Plenty of Data from the U.S and China Should be Anticipated

As the last week of August trading gets ready to begin, day traders may be glad to put the past month behind. The BRICS Summit and Jackson Hole Symposium delivered soundbites as promised last week, but there were few surprises. Forex, equities and commodities have been supplying a bumpy road for a while and may continue to do so.

Behavioral sentiment in the broad markets remains fragile, this as short-term U.S Treasuries continue to allure institutional players looking for solid returns. Some well known market players continue to issue cautious words regarding U.S equities, but the three major indices are still near mid-term highs. We have yet to experience a blood curdling selloff in the U.S equity markets. This maybe producing choppy results for some day traders pursuing CFDs while betting against higher moves.

Which brings up the question, which quantified analysis do you want to act upon? While the major U.S indices are up, a lot of the market action in these indices are driven by the ‘top performers’ which have ‘floated the boat’ while many other stocks have not performed handsomely.

Retail traders who are wagering on daily fluctuations need to understand there is a vast difference between short-term speculative positions and long-term investments. Hence the reason day traders are reminded to only bet money on what can be lost without a great deal of discomfort. Speculation should only be done with a very limited amount of cash, because day trading never offers guaranteed profits.

The next handful of days will deliver plenty of important data. The question is how financial institutions will react as they weigh the coming results against their own sentiment and outlooks regarding mid-term interest rates via the U.S Federal Reserve’s rhetoric. Market nervousness remains on edge as more tranquil days are certainly sought via risk adverse financial decisions.

The cryptocurrency market should be watched carefully by participants within its volatile assets. Bitcoin continues to trade near the 26,000.00 level and this is considered important support by many. And Binance coin has failed to inspire a sustained upwards reversal as Binance exchange remains under legal and regulatory shadows.

Traders are also advised to note the U.S will be on holiday on the 4th of September, the coming long holiday weekend could spark rather dynamic market action Thursday and Friday as financial institutions trade in advance of Labor Day.

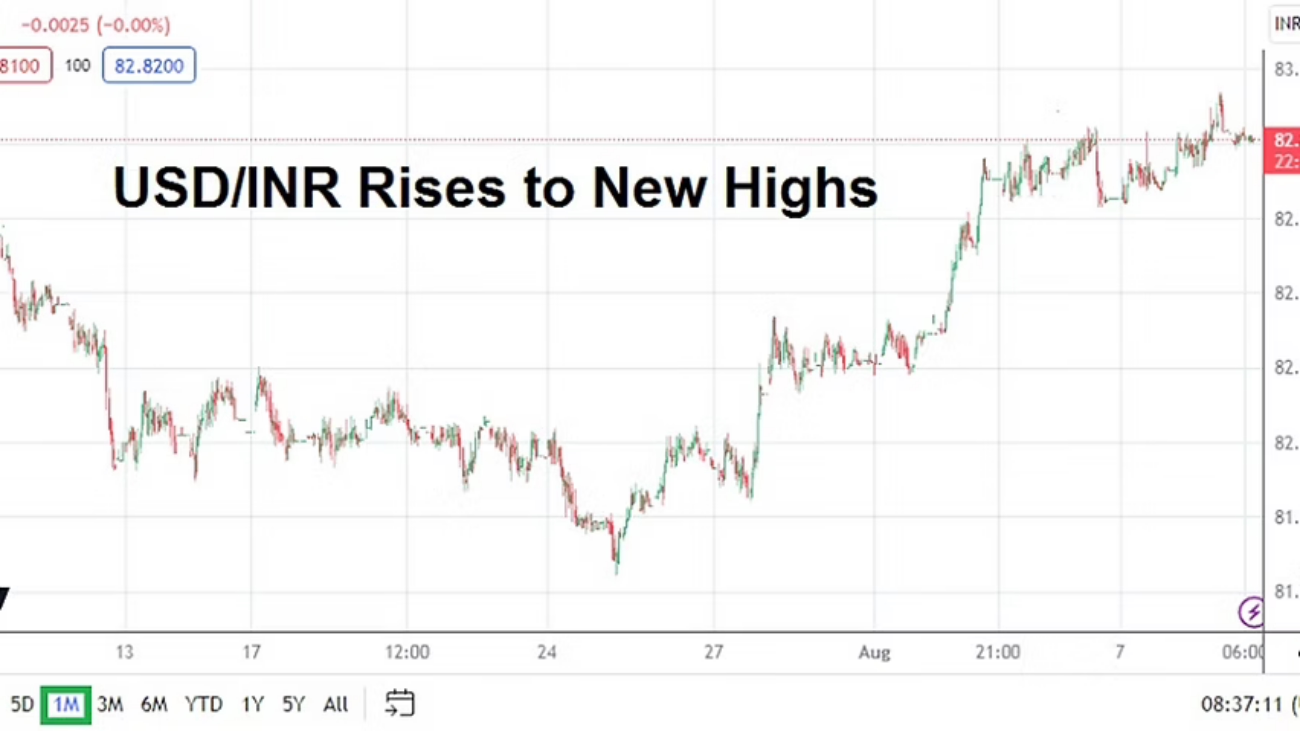

Monday, 28th of August, Australia Retail Sales – the numbers will cause a reaction in the AUD/USD and the result is expected to be slightly better than last month’s outcome. The AUD/USD is near important long-term lows.

Tuesday, 29th of August, U.S Consumer Confidence via The Conference Board – the anticipated result is lower than last month’s reading. However, the past three months have done better than expected, which may put some analysts on edge before the publication.

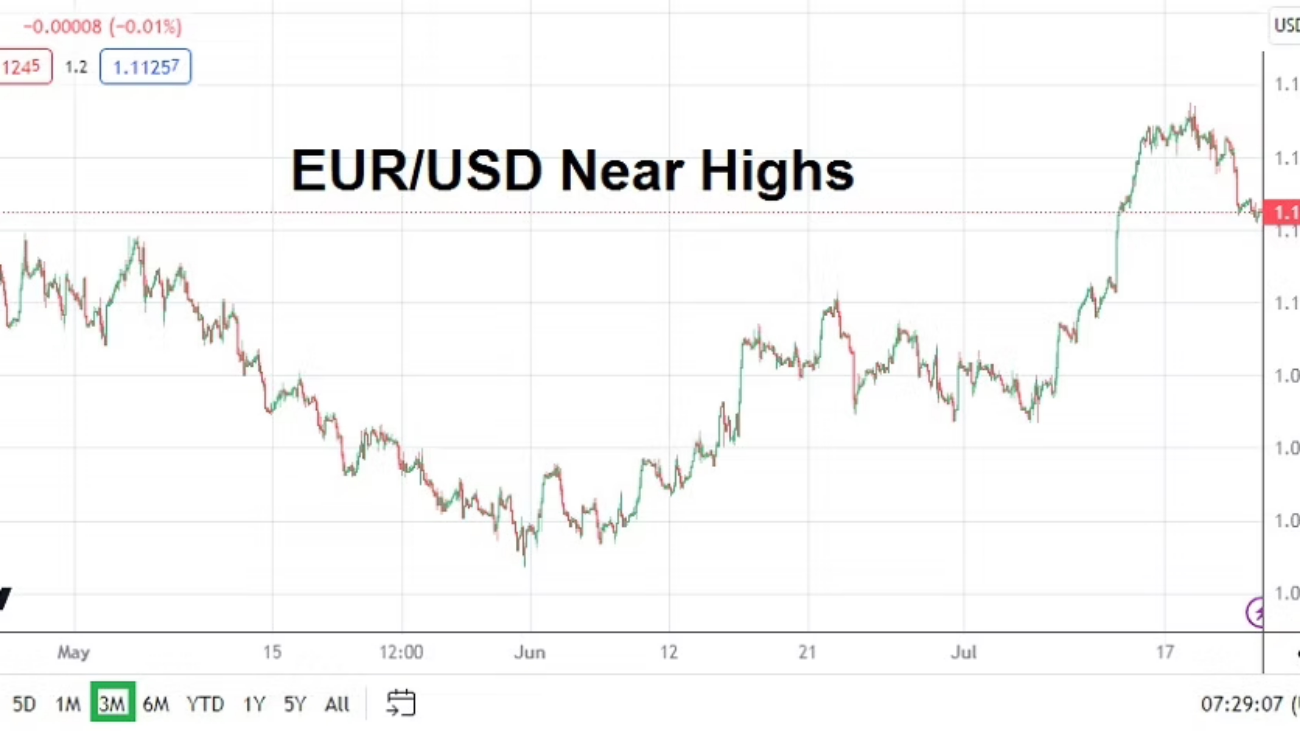

Wednesday, 30th of August, Germany Preliminary Consumer Price Index – the inflation numbers are expected to match last month’s gain of 0.3%. The EUR/USD will react to the outcome with momentary volatility. German economic data has been a concern in the European Union for a handful of months.

Wednesday, 30th of August, U.S Preliminary Gross Domestic Product and GDP Price Index – the numbers from the GDP reports will be watched by most financial institutions. Last month’s numbers surprised traders, this as growth remained quietly stubborn and inflation crept higher. The USD has been a powerhouse against the GBP and EUR recently. If these GDP reports surprise to the upside again, this could spark more buying of U.S Treasuries which could create additional strength in the USD.

Thursday, 31st of August, China Manufacturing PMI – the results from the Purchasing Managers Index from China since April have been lackluster and showed weak export demand globally. Economic data from China has sparked concerns from international investors, and the USD/CNY has certainly received attention as it has risen steadily and is now challenging highs from late October and early November 2022.

Thursday, 31st of August, U.S Core PCE Price Index – the Personal Consumption Expenditures data is expected to match last month’s gain. This inflation data, and the GDP Price Index numbers from the day before will certainly get a reaction from financial institutions which would prefer to see no surprises higher.

Friday, 1st of September, U.S Non-Farm Employment Change and Average Hourly Earnings – as always these reports could shake market sentiment instantly. However it is the wages data which will likely be a focal point for investors. If wages can come under last month’s gain of 0.4%, this would be welcomed by investors and they may go into the long U.S holiday weekend a bit more calm regarding the Federal Reserve.