10. Word of the Day: Quaestuary, the usage of the word comes from William Manchester’s book A World lit only by Fire. The word is now considered obsolete. Manchester used the Latin word, quaestiarii, to describe profit making by the Roman Catholic Church during the Middle Ages and into the Renaissance. Church ‘officials’ would use their positions of power to raise money dubiously. Promising absolution to the naive via treacherous claims which included the charging of payments for potential sins committed in the future, and a more lenient purgatory for already deceased members of a family who were waiting to be allowed into heaven because of past transgressions.

9. Undecided: With less than two months before the U.S election for President, swing States are crucial battlegrounds for candidates Trump and Harris. Turning purple into red or blue is the prime task for the Republicans and Democrats. Economy, immigration, foreign policy, reproductive rights are among the talking points. Which side can receive the most votes via promises that will be hard to accomplish?

8. Artificial Intelligence: Early this week Oracle Corporation released revenue results and projections showing that profits are increasing due to demand for data centers as the use of AI expands. Cloud services provided by Oracle has become the corporation’s largest source of growth. Investments in big data centers are getting competitive. Data4 has recently announced they are going to invest approximately 300 million EUR into a data center facility in Paiana, Greece. Data4 led by Olivier Micheli, CEO, has announced that it plans on investing around 7 billion EUR into 2030 for expansion.

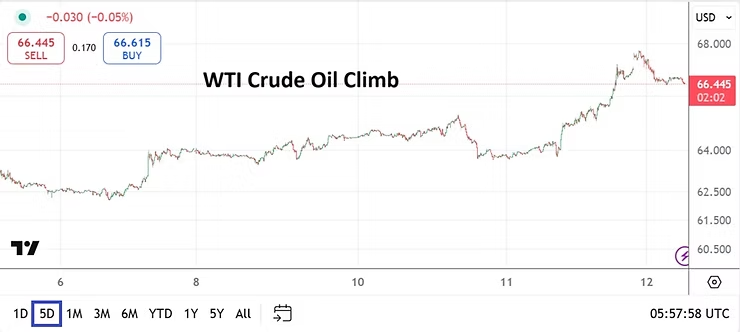

7. Crude Oil: WTI Crude Oil briefly went above the 70.00 USD mark on Friday, but went into the weekend near 69.33. U.S economic data this coming week (besides the U.S Fed on the 18th) will be limited to manufacturing readings and retail sales data. The notions that the U.S economy is struggling via weaker employment numbers and lackluster GDP, European data remaining murky, while China is not exactly robust is likely causing speculative demand in Crude Oil to remain low. Global energy supply is solid and the Middle East conflict remains somewhat muted.

6. Whipsaw Gains: Major U.S equity indices moved upwards as the Dow 30, S&P 500 and Nasdaq 100 all produced better weekly results. However, improved momentum mostly occurred as equities reversed from nervous lows on Wednesday. The Dow 30 and S&P 500 are within sight of apex values, while the Nasdaq isn’t far behind. U.S Treasury yields also dropped lower via their totals for the week with the 5, 7, and 10 Year Notes approaching yields last seen in the spring of 2023. The 30 Year Bonds are traversing lower too, but will have to penetrate early 2024 levels to then challenge depths from early 2023.

5. Inflation: Global central banks are having a large internal debate about their target inflation numbers. Trying to agree on what the neutral rate – mean average – over the next year should be is causing central banks to remain cautious about inflation projections. While it is clearly evident that Europe and the U.S are facing economic headwinds the ECB, Fed and BoE seemingly refuse to step on the gas pedal and become aggressively dovish. However, financial institutions who frequently use their mid-term outlooks as guidance continue to lean into their trading positions and seemingly wager on the central banks having to become more dovish. How much can each central bank cut by over the next 6 months? Why not cut by 0.50% to inject easier borrowing rates now? Because apparently it seems all the central banks remain nervous about inflation remaining stubborn. The word stagflation still comes to mind. The decline in Crude Oil prices seen the past few weeks may be a hopeful sign for lower costs.

4. USD/JPY: The currency pair finished trading near the 140.775 ratio on Friday. Trading in the USD/JPY appears to be driven by the notion that financial institutions believe the U.S Federal Reserve is going to have to cut the Federal Funds Rate by 0.75% over the next six months. Behavioral sentiment has a breathtaking history of producing strong trends in the USD/JPY. The Bank of Japan will announce their Monetary Policy Statement on the 20th of September. The USD/JPY was trading near 162.000 in July and its decline lower seems to have surprised some, but why? The BoJ is likely going to sound cautious this coming week, but sitting on their hands and allowing their global counterparts to become more dovish may be enough to keep the USD/JPY within its lower price realm.

3. China Data: Numbers published early this morning showed that New Home Prices continue to fall, Industrial Production has decreased, Retail Sales have dropped, and the Unemployment Rate has risen. China’s economy is suffering. The USD/CYN looks too low at the current rate of 7.0925. The Shanghai Composite (SSE) has fallen to nearly 2,704 and touching lows from early February of 2024. The SSE is down roughly -13.46% over the last year. The Chinese government’s desire to manage the economy with a tight grip continues to produce fractures and should be reconsidered.

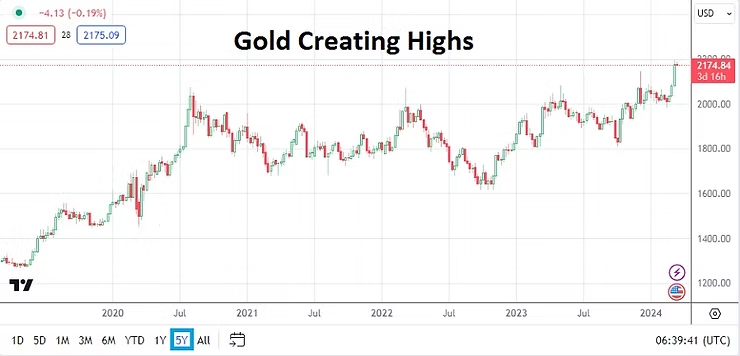

2. Gold: The precious metal finished Friday’s trading near 2,577.00. Yesterday’s values hit all-time record prices for Gold versus the USD. The 2,586.00 vicinity was touched before reversing slightly lower. The ability to remain near apex highs going into the weekend highlights large traders likely still have a taste for gold and that long-term investors remain bullish. Is nervousness due to perceived global central bank ineptitude helping to create more gold buying? Short-term speculators need to remain careful within these heights.

1. FOMC Prediction: The European Central Bank’s decision to cut by only 0.25% this past Thursday is almost a sure sign the Federal Reserve will mirror the ECB on the 18th of September. Last week’s prediction by AMT that the ECB would only cut by 0.25% proved to be true, and our outlook for the FOMC’s Federal Fund Rate decision is also a cautious 0.25% cut. While the U.S Consumer Price Index and PPI info published this past Wednesday and Thursday showed inflation is under control, the data also shows a stubborn streak. However, an erosion of inflation is taking place and while the target ‘neutral’ rate is likely being debated behind closed doors, it is also apparent to most outside observers that the Fed is being too cautious and will be ‘forced’ to cut this coming week, November 2024, and early in 2025.