Impolite Opinion: BRICS Long-Term Plans & Implications Part 1

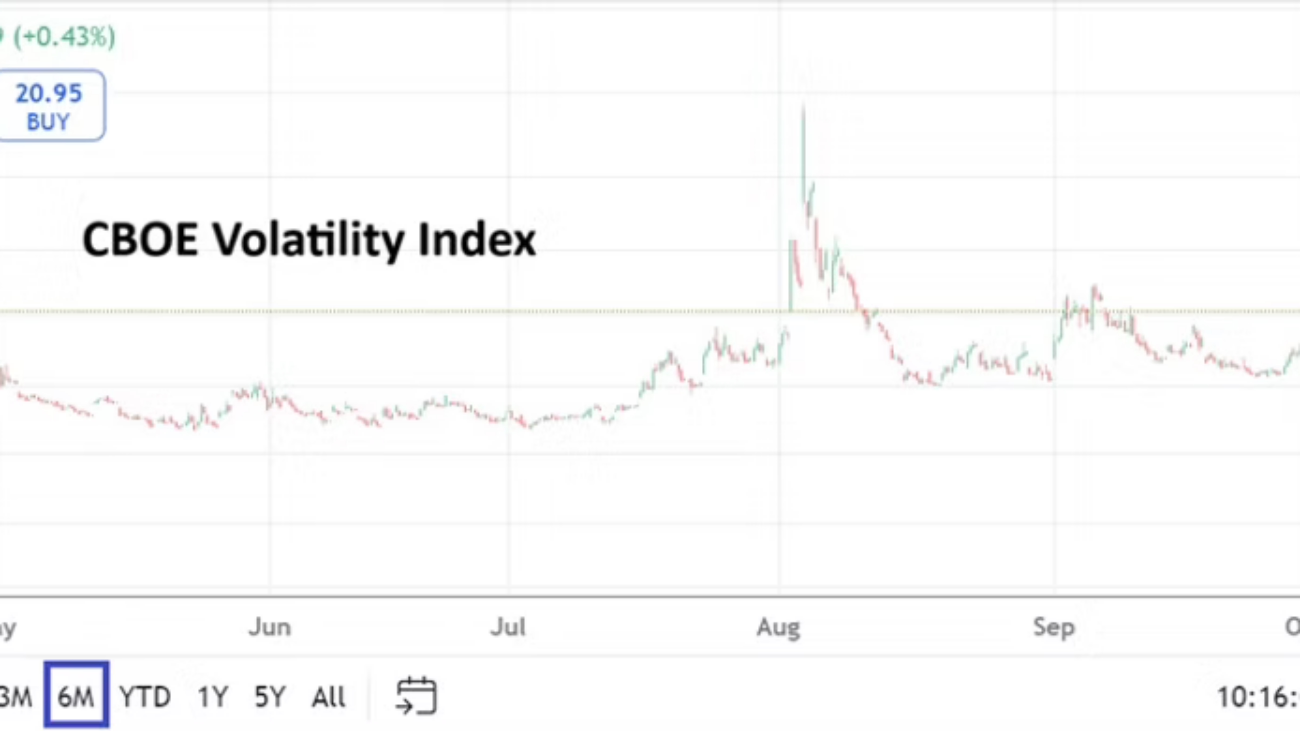

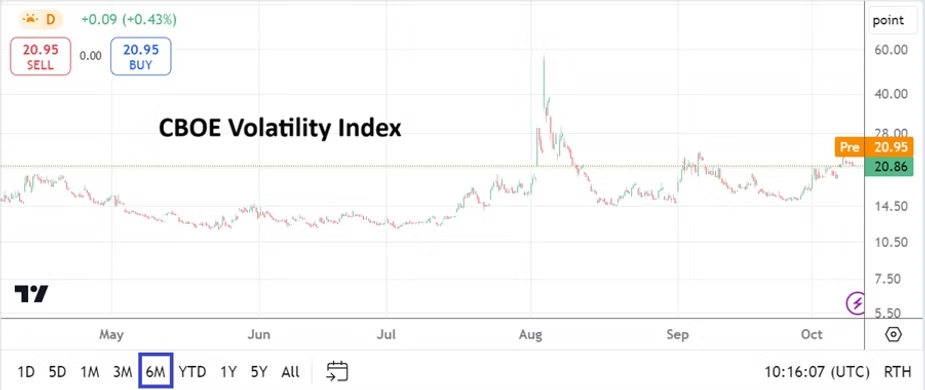

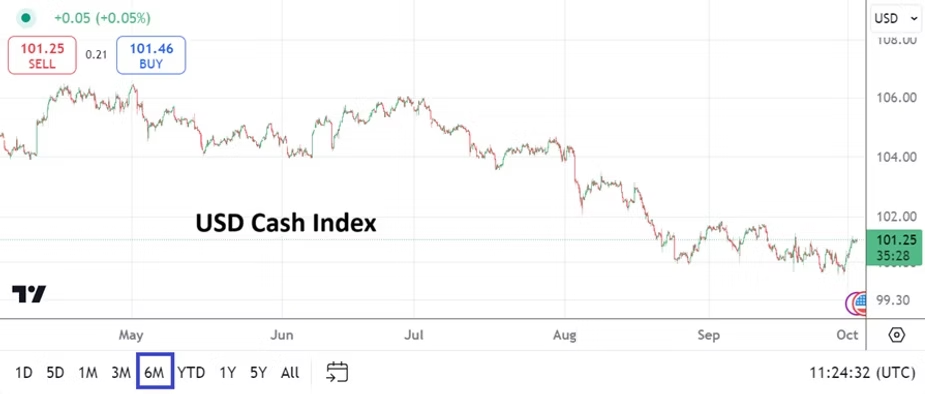

The global Forex market is spastic and many major currencies are traversing within weaker whipsaw value ranges against the USD. The currency pairs are trading in price bands seen before the Fed cut its Federal Funds Rate by 0.50 basis points on the 18th of September. And there is still one and a half weeks of assured volatility that will be demonstrated. Crucial U.S data is on the schedule in the coming days via the Advance GDP and Non-Farm Employment Change statistics, and the U.S Presidential election is edging closer. Israel and Iran continue to play a game of cat and mouse in the Middle East, which thus far has led to a controlled chaos and not worldwide bedlam. Financial institutions have plenty of reasons to be apprehensive.

Expansion of BRICS Feels Inevitable

Now let’s turn our attention to a tectonic foundational shift building in global trade and geopolitics. Attention on short-term behavioral sentiment which is fragile and has a less than clear mid-term perspective, needs long-term considerations too. Investors are required to contemplate possible dangers that are hiding in open sight and will pose a problem in the future.

The BRICS 2024 Summit was conducted this week in Kazan, Russia. This included the new member nations of Egypt, Ethiopia, Iran and the United Arab Emirates. I am not here to give you a major recap on what took place behind closed doors. I wasn’t invited. But we should look at some of the results and statements made and what they imply strategically.

The BRICS attendees to this year’s conference included powerful dignitaries from approximately 36 nations. One major result of this BRICS conference was to award Partner State status to 13 countries including Algeria, Turkey, Malaysia, Indonesia, Vietnam, Thailand, Nigeria, Uganda, Kazakhstan, Uzbekistan, Belarus, Cuba and Bolivia. Saudi Arabia was invited last year and has not made their full participation official yet, but they attended this year’s conference as an invited guest. The trend appears clear, we are entering a new paradigm in which long-term thinking by the BRICS nations could out maneuver the short-term nonchalance of the West and this has implications for the USD long-term.

There were high level meetings between leaders of BRICS countries including China, India and Russia. Perhaps, more importantly was Vladimir Putin’s bold statement about BRICS desire to start its own grain exchange. Putin also advocated for the creation of a BRICS cartel in other commodities such as metals, including gold. Gemstones such as diamonds and emeralds could develop into a sizeable entity too. This needs to be taken seriously by the West.

Credence must be given because the BRICS nations already are among the largest producers of grains, legumes and oilseeds. The scope of commodity production and supply capabilities by BRICS could certainly turn into a painful thorn in the side of existing large trading companies. And a potentially coordinated energy sector via Iran, Saudi Arabia, Nigeria, Russia and others must be taken into account.

Russia and China as Friends of the Underdogs

Historical entanglements put Western nations like France and others in a vulnerable spot diplomatically as they try to maintain alliances with many BRICS nations. France serves as a good example of diminishing Western influence. France remains on the ground overtly in Africa while dealing with vestiges of a colonial past. But France’s influence in Africa is under stress and their ability to use the continent as a source of power and financial gain is being confronted. France still maintains the Presidential Council for Africa, but France is likely perceived by many of the participants as a wolf dressed in sheep’s clothing. Coups in French influenced African nations have a bloody and present history when political diplomacy does not go well.

Exploiters of the past in many African nations are looked upon with derision and scorn. Russia and China are often viewed as friendly countries who helped fight along the side of certain African nations who sought and achieved independence. The ability to create ascendancy in Africa by Russia and China needs to be looked at within a prism that suggests additional spheres of power will develop in BRICS. Many nations that dealt with colonial statuses in the past are rightfully intent on shaking off the notion of being considered laggards.

The West certainly knows in no uncertain terms it cannot return to colonialism. However, African governments should make sure they are not replacing old masters for new. While some might say it is wishful thinking – and I am still on the fence contemplating the notion – on the part of Russia and China to create powerful commodity cartels, if achieved this actually could prove to be an emphatic first step in attempting to secure a new and powerful currency by backing it with a foundation of intrinsic value. Brazil and South Africa would be a big part of this underpinning too. Russia and China’s foray into Africa via their military and money lending excursions, and the already created organizational and trade structures which exists within BRICS opens the door for the perceived underdogs to battle together against the power of Western riches.

A competition is certainly underway between the West and BRICS. What exactly is the U.S doing in Angola? The planed visit of Joe Biden in the first week of December, which was supposed to take place in mid-October was postponed due to the recent hurricanes. Will the U.S presidential visit be anything more than a sideshow, particularly if the Democrats do not win the election on November the 5th? Angola has a massive amount of Crude Oil and is an OPEC member. American energy companies and other Western corporations are active commercial participants in the African nation. However, China has a firm financial stake in Angola via infrastructure projects too. The political and financial implications between BRICS and the West is a growing dynamic, one that will be further discussed in Part 2.