Retail Traders Caught Out by Shifting Sentiment as Data Hits

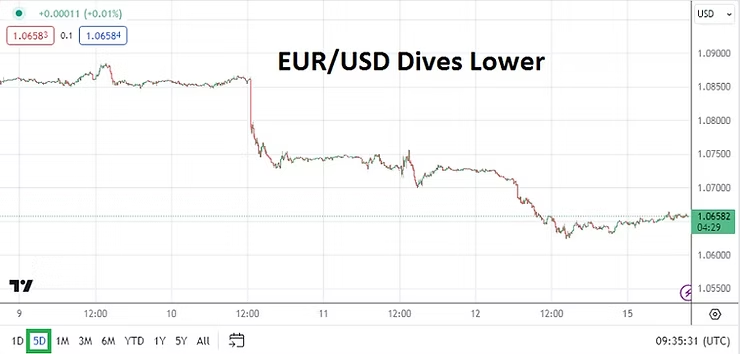

Forex speculators who relied heavily on technical data solely last week were likely punched in the gut by the rather surprising numbers from the Consumer Price Index results in the U.S last Wednesday, particularly if they were on the wrong side of trading trajectories. U.S inflation has shifted sentiment within many large investors with a rather seismic move regarding mid-term outlooks. Financial institutions which have been counting on cuts to the Federal Funds Rate have had to take a step backwards.

EUR/USD Five Day Chart as of 15th April 2024

The dynamic momentum in Forex hit major currency pairs in the middle of last week and washed away support and resistance levels within a blink of the eye. Behavioral sentiment turned U.S Treasuries yields upwards and the major equity indices also experienced nervousness. Volatility also continued in Gold as new record values were produced, and then were followed by a rather strong reversal lower which likely hurt over-leveraged day traders.

Gold Five Day Chart as of 15th April 2024

Not only were U.S inflation numbers important last week, but geopolitical noise became heightened. Perhaps the climb in Gold before the weekend was helped by the anticipated conflict between Iran and Israel which did play out. The price of the precious metal and WTI Crude Oil have been more tranquil early today, which may be a signal for the moment that large market players are calm.

Monday, 15th of April, U.S Core Retail Sales – after last week’s larger than expected increase in the CPI results, the spending report today will get attention from financial institutions. Last Friday’s Preliminary Price Expectations reading from the University of Michigan did not allow investors to rest when it came in with a 3.1% elevated mark. If today’s Retail statistics are above expectations, this could make Forex roil again.

Tuesday, 16th of April, China Industrial Production and Gross Domestic Product – these economic reports will be watched closely by international investors. While there have been murmurs that China’s economy is improving, and media reports that the Biden administration is trying to engage diplomatically, the industrial and GDP results are expected to be weaker than the previous month’s outcomes. China will also release Retail Sales figures.

GBP/USD Five Day Chart as of 15th April 2024

Tuesday, 16th of April, U.K Claimant Count Change – last Friday’s GDP report from Britain did not produce any significant surprises. The U.K economy continues to struggle, but like most spheres inflation remains a problem. The GBP/USD sunk violently last week, while many speculators may believe it is currently oversold they may want to remain cautious.

Because of the U.S Federal Reserve’s own perilous fight against inflation, there are some who believe the Bank of England may need to cut interest rates before the U.S central bank. However, given the lack of proactive characteristics from the BoE and ECB which have been on full display as they dance in step with the Federal Reserve, this makes a BoE cut before the Fed a skeptical notion for the time being. The GBP/USD will stay largely USD centric even in the wake of this U.K employment report.

Tuesday, 16th of April, U.S FOMC Members – a parade of Federal Reserve voting policymakers will speak at various events, this includes Fed Chairman Jerome Powell. There will likely be little in the way of surprises from the Fed members as they likely all stick to ‘party’ lines and emphasize a cautious outlook.

Wednesday, 17th of April, U.K Consumer Price Index – the inflation report could prove to be catalyst for the GBP/USD. If the CPI number does come in weaker than expected it could spur on behavioral sentiment shifts regarding the potential for changes to BoE policy. Because the GBP/USD was so volatile the past week, day traders should be prepared for rather combustible price action from the currency pair which may look counter-intuitive. Smaller speculators should remember that ‘smart money’ from larger players may be positioned for the results of the U.K CPI data already.

Thursday, 18th of April, U.S Weekly Unemployment Claims – although not the most significant of reports usually, financial institutions are ‘waiting’ on a change of statistical direction via labor market evidence. If jobs numbers start to come in weaker than anticipated – meaning there are higher jobless claims – then the USD could react with some selling.

Friday, 19th of April, U.K Retail Sales – having endured a rather wild trading cycle, Great Britain will deliver one more important economic report to end this week. The GBP/USD will react to the consumer spending results.

Forex Volatility and Coming Data Attractions for this Week

Nervous trading results have hurt many day traders and likely financial institutions too, as behavioral sentiment in Forex gets blindsided by rather mixed U.S data and the Federal Reserve not giving a definitive answer regarding monetary policy. The violent trading in the USD last week was expected, but the turbulence that many Forex pairs experienced on Thursday and Friday of last week was rather vicious. For all the perceived sophistication of Forex markets via financial institutions, the trading results last week point to a definite fear of the unknown.

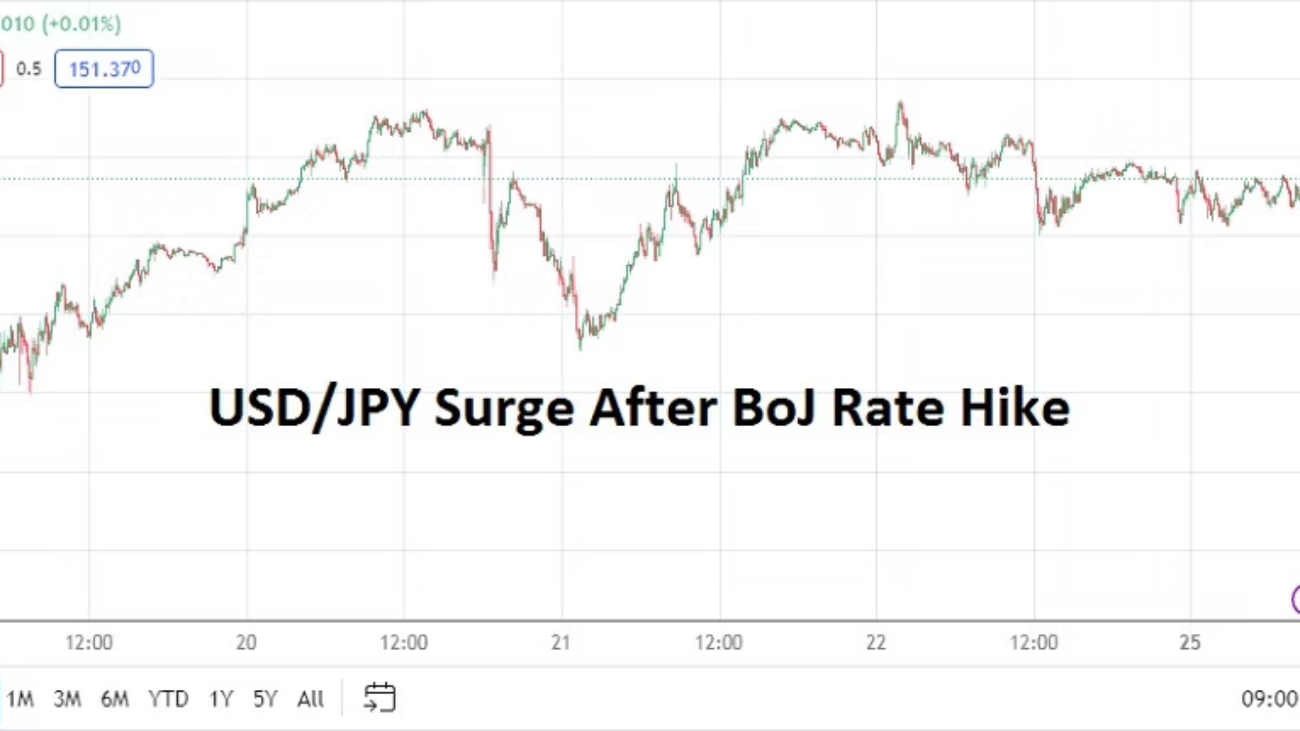

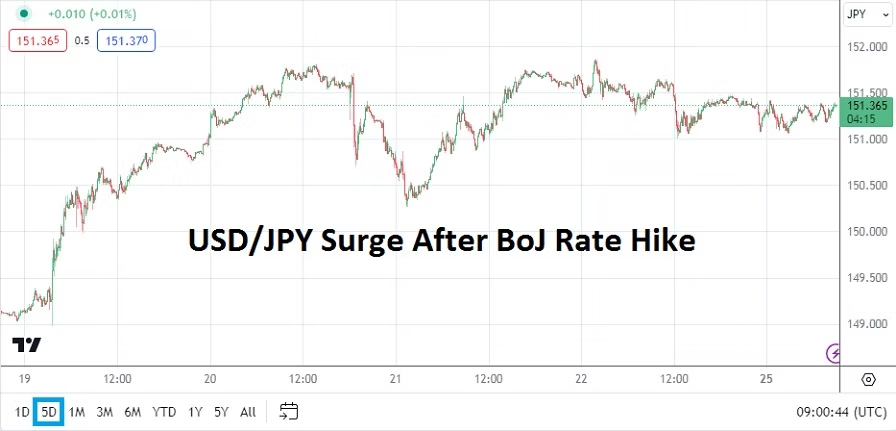

USD/JPY Five Day Chart as of 25th March 2024

While the Bank of Japan finally changed its interest rate policy and moved to a Policy Rate of 0.10% early last week, this did not create selling momentum in the USD/JPY. The Federal Reserve’s dangling of potential interest rates to come this year caused temporary weakness in the USD, but as financial institutions and their clients looked at the prospects for a more dovish Fed they apparently became unimpressed as the days passed.

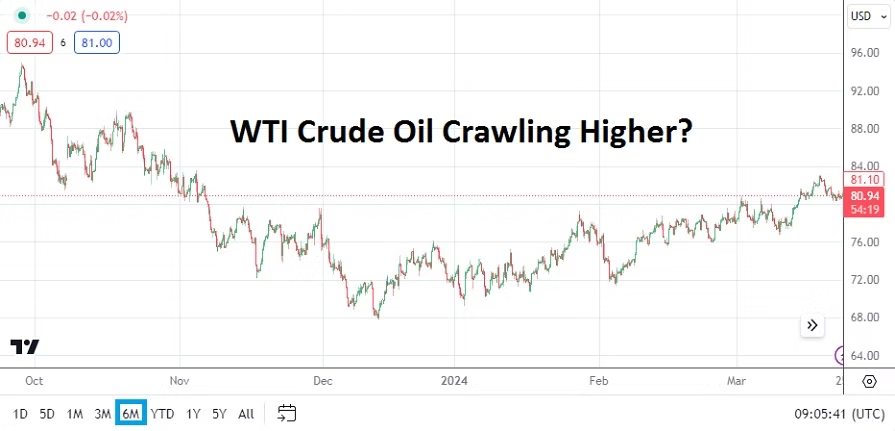

WTI Crude Oil Six Month Chart as of 25th March 2024

The Fed seems to be betting on weaker jobs numbers developing, and there has been data which points to part-time jobs increasing, and full-time jobs becoming harder to find in the States. Jerome Powell said last week that if jobs numbers start to show weakness that the Fed would be willing to begin cutting interest rates even if inflation remains sticky. Lagging economic data correlations have not eased the Fed’s problems.

The Fed has also admitted inflation in housing, transportation and food remains problematic. WTI Crude Oil spent much of last week above 80.00 USD per barrel as its price has begun to show signs of rising incrementally again; and there is little the Fed can do about more expensive energy costs should they be seen. Higher costs for logistics will not make anything cheaper. Pricier mortgages, more expensive rent and insurance rates for cars and gasoline is creating serious knock on effects.

And for the sake of acknowledging the screaming prices in Cocoa, please have a look at the chart below which should explain why your chocolate products are going to be more expensive in the coming months. The price of the most delicious commodity in the world has tripled in less than a year’s time and is around 8931.0 USD per metric ton as of this writing.

Cocoa One Year Chart as of 25th March 2024

Gold turned in a violent week of trading too as it reached 2224.00 last Wednesday, only to fall back to a known value around 2165.00. Day traders are dealing with violent cycles in Forex because sustained trends have been nearly impossible to find. While U.S equity indices are fighting upwards, speculators who are afraid of heights are likely being cautious if they are betting merely on the daily results from the S&P 500, Nasdaq 100 and Dow Jones 30 instead of investing for the long-term.

This week’s coming data from the U.S is important, financial institutions are already dealing with plenty of noise, and they will have to be careful regarding their interpretations regarding the coming economic statistics. Meaning day traders who are speculating in all financial assets should use risk taking tactics that are planned significantly in advance.

Monday, 25th of March, U.S New Home Sales – a slight gain is expected, but mortgage rates continue to shadow the housing sector and cause concerns.

Tuesday, 26th of March, U.S Consumer Confidence via the Conference Board – the reading is anticipating a slight increase. Consumer numbers from the U.S have come in mixed recently. A stronger result than estimated might not be welcomed by traders with bearish sentiment regarding the USD. The Fed wants its cake and to eat it too, they would like to see weaker consumer numbers and a soft economic downturn. If U.S shoppers remain confident this could help sustain inflation. It should be noted too, that Core Durable Goods Orders data will be released one and a half hours before the Consumer Confidence numbers.

AUD/USD Six Month Chart as of 25th March 2024.

Wednesday, 27th of March, Australia Consumer Price Index – inflation numbers are expected to come in slightly higher than the previous results. Like most other central banks, except for the BoJ, the Reserve Bank of Australia would enjoy seeing inflation erode. The AUD/USD will react to the results certainly, but the price action might prove complicated because of USD centric notions.

Thursday, 28th of March, U.S GDP, Weekly Unemployment Claims, Pending Home Sales, and Revised Consumer Sentiment from the University of Michigan – put bluntly day traders will have to be well prepared for the combination of data from the States. Spectators who do not have large trading accounts and cannot take on a great amount of risk, should seriously consider sitting on the sidelines until most of the data is published. The GDP numbers will be watched carefully, while they are expected to match last month’s total, any surprises will affect the USD immediately in Forex. Weaker growth numbers might cause USD sellers to ignite positions.

However, before traders react too much to the Gross Domestic Product numbers, the Weekly Unemployment data will also impact the financial market. Financial institutions are anticipating a higher amount of unemployment claims this week. Also, at the same time as the growth and jobs numbers, the Final GDP Price Index numbers will be brought forth. The mixture from these reports could cause speculative whiplash.

The housing sector numbers and consumer numbers which come one and a half hours later will finish off a very big day for traders and institutional investors. The wide array of data could make this coming Thursday rather loud, and again rather dangerous for retail traders to participate.

Friday, 29th of March, Japan’s Tokyo Core Consumer Price Index – the inflation numbers are expecting to show a slight decrease to 2.4%. The result should certainly be watched by USD/JPY and GBP/JPY traders. If the number were to come in higher than expected, this could cause additional volatility for the Japanese Yen. Financial institutions seemed to indicate last week they would like to see the BoJ become more aggressive with their Policy Rate.

Friday, 29th of March, U.S Core Personal Consumption Expenditures Price Index – the reading is expected to be below the previous month’s total. Traders should be on the lookout for revisions to past results. Financial institutions know this inflation number is important for the Federal Reserve, but they are concerned the U.S central bank doesn’t have the ability to combat inflation which is not part of the Core number. Energy and food costs which are hurting U.S consumers are not part of this report and likely making the Federal Reserve gun shy regarding monetary policy – which has caused a large part of the USD whipsaw trading results that Forex has experienced.

AMT Top Ten Miscellaneous Insights for the 9th of February

10. Super Bowl AMT Prediction: Kansas City Chiefs 27 – San Francisco 49ers 24. After winning the MVP Travis Kelce will hug Taylor Swift and announce his retirement.

9. Jazz Fusion: Please listen to the song School Days played by Stanley Clarke while delivering a supreme bass guitar riff.

8. Tech: Google has announced its Bard A.I will now be known as Gemini in a rebranding. ‘Bard’ was a rather poor name, but is Gemini much better? Let’s ask Gemini what it thinks about the Google marketing team.

7. Banking Animal Kingdom: Central Banks parroting the same rhetoric globally as they choose to be ‘prey’ instead of ‘predators’, driving financial institutions and traders batty in Forex.

5. Deutsche Pfandbriefbank AG: A large slump in bond values for the German bank has sparked additional fears of exposure for banks involved with the commercial real estate sector. CRE appraisals remain unrealistically high in many European and North American cities as lending risks climb.

4. Cocoa: The price for the commodity was 4055.00 USD per metric ton on the 8th of January, as of yesterday it was 5666.00, a rise in cost of 39.72% in a month. Our sweet tooth just got more expensive.

2. China Economy: Deflation continues to be reported via the CPI and PPI statistics. Also, value of properties for housing and commercial real estate face significant headwinds. The real estate sector including ancillary infrastructure is at least 21% of China’s total GDP.

1. Risk Appetite: U.S equity indices finished Thursday’s trading achieving apex highs. The S&P 500 is challenging the 5000.00 level. Gold is near 2033.00 USD and WTI Crude Oil is above 76.00 USD as of this writing.

Nervous Trading Results End of Last Week Serve as Caution

The end of last week saw mixed U.S inflation data and lingering nervous sentiment regarding outlooks about U.S Treasuries, create rather choppy conditions for day traders. Economic data this week should be more calm because there appears to be less significant risk events on the horizon. Financial institutions finished Friday within a USD buying mode, a bearish gold trend, and U.S stock indices declining – highlighting fragile conditions remain evident among larger market players.

NZD/USD Six Months Chart as of 13th August 2023

Monday, 14th of August, New Zealand Business Services Index – this report may turn out to be the highlight of the day for some traders. The NZD/USD which will start tomorrow near values last seen in the middle of November of 2022, may find interested speculators glancing at the report. But the NZD is moving largely under a USD centric driven market, like most of the broad Forex market. Mid and long-term technical support levels are certainly in focus, and they have proven vulnerable recently as the NZD/USD trends lower.

Tuesday, 15th of August, China Industrial Production – economic data from the nation has been troubling regarding deflation. However, traders who lean towards a ‘Western’ bias should remember to keep their perspectives realistic, because weaker China economic results mean the global economy is struggling too. A slight decline in Industrial Production is expected. Weaker than expected numbers from China could indicate ‘soft’ demand via export partners.

As an aside financial institutions will keep their eyes on the China real estate market too, this as whispers about ‘Country Garden Services Holdings’ funding problems remain a talking point and potentially escalate. Values of properties are suffering from declines too in China and this is hurting the domestic economy.

Tuesday, 15th of August, U.S Retail Sales – a slight gain in spending by U.S consumers is expected to be seen. If the number can meet the anticipated gain of 0.4% the result may not spark too much volatility. If for some reason a higher outcome is produced, this could spark some concerns about U.S Federal Reserve rhetoric. Although it may seem counter-intuitive to some traders, a weaker number could help ignite some bearish selling of the USD.

Wednesday, 16th of August, New Zealand Official Bank Rate – the interest rate policy from the RBNZ is expected to remain in place. Although it should be noted both New Zealand and Australia have almost made it a habit to surprise investors over the past few months.

Wednesday, 16th of August, U.S FOMC Meeting Minutes – the report will be studied for clues regarding outlook. However, the Fed has a well-practiced ability to maintain tight lips and not disclose too much internal thinking, particularly when it comes to disagreement regarding policy – which is seemingly escalating in the Federal Reserve.

Thursday, 17th of August, U.S Weekly Unemployment Claims and Philly Fed Manufacturing PMI – in what has likely been a quiet week of data leading up to these reports, some analysts may try to get the attention of their clients regarding these results to create ‘noise’, but unless there is a strong miss the data is likely to simply be digested quietly into the broad marketplace.

GBP/USD One Week Chart as of 13th August 2023

Friday, 18th of August, U.K Retail Sales – last week’s better than expected GDP numbers from Britain will make the outcome of this consumer data rather intriguing. The GBP/USD could find some impetus from the results. The estimate is calling for a decline of minus -0.4% compared to last month’s gain of 0.7%. The GBP/USD which went into last weekend near lows will likely find plenty of attentive traders as this new week comes to a close.