AMT Top Ten Miscellaneous Tastings for the 10th of May 2024

10. Word of the day: Ultracrepidarian is a person who speaks assertively about subjects that are beyond their level of knowledge. The world is full of many suspects ladies and gentlemen.

9. Steve Albini: The musician and production sound engineer passed away earlier this week in Chicago. Albini was a pioneer and leader in ‘alternative’ music and battled homogenized corporate music for nearly 40 years. Nirvana, Fugazi, Jimmy Page, the Pixies, P.J Harvey are some of the many that worked with Albini.

8. Bitcoin: BTC/USD continues to hover around the 63,000.00 realm per a three month technical chart perspective. Bitcoin’s higher values via one year results are being maintained. BNB/USD is lurking near 600.00 per a three month glance.

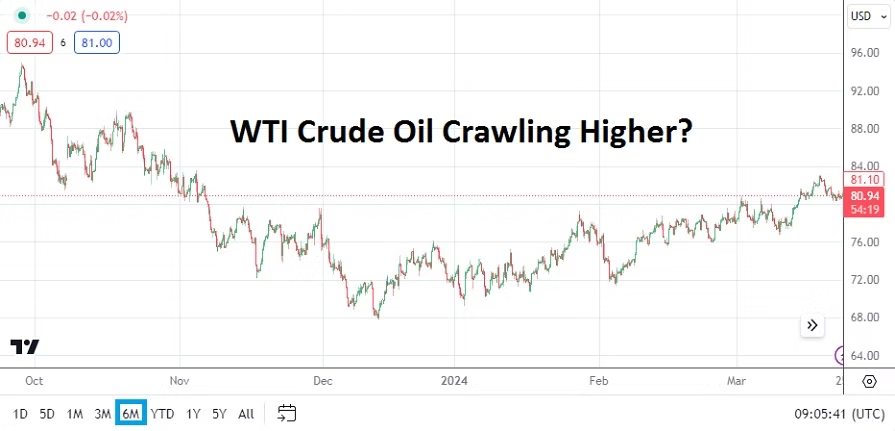

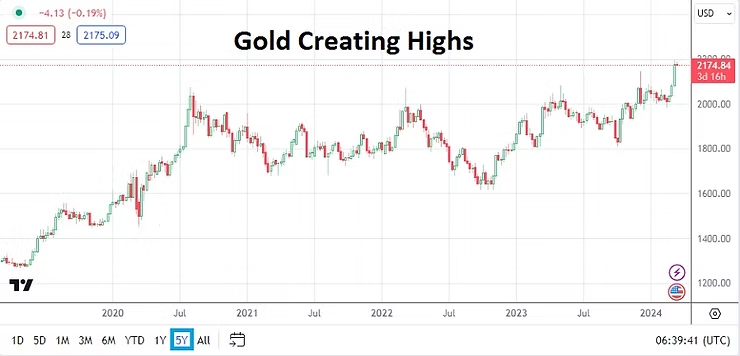

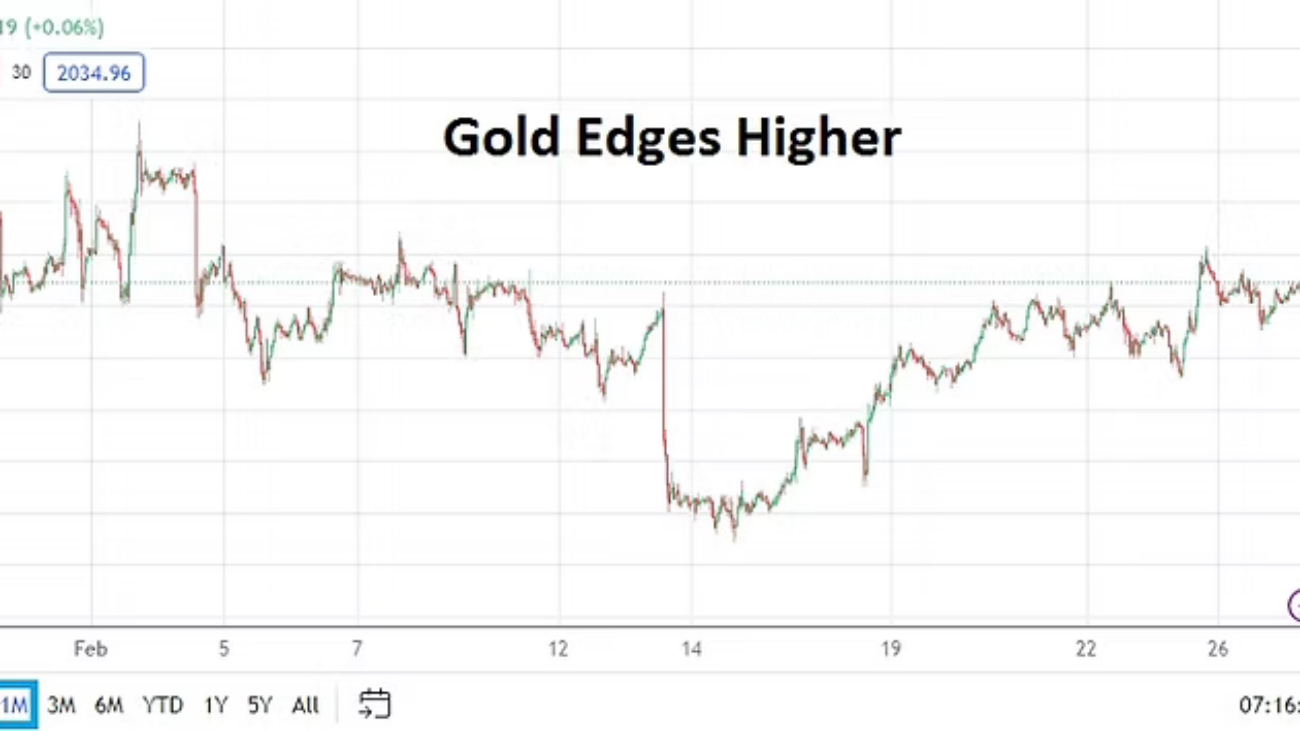

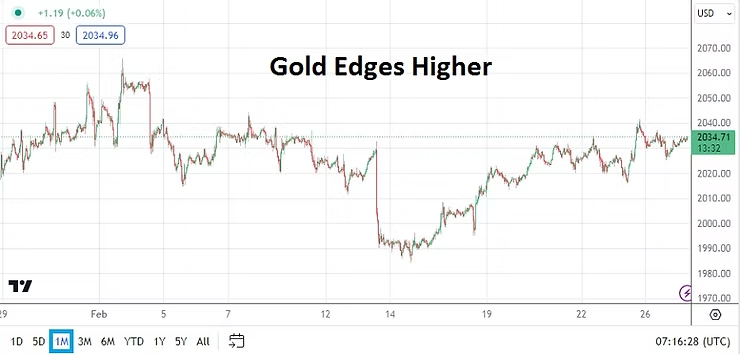

7. Commodities: Cocoa and Coffee prices remain elevated. After touching a low around the 7,250.00 USD mark last week per metric ton, Cocoa is now within sight of 9,000.00 USD again. Retail speculators who like to wager via CFDs on commodities need to remember their bets have no influence on the markets, which are in complete control by the largest players in the commodities sector.

6. Wayve Technologies: A U.K based company specializing in autonomous driving software has announced they have raised more than 1 billion USD in investments recently via the likes of Softbank, Nvidia and Microsoft. The U.K government has highlighted Wayve, proclaiming it shows Britain will be a major force in AI development. Wayve was established in 2017 and is still a privately held company.

5. U.S Foreign Policy: Election concerns appear to be a prime motivator for the U.S executive branch as its attempts to walk a fine line regarding diplomacy and saber-rattling in the Middle East. Polling from a variety of sources indicate Joe Biden is in jeopardy of not being reelected.

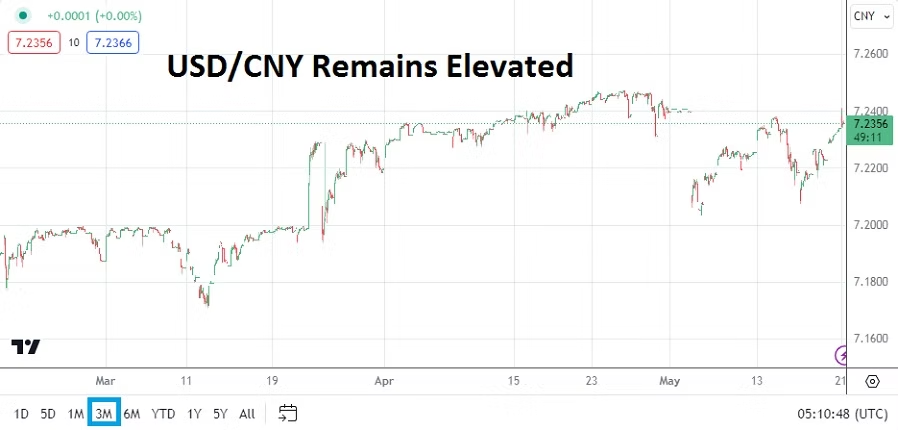

4. USD/CNY: China will release its Consumer Price Index and Producer Price Index numbers early on Saturday. The USD/CNY is trading around the 7.2245 mark as of this writing. Some analysts have expressed concerns about the China Yuan weakening via attempts by the Chinese government to boost exports. The USD/CNY certainly remains within the higher elements of its range, but is below marks seen in early September 2023 which were around the 7.3425 ratio.

1. Equity Indices: Bullish optimism has been seen in the S&P 500, Dow 30 and Nasdaq as all three major indices are ready to start the day near highs for the week. The burst of upwards momentum which started last Thursday, has ignited the major U.S indices within sight of their apex realms achieved in late March and early April.