AMT Top Ten Miscellaneous Frights for the 28th of October

10. MLB Concern: Baseball executives are hoping the Yankees can start to make the World Series more competitive this evening. The Los Angeles Dodgers have won the first two games of the championship battle. Significant hopes for a drama filled, seven game World Series would be dampened badly if the Yankees do not win tonight. Television ratings which were expected to be high could suffer appreciably if the Yankees go down three games to none. A non-competitive championship would mean a loss of revenue.

9. Israel and Iran: The Middle East saga is at number nine, and hopefully doesn’t become number one. A dangerous game of poker is being played by the participants. If Iran decides to up the ante once again, it would be a dangerous decision, because it appears Israel has positioned itself via this weekend’s retaliation to be more aggressive if need be.

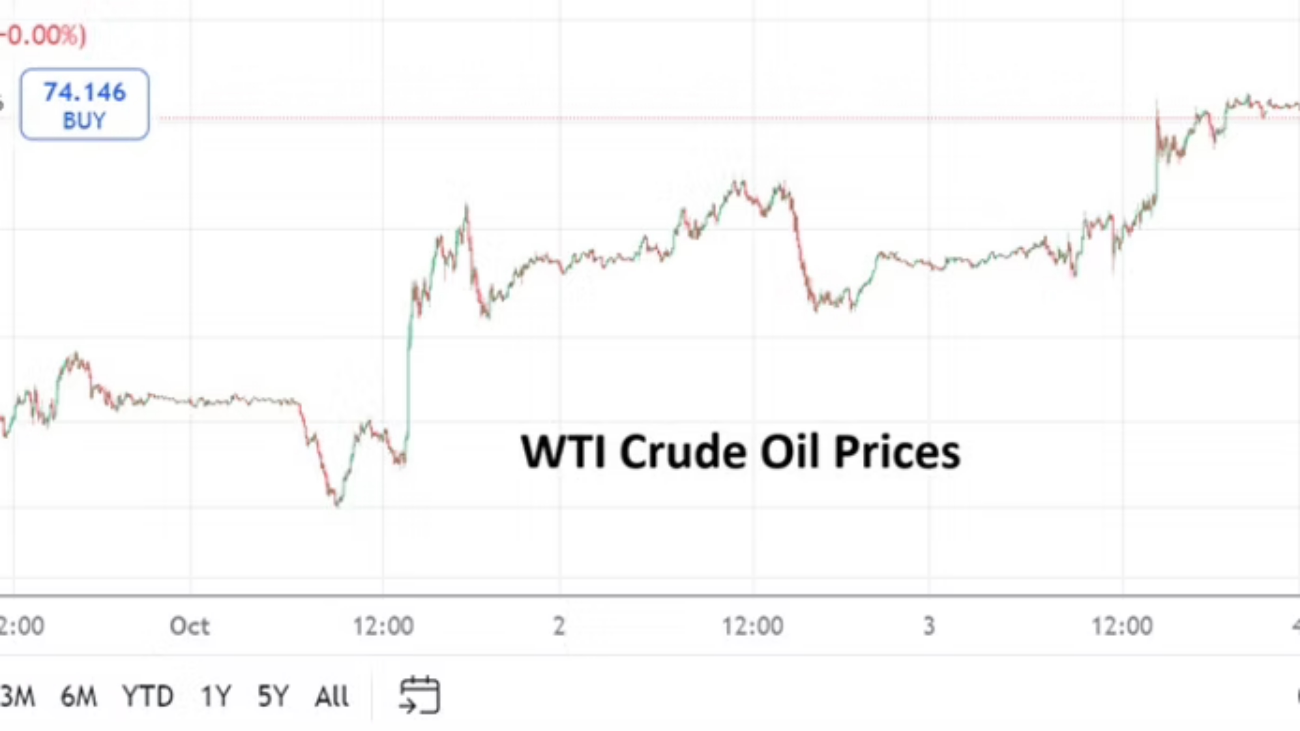

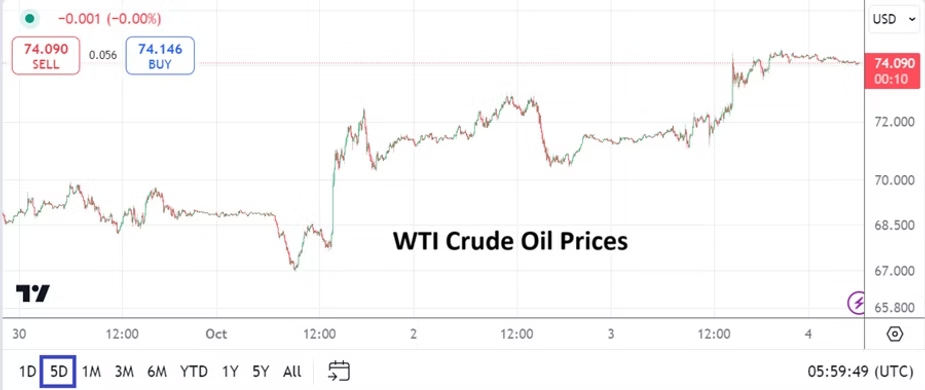

8. WTI Crude Oil: The ability of the energy to move below 70.00 USD upon this morning’s trading is a sign the Middle East conflict remains tranquil in the minds of large participants in the oil sector. However, if Iran decides to test Israel again directly, Iran may find that its oil infrastructure is vulnerable. As the price hovers below 68.00 USD during this writing, it appears buyers who bought speculative positions the past few weeks might be capitulating.

7. BRICS: The inclusion of 13 additional nations as Partner States to the international organization led by Russia, China and India shows the entity sees itself as a growing alternative geo-political force and trading sphere with real power. The West should be paying attention, but often seems like it is not concerned about the potential strength of BRICS, and instead makes believe the group is a fallacy and much ado about nothing – this is a mistake by the West.

6. North Korea: The potential of North Korean combat troops entering the Ukraine – Russia war is a dangerous notion. However, it opens the door for Ukraine and South Korea to offer surrendering deserters the possibility of being allowed into South Korea, if soldiers can prove they are not spies. Unfortunately, the temptation of desertion by enemy troops could prove to be wishful thinking because North Korean soldiers will have intense supervision at all times; the threat of being shot as a liable traitor is a likely constant menace.

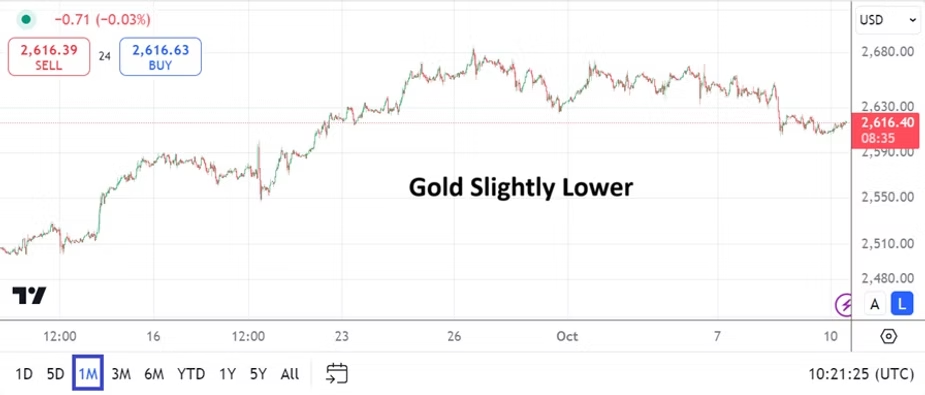

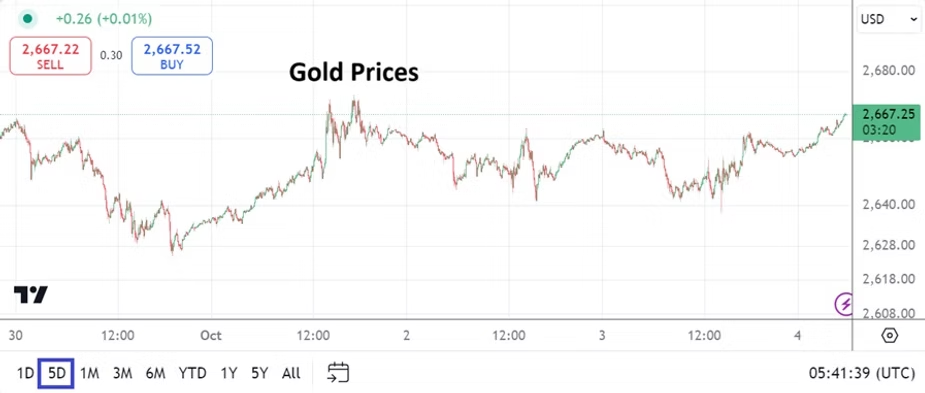

5. Gold: Record values continue to be seen, the price of the precious metal as of this writing is near 2,732.00. Noted as a store of value, gold is also seen as a safe haven by its buyers. Now may be the time to consider behavioral sentiment as a main driver because of anxiousness in the global marketplace. Speculative forces are certainly involved in the move higher too. With so many risk events shadowing, it may be very unwise for day traders to bet against the rise of gold near-term.

4. U.S Data and the Fed: Advance GDP numbers will be published this Wednesday, the Core Personal Consumption Expenditures Price Index will be seen this Thursday, and on Friday the Non-Farm Employment Change statistics will be presented. Fireworks should be anticipated by day traders. The combination of these reports, the approaching U.S election, and the Federal Reserve’s FOMC Meeting decision on the 7th of November will be enough to make most analysts hearts beat faster.

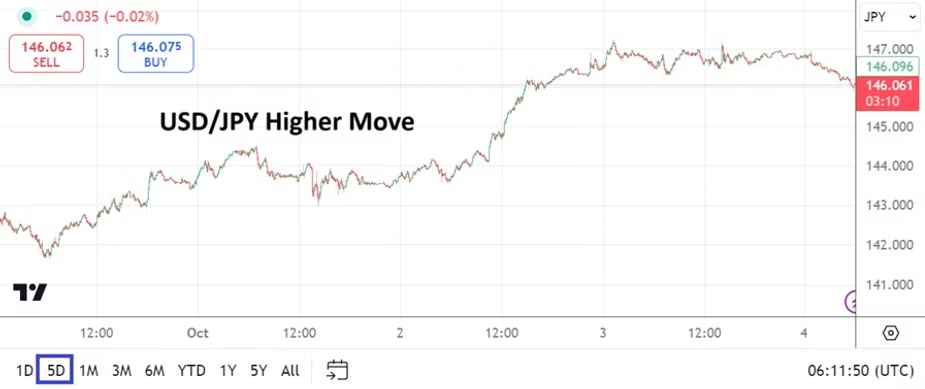

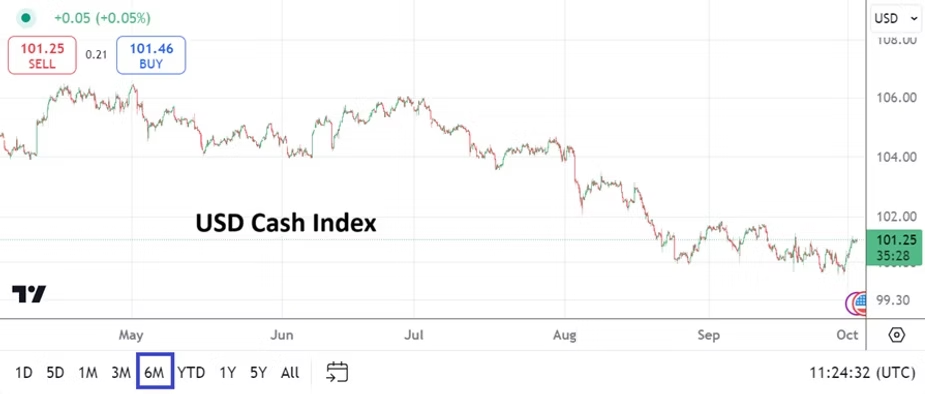

3. USD/JPY: Japan’s election results today now require a coalition government because the ruling Liberal Democratic Party has lost its majority. The Bank of Japan has a meeting this Thursday and is expected to hold its BoJ Policy Rate in place. The Japanese Yen has returned to values above the 153.000 level as of this writing. While many major currencies have lost value against the USD since the end of September, the USD/JPY needs to be watched as a dynamic combination of risks abound. Political gridlock, inflation, and lackluster economic data in Japan are not ingredients which will provide financial institutions with optimism in the near-term. The historically cautious attitude of the Bank of Japan will be severely tested in the coming weeks.

2. U.S Election: There is a little more than one week to go before the Presidential vote begins. While many folks are focused on the White House, the race for the Senate looks to be a stiff competition too. Republicans are hoping to regain the majority in the Senate and retain their power in the House of Representatives. Financial institutions are apprehensive about the outcomes for Congress, which will have an important role in fiscal and regulatory management. The Democrats appear to be nervous. Noise from the campaign trail and media will become heightened over the next seven days. Top bureaucrats in offices like the SEC, CFTC, FCC and other agencies know their jobs are on the line.

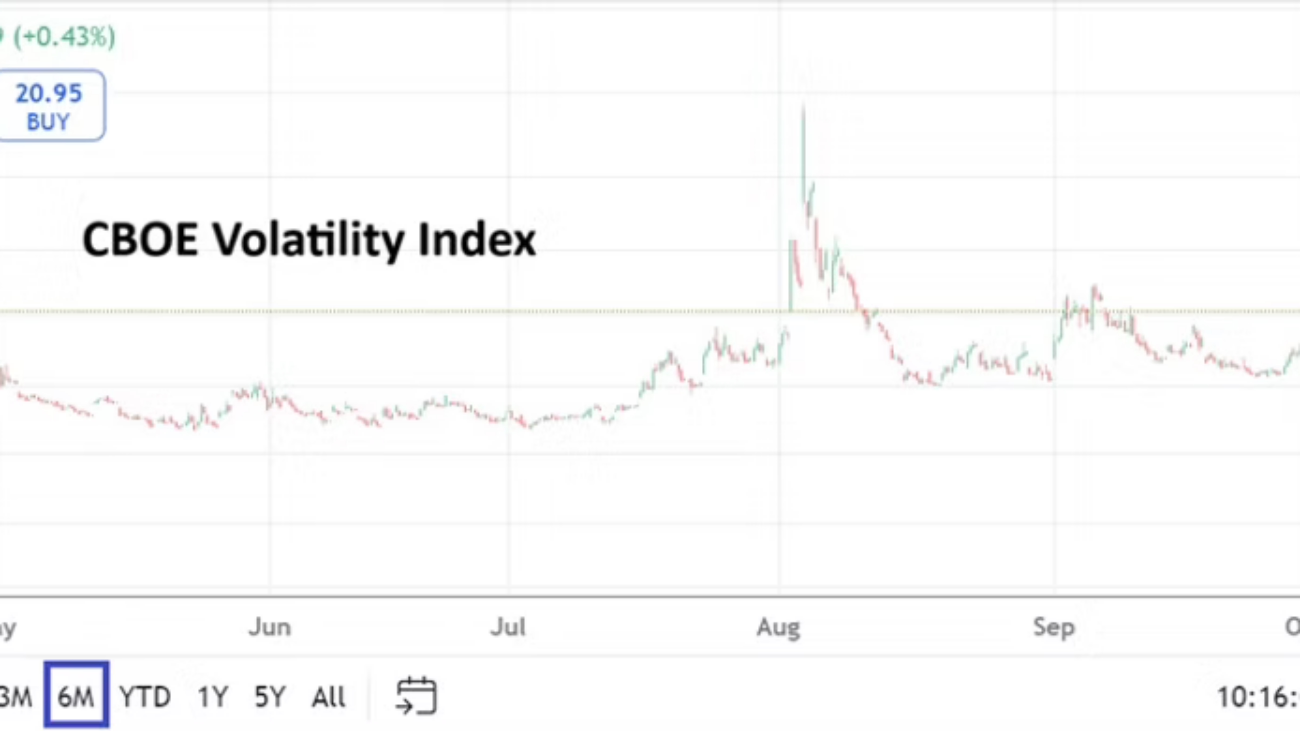

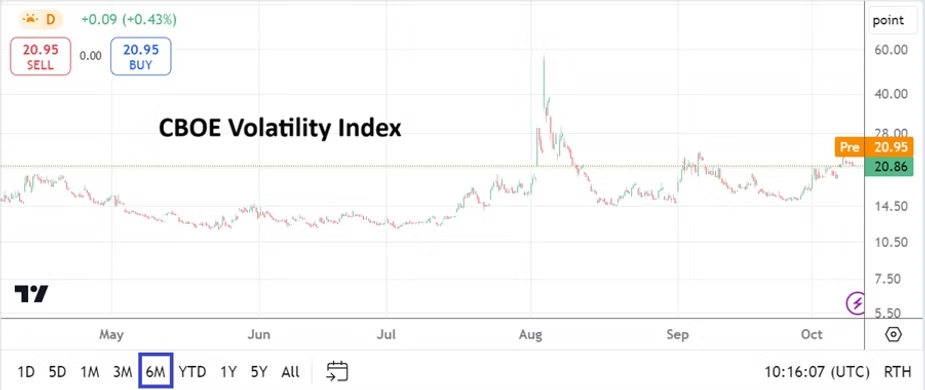

1. Market Volatility: U.S economic data, the coming election, and the Fed means the next week and a half of trading in the global markets are going to be packed with violent firework displays. Day traders who do not have experience should watch from afar, because the coming price action can cause fast losses for those caught on the wrong side. Trading sentiment is fragile, this is evident via the choppy results seen in equities, Forex, many commodities, and rising U.S Treasury yields. Over stating the obvious for the moment about risk management is a public service.