AMT Top Ten Miscellaneous Battlefronts for the 7th of Sept

10. Cape Town: Springboks take on the All Blacks in Round Four of the Rugby Championship later this afternoon. South Africa won last week’s test. Roster changes have been made to both starting squads. Springboks Captain Siya Kolisi will start, this after he had been listed as questionable earlier this week because of a nose fracture he suffered in last Saturday’s game, which will be dealt with surgically in the near future. The All Blacks are extremely difficult to beat two games in a row, today’s match could be a firecracker.

9. Spy Games: Alleged China spy Linda Sun is accused of trying to influence policy while working in New York Governor Kathy Hochul’s office as an aide. The alleged spy also worked in the previous New York administration under Andrew Cuomo. Sun and her husband, Chris Hu, have been charged by the U.S government to be in violation of the Foreign Agents Registration Act amidst a litany of alleged illegal activities.

8. VPN Wanted: Brazilian Supreme Court Justice Alexandre de Moraes has suspended X because of claims the social media service, previously known as Twitter, is allowing ‘misinformation’. Justice Alexandre de Moraes has broad powers and is permitting Brazil’s ruling government led by Lula da Silva to walk a perilous line that does not allow for free expression. Brazil has not heard the last of Elon Musk.

7. Boeing: Starliner returned to earth last night touching down in New Mexico, but without the astronauts it delivered to space in early June. The mission was supposed to take 8 days, but instead stranded the two astronauts on the International Space Station. NASA has stated it was potentially dangerous for the astronauts to return in Starliner. The astronauts are now scheduled to return in February 2025 with SpaceX. Starliner is owned by Boeing. This time last year Boeing’s share value was near 219.00, as of yesterday it is 157.62 USD.

6. Xmas in October: Nicolas Maduro, the Venezuelan President (dictator), has announced the Christmas holiday will be celebrated on the 1st of October, allowing Venezuelan citizens an early celebration in order to forget the troubles imposed on the nation by foes who are working against the socialist government. Maduro joins a well established line of totalitarian leadership who have historically moved or canceled religious holidays to manipulate the population.

5. Harris vs. Trump: A debate between the two candidates will take place this coming Tuesday on the 10th of September. Because of murky outlooks among many financial institutions, this televised ‘exchange of views’ will not only get the attention of U.S voters and an interested worldwide populace, but global investors as well. The last Presidential debate effectively ended Joe Biden’s hopes of being re-elected. Will this event proceed without biased moderators?

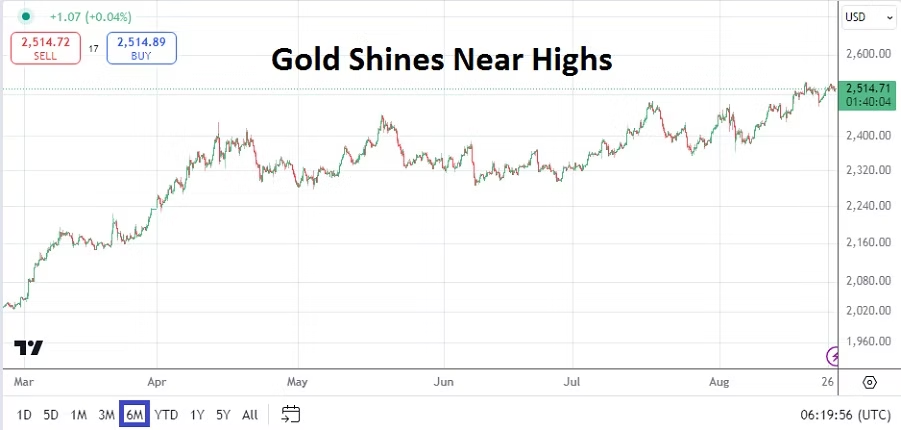

4. Wobbly High-Wire: WTI Crude Oil finished the week around 68.52 per barrel as traders appear to be worried about a U.S economic slowdown. Gold closed Friday near the 2,497.00 realm per ounce, as investors fret over the USD and Federal Reserve. BTC/USD is trading around 54,230 at the time of this writing, Bitcoin was valued around 65,000 early on the 26th of August. Cocoa closed near 8,300.00 USD per ton yesterday after flirting with lows touching 7,900.00 on Wednesday. Day traders trying to wager this past week within commodities likely found they were not immune to nervous sentiment.

3. Negative: U.S jobs data was bad. While some say the numbers were mixed the Non-Farm Employment Change came in significantly lower than its estimate, and the previous month’s statistics were revised downwards. The higher Average Hourly Earnings report provided no favors via its outcome of 0.4% compared to the expected result of 0.3%, it wasn’t too far from the estimate and should not change inflation perspectives. Simply put, the jobs numbers are causing concerns in many financial institutions who believe the Federal Reserve is being too cautious.

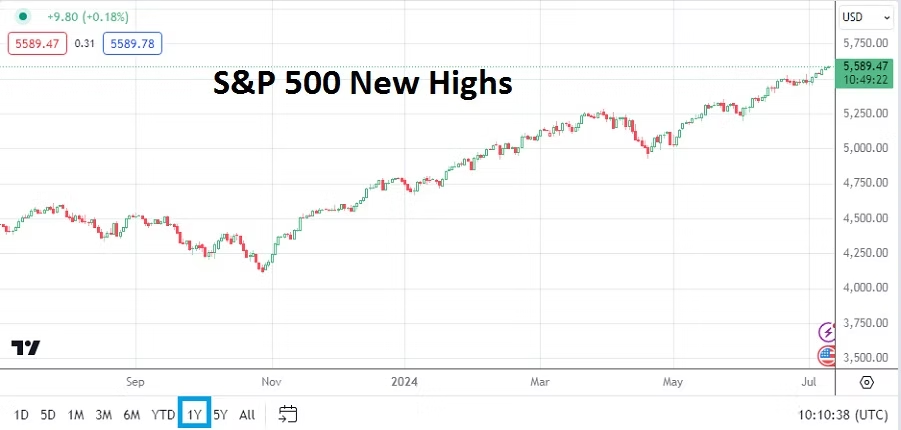

2. Nervous Investors: U.S equity indices finished yesterday’s trading at their lows for the week. In fact the Nasdaq 100, Dow 30 and S&P 500 are all traversing values they last saw on the 13th of August. The major indices are fragile. Equities on the 13th of August were still recovering from losses seen the week before when previous Fed and BoJ policy chaos triggered overreactive selling on the 5th of August. On Friday the 2nd of August negative Non-Farm Employment Change data was published. What will happen to indices, Forex and Treasury yields on Monday the 9th of September?

1. Fed Fail: John Williams the New York Federal Reserve President said after the jobs numbers were reported, that the Federal Funds Rate is in a position to be cut. However, Williams continued to lean into the widespread notion the Fed will only impose a 0.25% decrease. He did say he would look at the jobs numbers closely, but he believed the Fed is well positioned. Behavioral sentiment among financial institutions appeared to react poorly to Williams remarks, producing a strong selloff as Friday progressed. The dream of orchestrating a soft economic landing in the U.S by the Federal Reserve allowing inflation to erode, the jobs market to soften, and GDP to remain above recessionary pressure remains the lofty goal. However financial institutions do not like the convoluted mid-term economic outlook, they now want to hear a dovish sounding Federal Reserve and appear ready to cause more short-term chaos in the markets this coming week.