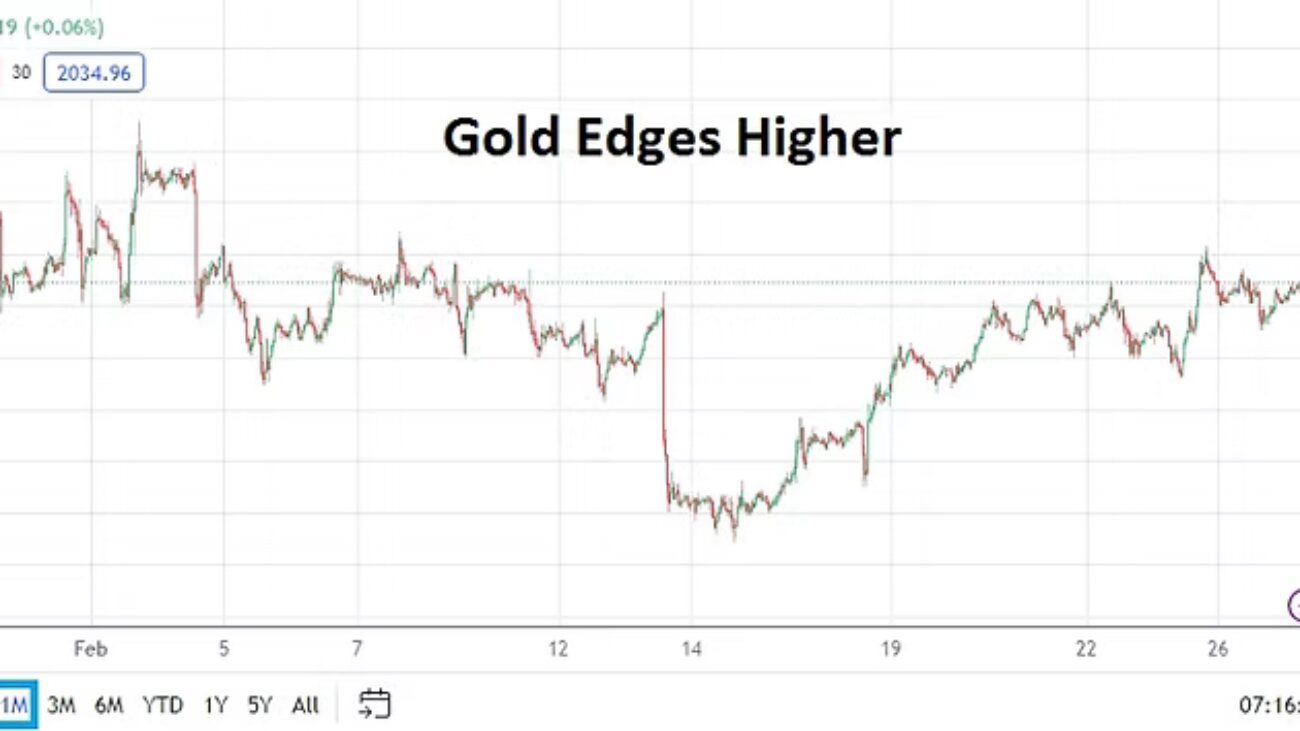

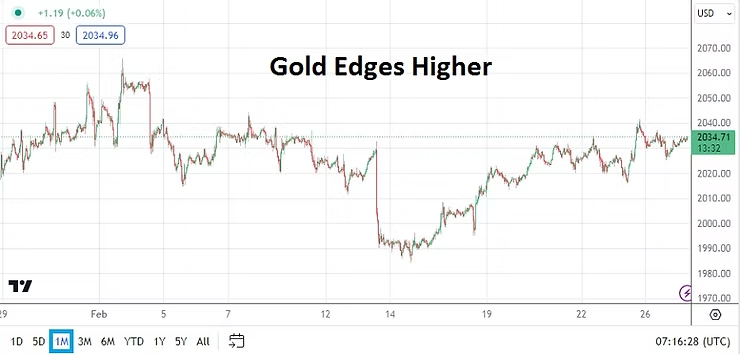

6. Gold: The precious metal has sold off this week and is hovering near 2,300.00 per ounce as concerns build about USD outlook remaining strong over the mid-term. A low of nearly 2,282.00 was seen on Wednesday. Today’s publication of U.S economic data will push the price of Gold around.

5. Mixed Trading: Equity indices have produced uneven results this week as investors try to find equilibrium. Optimism almost always is the eventual emotion long-term institutional market participants lean towards. The S&P 500, Dow 30, and Nasdaq Composite all gained yesterday, but remain below highs from earlier in the week. Behavioral sentiment appears fragile and many Fed observers are disgruntled.

4. Uncertainty: The Federal Reserve has admitted it is unsure about future economic progress this calendar year. When questioned about the potential of stagflation Fed Chairman Jerome Powell said he see no signs of this – while forgetting to add that politically saying such a thing would likely cost him his job. And lets remember, the Fed claimed they thought inflation was transitory in July of 2021.

3. Bank of Japan: A battle is underway with the USD/JPY as the BoJ has staged two interventions this week. Intent on trying to create economic growth via stronger exports, while allowing import inflation to be seen, the BoJ interest rate policy remains dovish. The USD/JPY is near 153.230 now, but it is unlikely to go into the weekend with this price. An apex on the 29th of April approached the 159.610 ratio. Financial institutions and Japanese Yen traders must remain alert.

2. High Anxiety: Day traders in Forex, equity indices and commodities have certainly seen heightened volatility and the choppiness is going to persist. Retail brokers will welcome speculators with open arms and point to opportunities, but traders need to understand the ‘casino’ often is making money via losses incurred because of leveraged wagers which turn into losing bets when price velocity hits.

1. Jobs Data: Yet another opportunity for inflation to be seen today via the Average Hourly Earnings numbers. A cautionary road sign was seen this Tuesday when the U.S Employment Cost Index came in with a stronger than anticipated quarterly gain of 1.2%. The USD will remain a lynchpin in many financial assets, and Treasury yields should be watched after the employment statistics have been printed.