Trading Optimism for 2024 and Pursuit of Castles in the Air

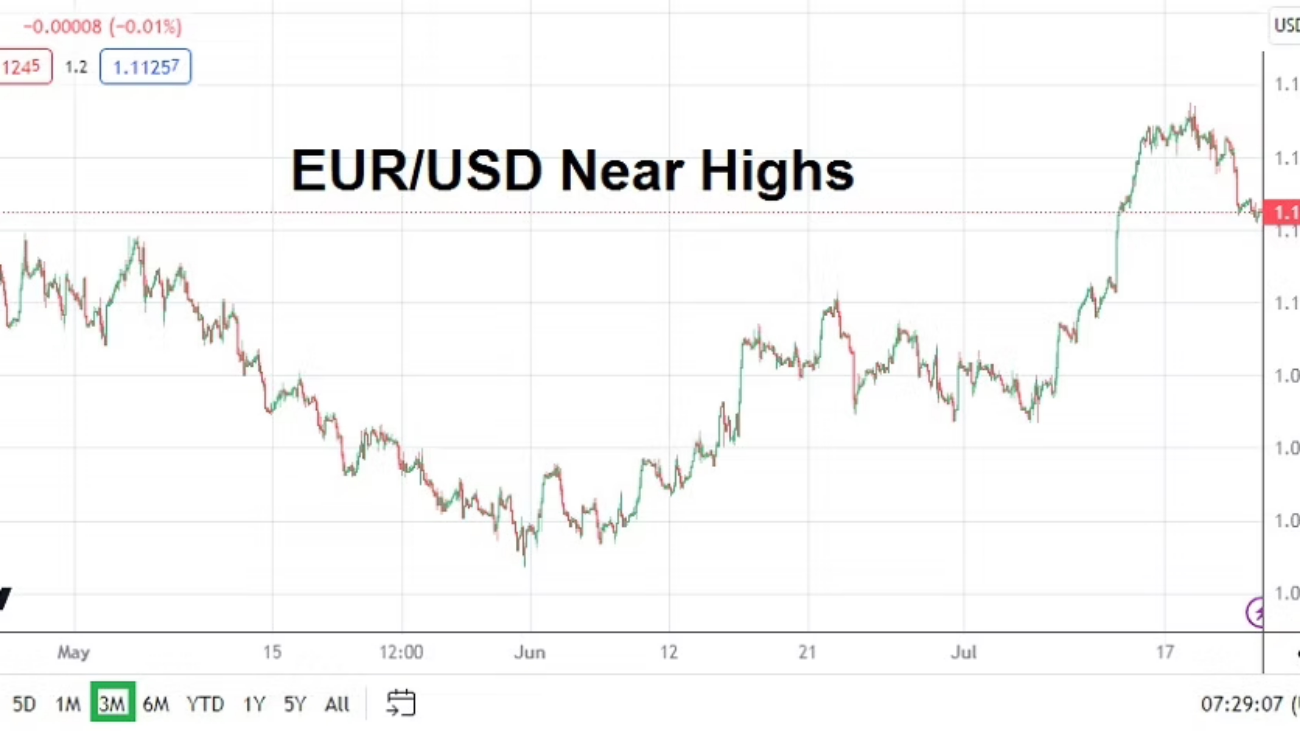

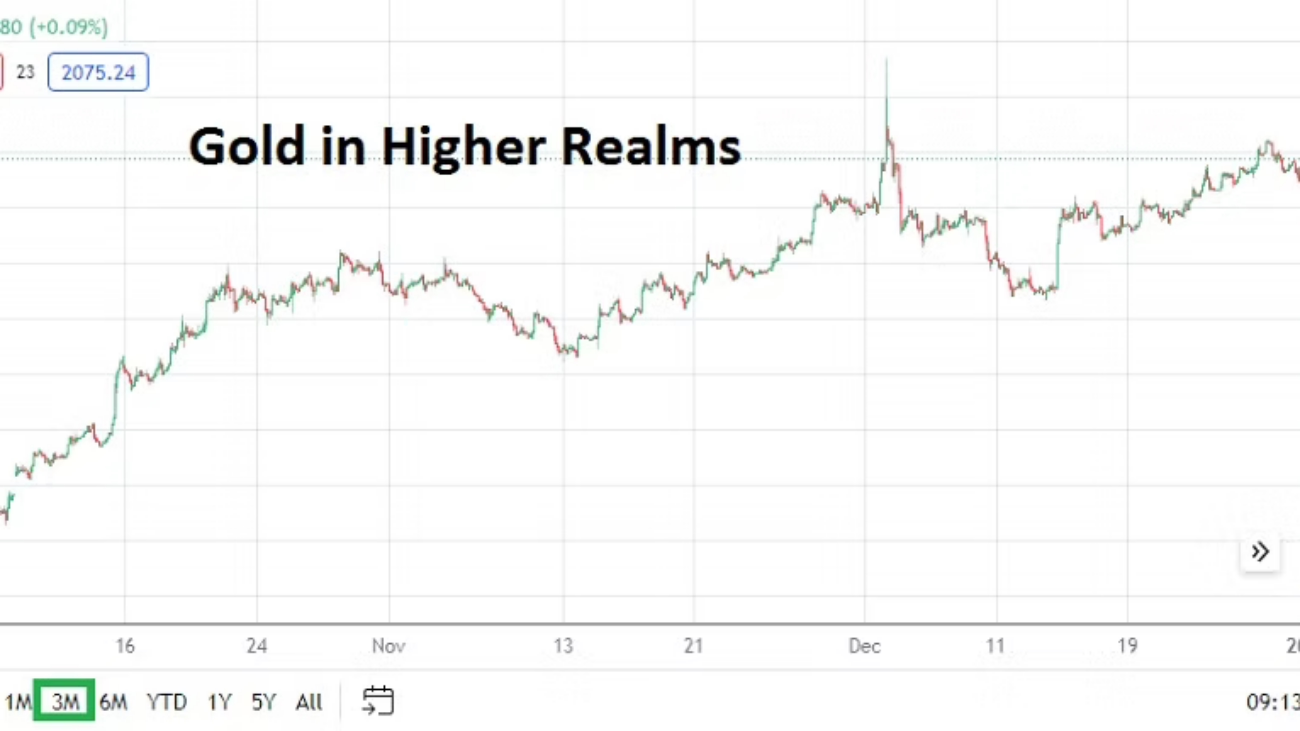

Traders may feel like horses being kept in their stables right now. The desire to run freely in Forex and other markets is certainly being felt, this as many analysts have jumped onto optimistic bandwagons and are pointing to the U.S Federal Reserve and its rather dovish outlook for 2024. Gold in early trading this morning is lingering near highs and the USD remains within weaker territory when technical charts are inspected via one month results.

Yet, thin holiday trading is full in effect. Light volumes will continue to be seen early this week after the New Year’s celebrations. Financial institutions will open their doors today, but their corporate clients around the world will have plenty of employees who will remain on vacation until the 8th of January. Thus, while day traders may feel enticed to wager in the markets with various CFDs, they should be careful and understand unbalanced positions may cause temporary chaos. Risk taking tactics should be carefully considered.

The desire to dream about castles in the air is a source of comfort for many new day traders. But remaining realistic about potential results, while not getting overly ambitious about targets is an important aspect for all speculators. While trends may look attractive in Forex, commodities and equities a well planned approach regarding risk taking is a practical road. Castles in the air tend to vanish.

Optimism will be a word frequently heard in the coming days and weeks, and here’s to wishing everyone a prosperous and peaceful 2024. The potential of a more dovish U.S Federal Reserve regarding monetary policy and declining Treasury yields sparking more risk appetite in equities as investors seek solid returns is alluring, however risks remain on the table. The economy of China continues to worry analysts and tensions in the Middle East are still a long way from being solved.

However, the biggest cause for speculative concerns during 2024 may come from elections in Taiwan, India, South Africa and the United States. Taiwan’s presidential vote is on the 13th of January. China will certainly be watching the results, and traders should expect to hear swords rattling afterwards and then hope the noise calms down.

Tranquil voting results in India will be welcomed by investors. India is becoming a noteworthy economic giant, its rapid growth and ascension as an important investment vehicle needs to remain stable. South Africa remains troubled domestically by concerns regarding corruption and inefficiency, its upcoming spring election results may not solve the problems it faces. There will be many elections in Africa this year, which could spur on considerations regarding geopolitical alliances and the price of commodities.

The U.S election late in 2024 will start to grow in noise as the months progress and by early this summer behavioral sentiment will begin to become nervous regarding the outcomes for the White House and Congress. The U.S appears to be braced for an election between Joe Biden and Donald Trump and this will certainly cause skittish storms.

Traders should feel confident about risk appetite in the global markets improving, but they should keep in mind that impetus coming from many different spheres can affect the financial world.

Tuesday, 2nd of January, U.S Final Manufacturing PMI – today’s Purchasing Managers Index is expected to show a slight improvement, but the results may fall on deaf ears because many market participants will not be around to react due to the fact they are still on vacation.

Wednesday, 3rd of January, U.S ISM Manufacturing Prices – this inflation survey from purchasing managers may be given a bit of attention, but its effect may be limited because of light trading volumes still being exhibited.

Thursday, 4th of January, Germany Preliminary CPI – the inflation data from Germany will get some consideration, and the result is expected to show a slight increase. Services PMI data will also come from European Union nations, the U.K and U.S.

Friday, 5th of January, U.S Non-Farm Employment Change and Average Hourly Earnings – the jobs reports will get the notice of financial institutions. The results for employment and wages are expected to be slightly weaker than the previous month’s outcomes. Typically these numbers would cause a stir, but unless there are surprises, most financial institutions may not react massively to the reports because it remains a ‘holiday’ week. If the numbers come in weaker than expected this could cause interesting reactions on the 8th of January and weaker USD sentiment.