Reflections on a Disappearing Workforce and a Long-Term Strategy

Tamil Nadu is one of the fastest growing States in India with an impressive Gross State Domestic Product result of 11.9% in financial year 2024-2025. Despite the former Dravida Munnetra Kazhagam’s (DMK) government being unseated by the new party Tamilaga Vettri Kazhagam’s (TVK) in State elections recently, Tamil Nadu has continued to attract billions of USD. Automobiles, information technology (IT), electronics, and high-end engineering from global investors continues to be alluring.

As a student of economics, I have looked at and questioned how far this growth has helped raise wages and create jobs. In other words, will these investments help create linkages across the Tamil Nadu economy and generate deeper opportunities? Tamil Nadu may have higher GDP growth than any other State economy in India, but its growth is highly skewed towards a relatively small number of sectors.

India Insider: What Do Rural Areas Say About the Nation’s Fast Growing Economy?

As noted, some of these sectors that attract investment generate high output, but employ a relatively small share of the workforce. As a result the gains are not spread evenly across the labor force.

Since the informal workforce constitutes a large share of employment in Tamil Nadu, many companies rely on contract labor that has created limited individual bargaining power. This is evident in many automobile, textile, and mobile phone assembly plants in Chennai.

I knew a friend who worked in a mobile phone assembly plant in 2019 and despite completing a Bachelor of Engineering degree, he earned only around USD 150 per month. Since employees have weaker bargaining power, wages do not rise even as inflation increases every year.

Many people leave these companies within one or two years. However, companies do now worry, because these firms can recruit replacements because the supply of educated workers remains high relative to demand. Tamil Nadu produces a higher number of graduates every year, and it knocks down the wage bargaining power of workers, allowing the formal economy to employ a multitude of people without having to raise wages

In the 1990’s these conditions weren’t prominent because there were fewer people who had accomplished university studies and graduation. Getting into the formal economy became easier and capital started to flow after the end of the License Raj era controls in 1991, this when India opened up it’s economy for foreign direct investment.

In the last two decades, Tamil Nadu’s industrialization has become heavily concentrated in cities such as Hosur, Chennai, Tiruppur and Coimbatore. Despite strong outbound trade, the State records an overall trade deficit. This also means some districts are performing well, while others remain heavily dependent on agriculture or services to generate Gross District Domestic Product (GDDP).

Pudukkottai District as a Case Study

I was doing some field surveys in Pudukkottai district, especially in the town and surrounding rural areas. And since we have no clear up-to-date Census numbers, we have to rely on the 2011 Census to understand the composition of Pudukkottai district’s economy.

According to the 2011 Census, Pudukkottai district is heavily dependent on agriculture, accounting for roughly 45–55% of employment. An important parameter to examine in the next Census will be whether this composition has changed.

Because the census is not giving us clear answers, we need to conduct random surveys across multiple villages to understand the reality. And during my visits around Pudukkottai, I consistently saw people mainly below the age of 20 and above the age of 50. Why?

This was the case in numerous villages around Pudukkottai. Still, we need stronger evidence. I repeated this exercise across different time periods to understand whether the pattern remained the same. The result was remarkably similar regarding ages.

Interestingly, the predominant working age population of India – between 25 and 40 years old – is largely absent from villages and even from Pudukkottai town, although I did see some from this age group employed in the service sector.

Where Did These Missing Workers Go?

The single reason lies in Pudukkottai district’s relatively high agricultural productivity. Since the service sector accounts for only around 30–35% of employment, the district still relies heavily on agriculture and allied activities for income generation.

That model has weakened over the last fifteen years. Lack of small scale manufacturing industries has crippled employment opportunities. Unlike Coimbatore or Tiruppur, Pudukkottai has attracted relatively few large manufacturing or technology investments. Economic growth has therefore remained dependent on agriculture, small businesses, and government employment.

Another important aspect is that many small businesses in the service sector are struggling or have closed altogether in Pudukkottai compared to 2016 because of weak local consumption. This is because people are migrating. That is clearly visible, and businesses cannot survive without a sufficient working age population. While Pudukkottai’s district’s population may have grown, much of the increase may have occurred in rural areas and been offset by outward migration of working age adults to Chennai, Bengaluru, Singapore, Malaysia, the Gulf countries and other employment centers.

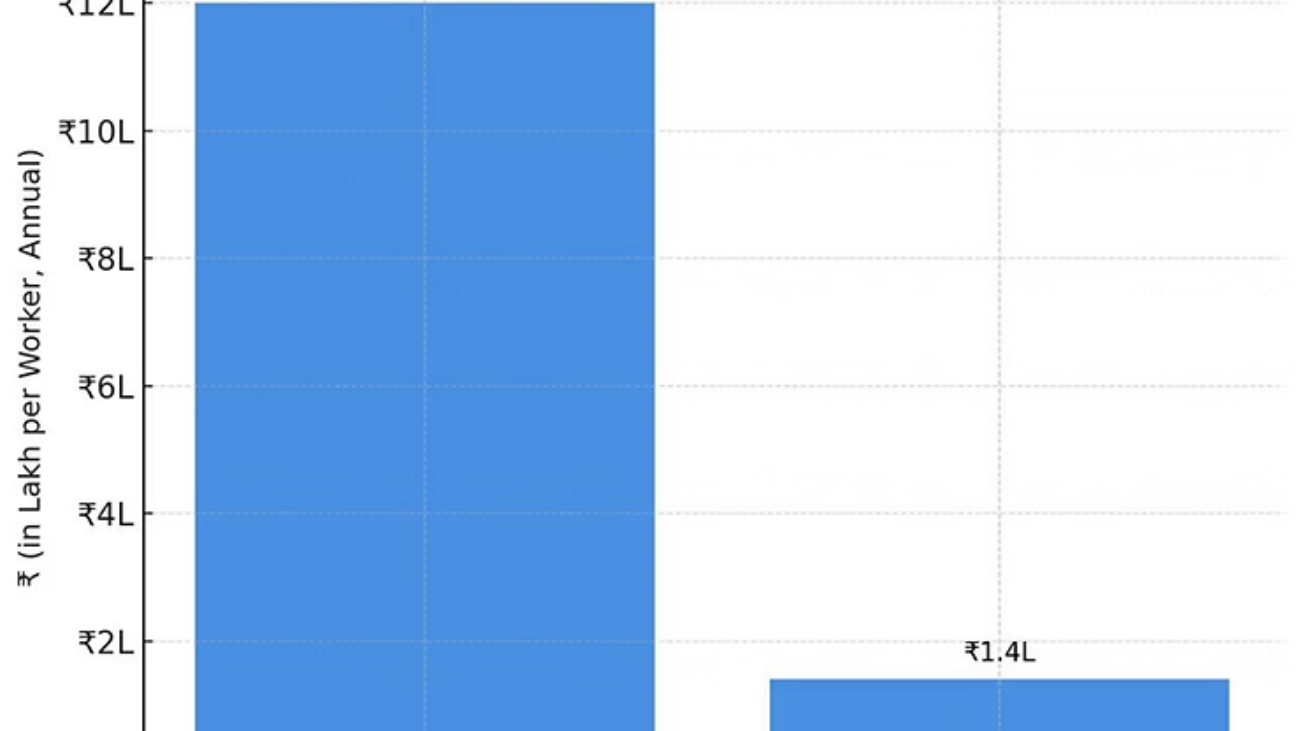

The difference is also reflected in income levels. Recent district estimates place Coimbatore district per capita income at around ₹4.1 lakh, while Pudukkottai’s is approximately ₹2.4 lakh. The gap reflects differences in industrialization, labor productivity, and the availability of high value employment rather than population alone.

The next Population Census and the Periodic Labor Force Survey (PLFS) will be important in determining whether outward migration and changes in employment composition support these observations. Indicators such as graduate unemployment, labor force participation, regular salaried employment, and sector wise employment will provide a clearer picture of whether Tamil Nadu’s growth is creating quality jobs.

Limited industrial growth will become a much bigger challenge for Tamil Nadu over the coming years if unemployment among educated youth continues to remain high. Pudukkottai district is a classic example of that challenge.

India’s fast growing economy needs proactive business policies in small towns, together with the infrastructure needed to attract manufacturing and private investment. Depending primarily on IT hubs or remittances from the Gulf and Southeast Asia is not a sustainable long-term strategy.