Fed Rhetoric, U.S Consumers, and Fresh Concerns about China

U.S inflation data via the Consumer Price Index last Thursday met the anticipated result regarding the core number, and the broad statistics were only fractionally larger than expected. U.S Treasuries yields however jumped via quick reactions about stubborn inflation, then settled down. Equities via the major indices continue to show nervousness.

Day traders continue to get hit by choppiness, which means if they are not on the correct side of a trade initially, they can get knocked out of their positions quickly due to the use of too much leverage.

China produced another round of troublesome Consumer Price Index Producer Price Index reports last Friday, once again highlighting deflation is a legitimate concern for the nation.

The USD began to weaken within many major currency pairs on late Tuesday and early Wednesday, and then began to prove difficult with sideways price action. However, many currencies held onto their slight gains against the USD going into the weekend. But before a massive bearish trend against the USD actually can be sustained, perceptions about the U.S Federal Reserve stands clearly in the way regarding behavioral sentiment.

Inflation numbers last week remained strong enough to suspect the Fed will raise interest rates again on the 1st of November. As a way to keep traders on their toes, U.S Federal Reserve officials will be speaking at many functions over the entirety of this week, offering crumbles of evidence for their less than spectacular rhetoric on the global economy no doubt.

Gold has produced a rather startling climb in the past ten days and its one month charts resemble a rather turbulent roller coaster. Traders who have been pursuing the precious metal during its strong reversals the past handful of weeks have hopefully been using solid risk management while taking a speculative ride.

Monday, the 16th of October, U.S Empire State Manufacturing Index – the number has come in slightly better than expected, but has still produced a negative reading of minus -4.6. While many U.S officials will not state it publicly, a decline in the manufacturing index may pave the way towards a more tranquil Federal Reserve. But this may be wishful thinking too, particularly if inflation remains elevated.

Tuesday, the 17th of October, U.S Retail Sales – the data about consumer spending will affect Forex if there are surprises. Both the core and broad reports are anticipated to be weaker than last month’s numbers. Weaker results could create some USD weakness.

Wednesday, the 18th of October, China Industrial Production, Gross Domestic Product and Retail Sales – the Industrial Production results are expected to be slightly weaker than last months, while the GDP outcome is being estimated to show a significant drop. If the growth number comes in at the anticipated 4.5% mark it would be another signal that China is struggling while trying to jump start the economy. USD/CNY traders should be careful around these reports.

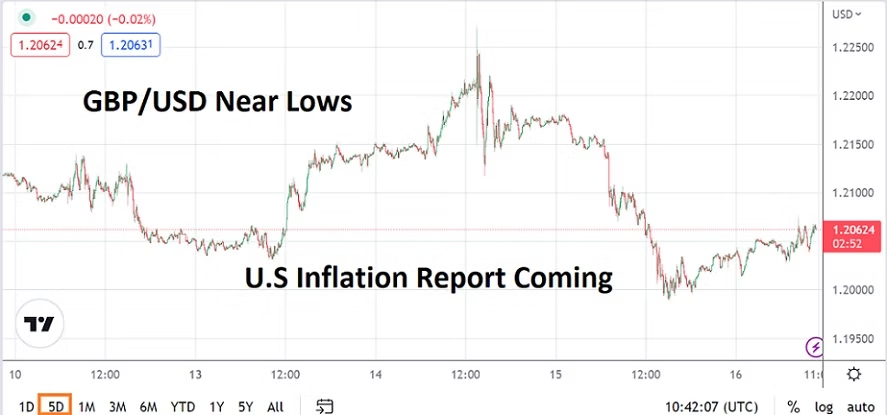

Wednesday, the 18th of October, U.K Consumer Price Index – the CPI data from Great Britain is expected to show a slight decline from the previous month. While last week’s GDP numbers met their rather lackluster expectations; Construction, Manufacturing, Trade Balance data came in much worse than anticipated. While no one from the U.K government is going to cheer on the bad economic numbers from last week, these figures will make these CPI inflation results important to monitor. Will the U.K inflation numbers remain stubborn like the U.S? The GBP/USD certainly needs to be watched in the aftermath of this CPI report.

Thursday, the 19th of October, China New Home Prices – the housing bubble within China is a thing of the past. Last month’s outcome produced another negative number and a poor report would not be a surprise this week. Negative housing values hurt the Chinese public which have largely quantified their personal savings via their real estate holdings.

Thursday, the 19th of October, U.S Unemployment Claims – the weekly report will give another small dose of evidence regarding the strength of the U.S economy for financial institutions to consider.

Friday, the 20th of October, U.K Retail Sales – the consumer spending report is expected to produce a decline of minus -0.3%. GBP/USD traders may use this report as another sphere of influence.