While Forex traders around the world look for clues as to why their local currencies are suffering and are likely blaming domestic policy from their own governments and central banks, they should remember the larger global financial markets tend to move in a unified sphere. Domestic concerns are a real cause for market action often, but when global sentiment becomes nervous the larger force of institutional financial houses shake the ground.

Correlations exists worldwide because of behavioral sentiment ruling outlooks over the near, mid and long-term in the marketplace. While we like to put our faith in the financial markets as an all knowing entity, this is far from the truth. Humans who react to nervous conditions and also have bias are the ones still making decisions in financial houses, they are the ones giving orders to their programmers via their trading software which is largely geared to follow perceived trends these institutions deem important.

Most financial institutions are not speculative in nature, day and even longer term retail traders should remember this point. Most institutions are trying very hard not to ‘speculate’, they are simply positioning per their outlooks based on their understanding of the trading landscape. Whispers of potential downgrades from U.S rating agencies on larger corporate banks yesterday sent a shudder through the broad markets, economic data and rumors swirling about China are not helping either. The current volatility in the broad markets is not welcomed warmly by financial institutions.

When price velocity accelerates and volatility flourishes in highly charged trading situations, this suggests financial institutions are nervous and not able to find comfortable positions. Conflicting ‘opposite’ positions from other larger players are causing market chaos in Forex, equities and other financial assets. There is a herd mentality in trading and when the herd doesn’t march in an unified direction chaos happens.

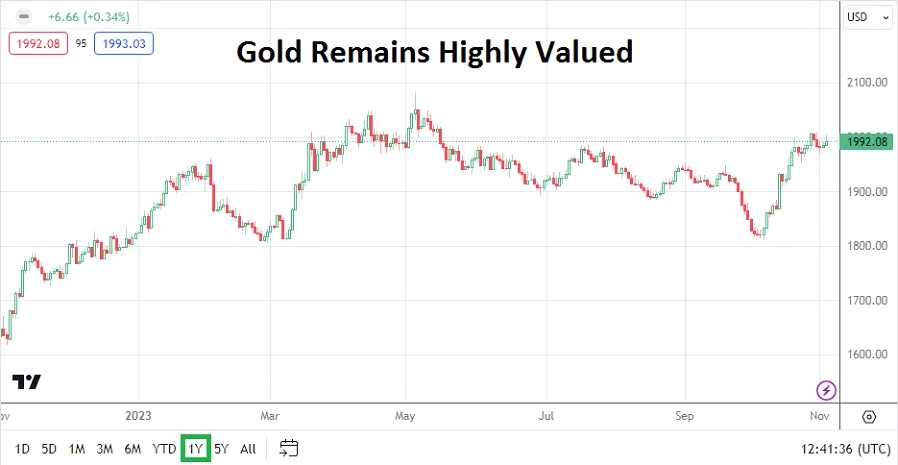

Most institutional players want calm, they want tranquil trading conditions so they can manage their clients’ money quietly. Bonds, equities and indices, real estate holdings via REITs, and gold make up a large part of their holdings.

Most U.S pension funds for instance have mandates to be positioned into a large amount of quiet investment vehicles which do not trade with wild price ranges. They seek steady returns from their institutional investors that can be counted on in a quantitative manner to demonstrate to their clients.

Large financial institutions are allowed sometimes to trade 2 to 4% of their holdings in different categories of speculative investments – such as start-ups, allocate cash to hedge funds they trust, small cap stocks they might know about, etc., depending on the exact mandates agreed upon.

Yes, hedge fund managers like Bill Ackman and investor Michael Burry get a lot of attention when they bet against the markets, but believe it or not they are small fish in a large ocean a lot of the time. They are good at what they do, but their speculative positions cannot be mirrored by most financial institutions or small day traders.

Ackman and Burry may be trading billions, but remember institutional financial companies including pension funds when combined total approximately 80% of market cap. Institutional trading decisions can cause massive waves in the financial world, but they actually seek calm seas.

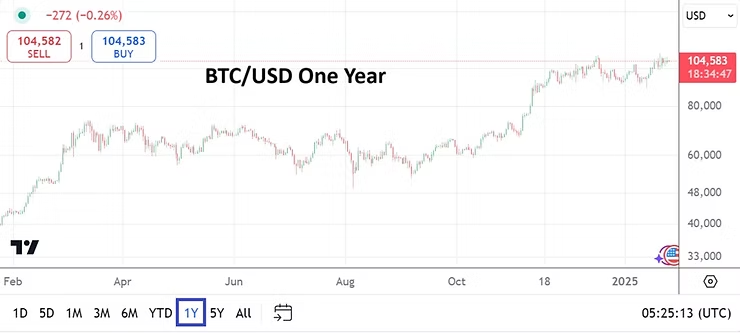

When markets become volatile this often means institutional traders are not comfortable and their behavioral sentiment is fragile. Forex for example is often affected by financial institutions moving money as they handle export and import transactions for companies, but transactions are often done to buy and sell equities too. The Bank of International Settlements estimated an average around 7.5 trillion USD in value was traded in Forex everyday in 2022.

Day traders should not take it personally when the markets move against them, instead they should look to try and mirror the sentiment of larger financial movers. However, knowing and timing financial institution decisions is elusive because short term compared to long term considerations are often different.

Most traders are merely betting on the price action the large institutional funds are undertaking via the direction of the marketplace. Day trading for most retail speculators remains dangerous. A solid fundamental understanding of market ‘forces’ can allow smaller traders to feel more comfortable.