Forex: Behind the Curtain as Speculative Deja Vu Strikes

Friday jobs reports came in stronger than anticipated on the surface, and this led to a roller coaster like ride for Forex traders as results were acted upon by financial institutions. However, a look behind the data shows ‘positive’ results were spurred on by part-time hiring and government influences leading to a notion that jobs numbers were not exactly a ray of sunshine regarding U.S economic health. The suspicious results cause a desire to look for ulterior motives, and to wonder if election year politics are playing a role in the U.S employment picture.

GBP/USD Six Month Chart as of 9th April 2024

The GBP/USD and EUR/USD are rather insightful for technical and fundamental traders. The currency pairs are languishing as of today’s values near pricing that was seen in the second week of December. Since the ‘announcement’ from the U.S Federal Reserve on the 13th of December that a change in monetary policy would begin to occur in 2024, in actuality nothing has really happened, except government ‘speak’ trying to sound as if everything is understood and in control, while it is clearly not.

Economic data from the U.S and Europe has continued to be soiled by mixed results, and retail speculators looking for a trend to emerge have had to deal with choppy conditions. Financial institutions remain unclear about interest rate outlooks. The Fed while trying to ‘sound’ dovish rhetoric remains locked within a Google engine keyword mantra as they mutter the phrase ‘over time’ when trying to convince people that interest rates will ‘eventually’ be cut.

Last week leading up to the Non-Farm Employment Change numbers, many FOMC members were offering cautious tones about the Federal Funds Rate and warning it should not be changed yet. The implication of the Fed’s verbiage could lead some to suspect they have all practiced statements handed to them by their overlords who are concerned this is an election year and jobs are in jeopardy.

EUR/USD Six Month Chart as of 9th April 2024

Which leads us back to Forex and all financial assets, as investors try to swim waters which have left fundamental perspectives grasping at data which is not easy to decipher. U.S government policy is practicing fiscal spending that is causing massive debts, and perhaps influencing hiring data which may be more akin to putting lipstick on a pig. Many U.S voters seemingly lean towards electing officials who promise to hand out the biggest ‘social rewards’, while ignoring there will be a price to be paid down the road.

The Federal Reserve in the meantime tries to sound optimistic about inflation eroding, but concerns due to U.S government debt being accrued, and global geopolitical affairs combined with energy policy which is making it more expensive to maintain cheap transportation, efficient agriculture and manufacturing, shadow the Fed’s hopes. WTI Crude Oil remains over 86.00 USD per barrel. Gold is trading at record high values and above 2300.00 USD. Does anyone see the dangerous connections? Equity indices should be watched as a barometer this week.

USD/JPY Six Month Chart as of 9th April 2024

Monday, 8th of April, Japan Average Cash Earnings and Economic Watchers Sentiment – yesterday’s reports matched expectations regarding wages, but workers surveyed noted their concerns about incremental inflation which is being seen in Japan. The USD/JPY is challenging November higher values and the Bank of Japan has been widely criticized for not raising interest rates more aggressively. However, it is possible the BoJ wants the Japanese Yen to remain within its weaker price range to spark a stronger Japanese economy via exports.

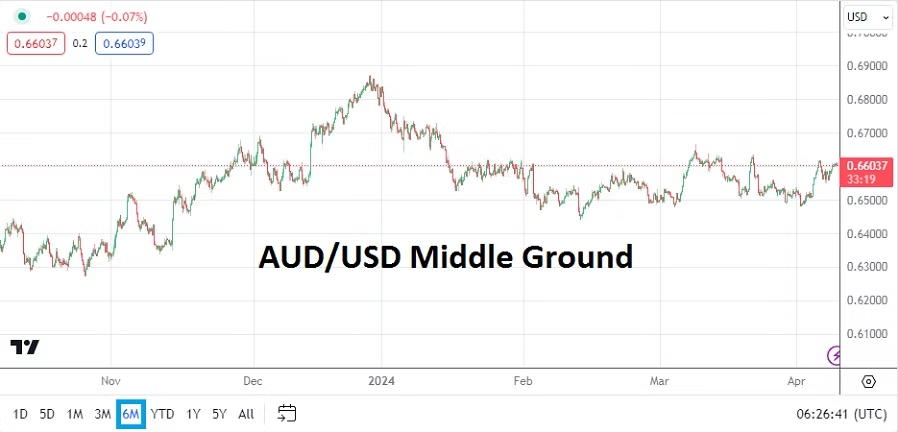

AUD/USD Six Month Chart as of 9th April 2024

Tuesday, 9th of April, Australia Westpac Consumer Sentiment – the results via the consumer reading came in negative. The AUD/USD like the GBP/USD and EUR/USD is traversing values tested in the second week of December 2023, leading to the feeling of deja vu.

Wednesday, 10th of April, U.S Consumer Price Index – you have heard this before, the inflation reports from the States are going to rattle the financial markets including Forex. The USD is certain to react. Data from the U.S has produced surprises aplenty in the past few months. The Consumer Price Index is important and day traders certainly need to pay attention.

Thursday, 11th of April, European Central Bank – the ECB is not expected to change its Main Refinancing Rate, but many analysts believe they should cut borrowing costs. However, the ECB will likely remain within the camp of choosing to ‘wait and see’. The ECB Press Conference with Christine Legarde has widely become regarded as an opportunity for political speech as much as an economic dialogue. Recent data from the European Union suggests the worst of the recessionary cycle is gone, but German Trade Balance numbers released on Monday were negative, highlighting hurdles remain. Inflation is a worry, and a cut to the interest rate might be able to help spur on economic activity while counting on lagging data to prove proactive policy should be implemented. But this likely is not going to happen and the EUR/USD will remain problematic.

Thursday, 11th of April, U.S Producer Price Index – these slew of reports should be watched carefully. If the data is stronger than expected it is likely a part of the residue caused by higher energy costs that have affected logistics and created more expensive raw materials which are needed to produce goods. It was the higher PPI reports last month that caused dramatic tidal shifts in Forex, speculators should brace for the potential of additional mayhem.

Friday, 12th of April, U.K Gross Domestic Product – last month’s GDP numbers from Great Britain came in slightly higher than expected with a 0.2% gain, this report is anticipating growth of only 0.1%. Traders should take a deeper look at the statistics upon publication and check for revisions to past months. The U.K economy has been struggling, the ‘growth’ results will affect the GBP/USD before going into the weekend.

Trading Optimism for 2024 and Pursuit of Castles in the Air

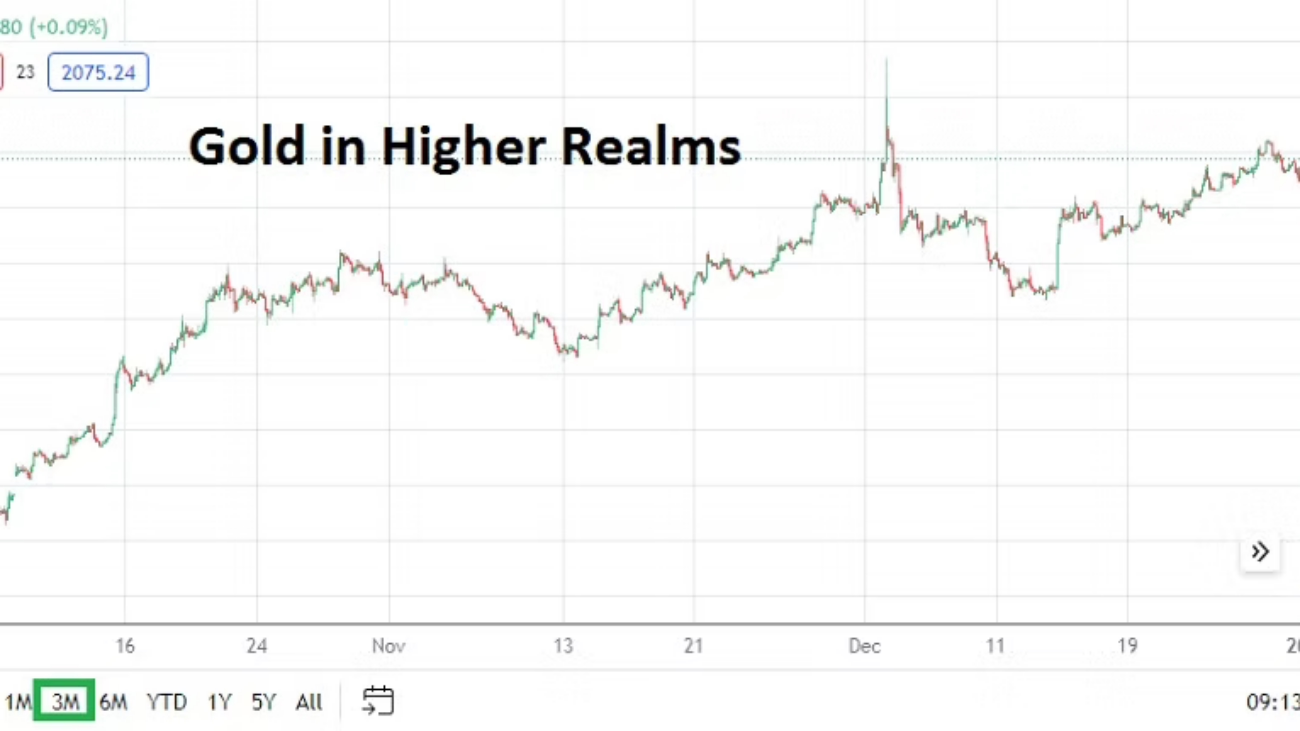

Traders may feel like horses being kept in their stables right now. The desire to run freely in Forex and other markets is certainly being felt, this as many analysts have jumped onto optimistic bandwagons and are pointing to the U.S Federal Reserve and its rather dovish outlook for 2024. Gold in early trading this morning is lingering near highs and the USD remains within weaker territory when technical charts are inspected via one month results.

Gold Three Month Chart as of 2nd January 2024

Yet, thin holiday trading is full in effect. Light volumes will continue to be seen early this week after the New Year’s celebrations. Financial institutions will open their doors today, but their corporate clients around the world will have plenty of employees who will remain on vacation until the 8th of January. Thus, while day traders may feel enticed to wager in the markets with various CFDs, they should be careful and understand unbalanced positions may cause temporary chaos. Risk taking tactics should be carefully considered.

The desire to dream about castles in the air is a source of comfort for many new day traders. But remaining realistic about potential results, while not getting overly ambitious about targets is an important aspect for all speculators. While trends may look attractive in Forex, commodities and equities a well planned approach regarding risk taking is a practical road. Castles in the air tend to vanish.

Optimism will be a word frequently heard in the coming days and weeks, and here’s to wishing everyone a prosperous and peaceful 2024. The potential of a more dovish U.S Federal Reserve regarding monetary policy and declining Treasury yields sparking more risk appetite in equities as investors seek solid returns is alluring, however risks remain on the table. The economy of China continues to worry analysts and tensions in the Middle East are still a long way from being solved.

However, the biggest cause for speculative concerns during 2024 may come from elections in Taiwan, India, South Africa and the United States. Taiwan’s presidential vote is on the 13th of January. China will certainly be watching the results, and traders should expect to hear swords rattling afterwards and then hope the noise calms down.

USD/ZAR One Year Chart as of 2nd January 2024

Tranquil voting results in India will be welcomed by investors. India is becoming a noteworthy economic giant, its rapid growth and ascension as an important investment vehicle needs to remain stable. South Africa remains troubled domestically by concerns regarding corruption and inefficiency, its upcoming spring election results may not solve the problems it faces. There will be many elections in Africa this year, which could spur on considerations regarding geopolitical alliances and the price of commodities.

The U.S election late in 2024 will start to grow in noise as the months progress and by early this summer behavioral sentiment will begin to become nervous regarding the outcomes for the White House and Congress. The U.S appears to be braced for an election between Joe Biden and Donald Trump and this will certainly cause skittish storms.

Traders should feel confident about risk appetite in the global markets improving, but they should keep in mind that impetus coming from many different spheres can affect the financial world.

Tuesday, 2nd of January, U.S Final Manufacturing PMI – today’s Purchasing Managers Index is expected to show a slight improvement, but the results may fall on deaf ears because many market participants will not be around to react due to the fact they are still on vacation.

Wednesday, 3rd of January, U.S ISM Manufacturing Prices – this inflation survey from purchasing managers may be given a bit of attention, but its effect may be limited because of light trading volumes still being exhibited.

Thursday, 4th of January, Germany Preliminary CPI – the inflation data from Germany will get some consideration, and the result is expected to show a slight increase. Services PMI data will also come from European Union nations, the U.K and U.S.

Friday, 5th of January, U.S Non-Farm Employment Change and Average Hourly Earnings – the jobs reports will get the notice of financial institutions. The results for employment and wages are expected to be slightly weaker than the previous month’s outcomes. Typically these numbers would cause a stir, but unless there are surprises, most financial institutions may not react massively to the reports because it remains a ‘holiday’ week. If the numbers come in weaker than expected this could cause interesting reactions on the 8th of January and weaker USD sentiment.

AMT Top Ten Miscellaneous Feast for the 24th of November

10. Book: A Thanksgiving Diet – Life as a Glutton by T.M.F Resuscitate.

9. Music: Frank Sinatra singing Somethin’ Stupid.

8. Global Commerce: London Metal Exchange and Baltic Exchange Dry Index prices are higher since September lows.

7. Post Holiday Warning: Trading volumes will be light today, day traders should expect quiet markets and sudden bursts of volatility. Early reactions next week may result in reversals due to perceived lack of price equilibriums having occured via today’s results, this as U.S financial institutions return in full to their offices Monday and Tuesday.

6. Election Surprises: Argentina and the Netherlands point to seismic changes in voting sentiment. India, South Africa and the U.S have major elections coming in 2024.

5. Crytocurrencies: Binance legal problems in the U.S casting shadows of doubt, but BNB/USD has been somewhat stable. Bitcoin – yes, a digital asset – is above 37,000.00 USD as of this writing.

4. Gold: Price of the precious metal remains slightly below 2000.00 USD level.

3. Energy Prices: WTI Crude Oil, Brent, Natural Gas and Gasoline remain within sight of one year lows, but intriguing support levels for speculators with long-term outlooks.

2. U.S Equity Indices: Stocks will trade in shortened sessions today. The major indices are within sight of one year highs. Next week could see positive momentum sustained.

1. Forex: USD within an intriguing near-term price range. GBP, JPY and NZD are some of the major currencies showing signs of potential strength versus the ‘greenback’ as outlooks seemingly shift.