Leverage and the Holidays Often Leads to Costly Volatility

This may seem like an unfriendly reminder for this time of year, but holiday trading can lead to dangerous storms for traders. Keeping a realistic viewpoint regarding your ambitions during Christmas and New Year’s is important.

Most day traders cannot afford to have an outlook that is beyond the short and near-term. This is an ugly fact many speculators with less than deep pockets have to acknowledge if they are new to speculating. While large traders and financial institutions can maintain mid and long-term outlooks, day traders who do not have the funds to keep overnight positions need to operate in an entirely different fashion.

Trends via technical charts and fundamentals are crucial for all traders. Behavioral sentiment is a key ingredient too for all participants chasing assets. However, day traders also need to understand unique risk management limitations. The use of leverage is a vital dynamic, and can cause devastation fast when too much money has been wagered. The use of leverage by day traders effectively raises the probability that a trade will lose money.

Incremental changes in value to a Forex pair, commodity and equity share being traded on a brokers platform by a speculator using ‘borrowed’ money via an account that allows for margin often leads to quick outcomes that fail. Many brokers offer traders ‘polite’ leverage ranging from 10% to 100% in extra funds, this while enticing the speculator to the potential of profiting in a quicker and more robust manner. It should also be noted that when a broker is offering vast amounts of leverage, they are knowingly increasing a traders likelihood of losing. The use of leverage beyond 10% leads to plenty of expensive mistakes.

Unfortunately, the simple truth is if you can make fast money trading, you can lose fast money while trading. The use of the word speculating is simply a gentle way of not using the word ‘gambling’.

Traders tempted to pursue wagers during the next couple of weeks should remember a lack of normal volumes make many asset classes more volatile, meaning the use of leverage by speculators often leads to dangerous gyrations within their accounts.

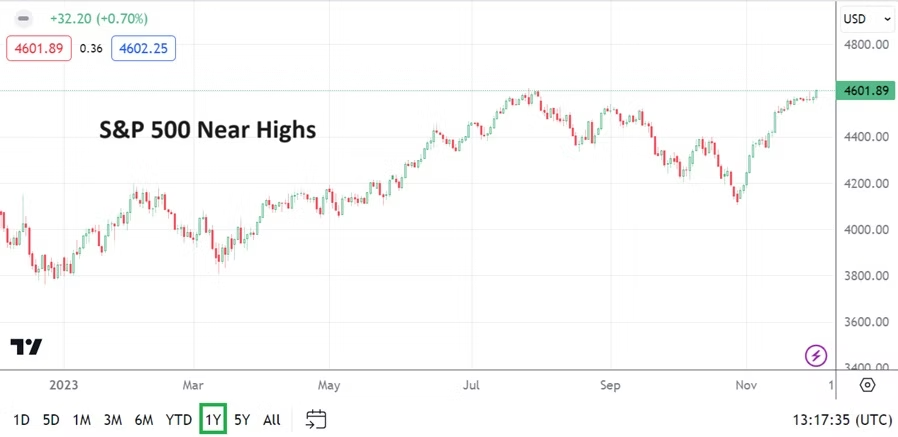

Risk appetite has taken on a optimistic tone globally because of the upside U.S equity markets have been producing, while U.S Treasury yields are decreasing, but dangers still lurk. Day traders need to remain realistic regarding their pursuit of quick hitting trades during the holiday season, and make sure they use solid tactics while pursuing their outlooks. The trend may appear to be your friend, but short-term reversals in the wrong direction can cost money.

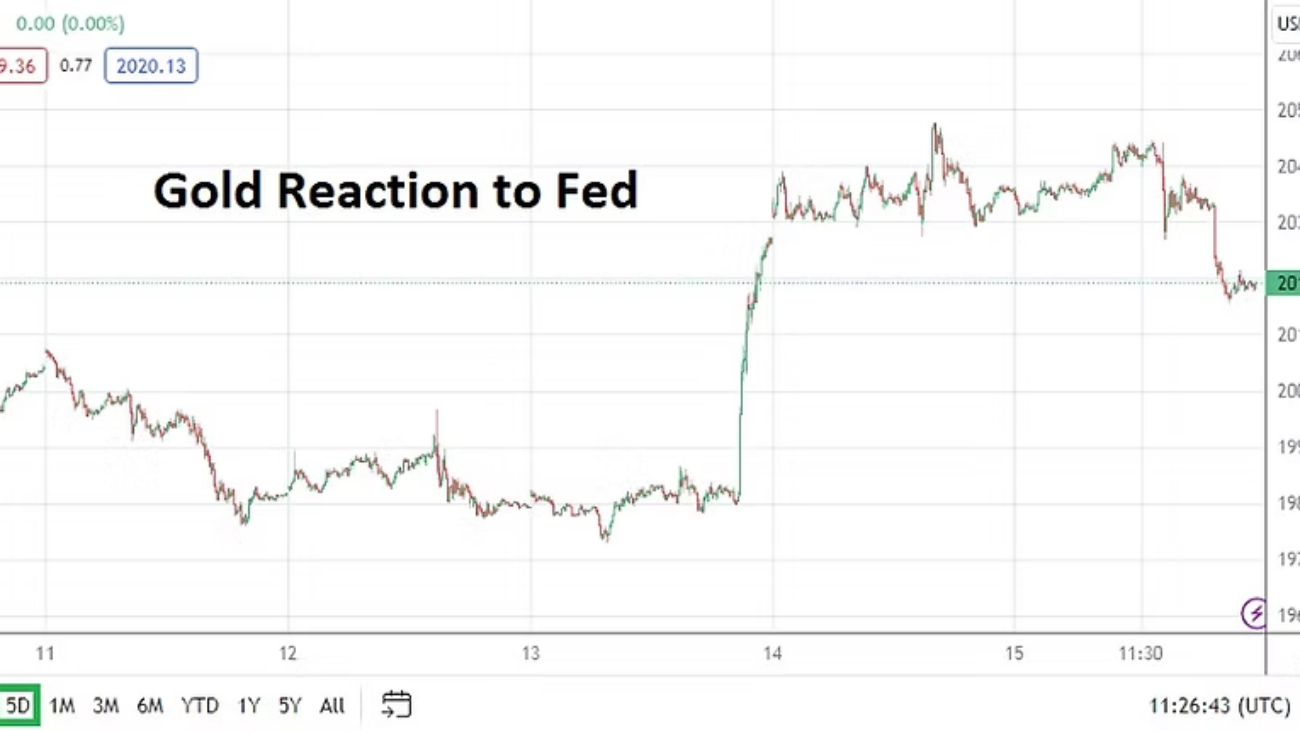

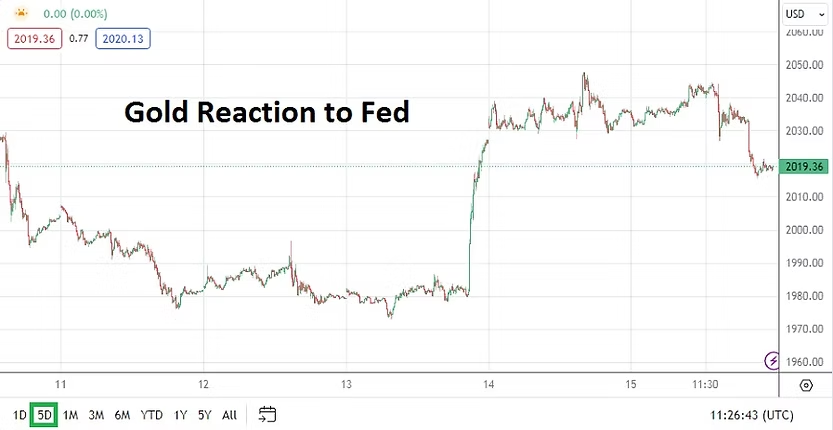

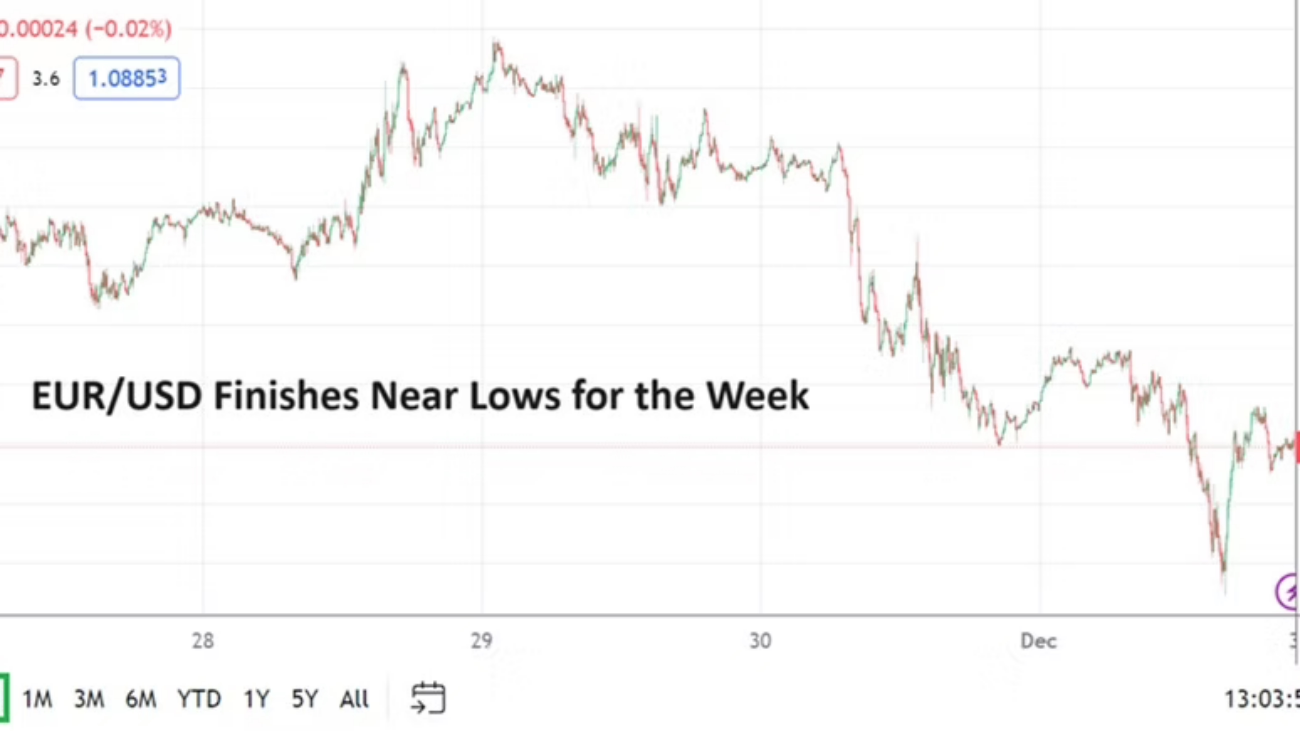

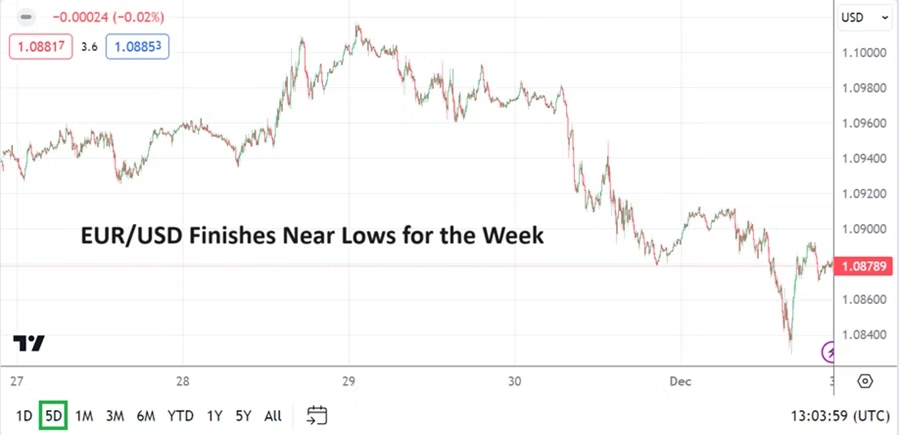

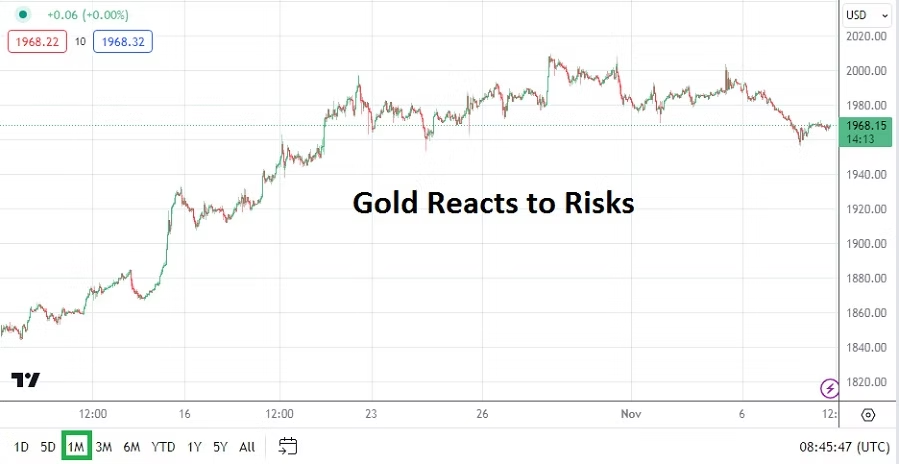

No one wishes for bad things, but speculators should also note that if risk adverse events occur during the holidays, that ‘negative news’ can often become amplified this time of year and cause more volatility. Speculative positions in Forex, Crude Oil and gold can produce rather wild results, and thin trading volumes can add to the swift changes in values.