China and U.S Data Early and Important as Central Banks Fret

Monday, 17th July 2023, China GDP and Industrial Production – the economic numbers coming from China have shown steady signs of a downturn. Gross Domestic Product figures however are expected to increase this month, but some analysts may question transparency issues regarding the reported statistics. Industrial Production numbers are expected to fall, which on the surface may cause people to question any positive results from the GDP. Retail Sales will also be published on Monday. The housing market in China remains critically important in the nation and some borrowers appear to be suffering financial stress. While many global retail traders might not be invested in China, the nation serves as a good barometer for the world’s economy, particularly regarding consumer demand.

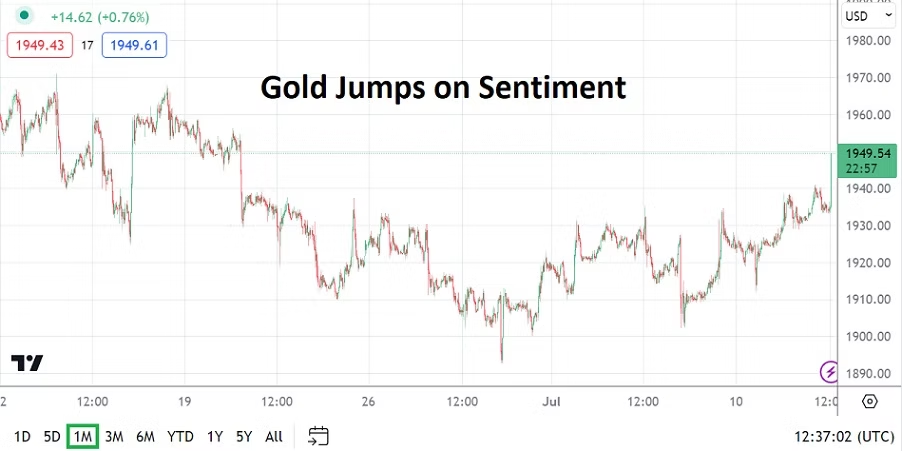

Monday, 17th July 2023, U.S Empire State Manufacturing Index – the New York based report is expected to have a negative reading. It should be noted June’s data came in stronger than expected. Another positive surprise outcome would continue to show economists are finding it difficult to gauge the U.S economy. Last Friday’s solid Consumer Sentiment reading from the University of Michigan highlighted the rather complex results from the U.S, weaker than expected inflation numbers are also factoring into a muddled sentiment. However, the Federal Reserve is still believed to be leaning towards another interest rate hike on the 26th of July. Day traders should remain alert.

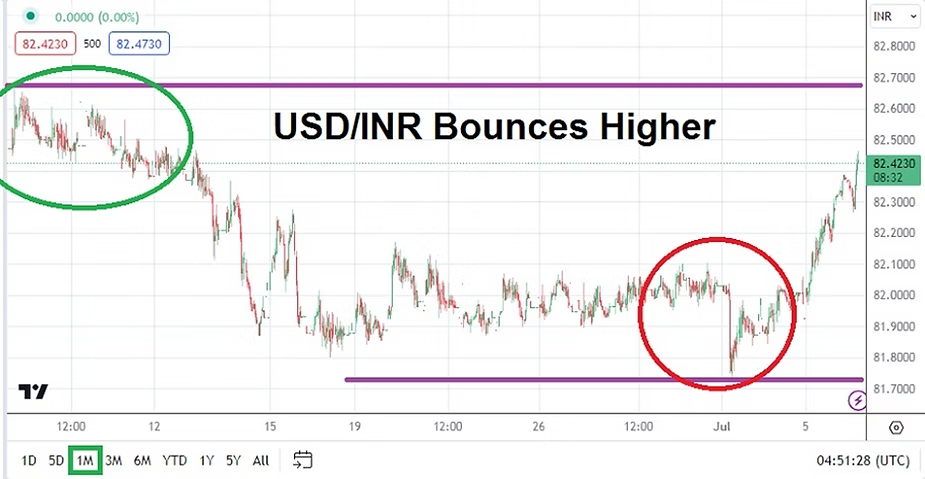

Tuesday, 18th July 2023, Canada Consumer Price Index – the inflation numbers from Canada are expected to show a slight decrease in the velocity of rising prices. The numbers are likely to affect the USD/CAD which is trading near lows last challenged in September of 2022.

Tuesday, 18th July 2023, U.S Retail Sales – considering last week’s improved Consumer Sentiment numbers recently from the States, demonstrating better retail results compared to last month will not be a surprise. Earnings season on Wall Street gets underway this coming week and solid Retail Sales numbers may help mid-term outlook regarding equities. However, behavioral sentiment is fragile.

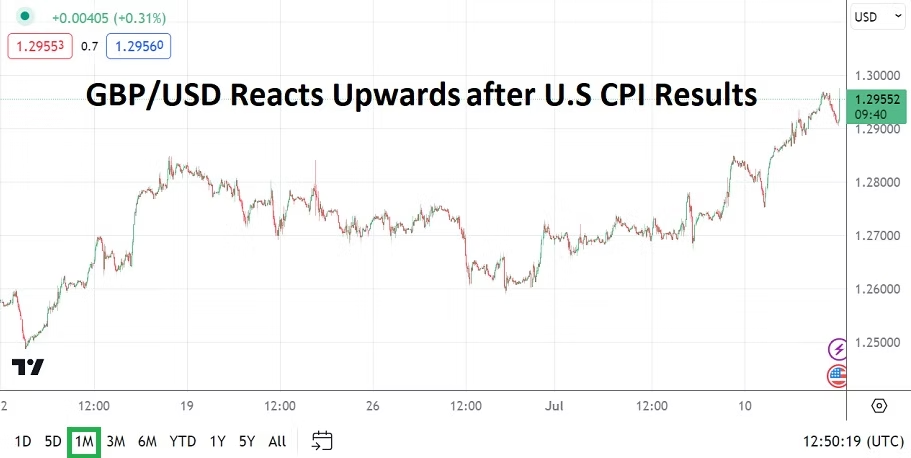

Wednesday, 19th July 2023, U.K CPI – the inflation numbers from Britain are expected to show a slight decrease in the rate of price expansion, but any result above 8% via the broad data will not make many folks feel better. GBP/USD speculators should monitor the reports.

Thursday, 20th July 2023, U.S Existing Home Sales – the rising costs of mortgages in the States is having an effect on the marketplace. Signs of stress in housing is an intriguing barometer regarding the outlook for the American economy. Better Consumer Sentiment and Retail Sales mixed with less than glowing numbers from the housing sector could make for a troubling diet for traders to consider and act upon.

Friday, 21st July 2023, U.K Retail Sales – recessionary results are shadowing Britain. Poor results from the retail sector would not help behavioral sentiment, particularly if inflation numbers have continued to show they are unrelenting two days before. The Bank of England is in an uncomfortable spot, this as the GBP/USD trades near highs it last saw in April of 2022.