India Insider: U.S Credit Crunch vs. Indian Banking Paralysis

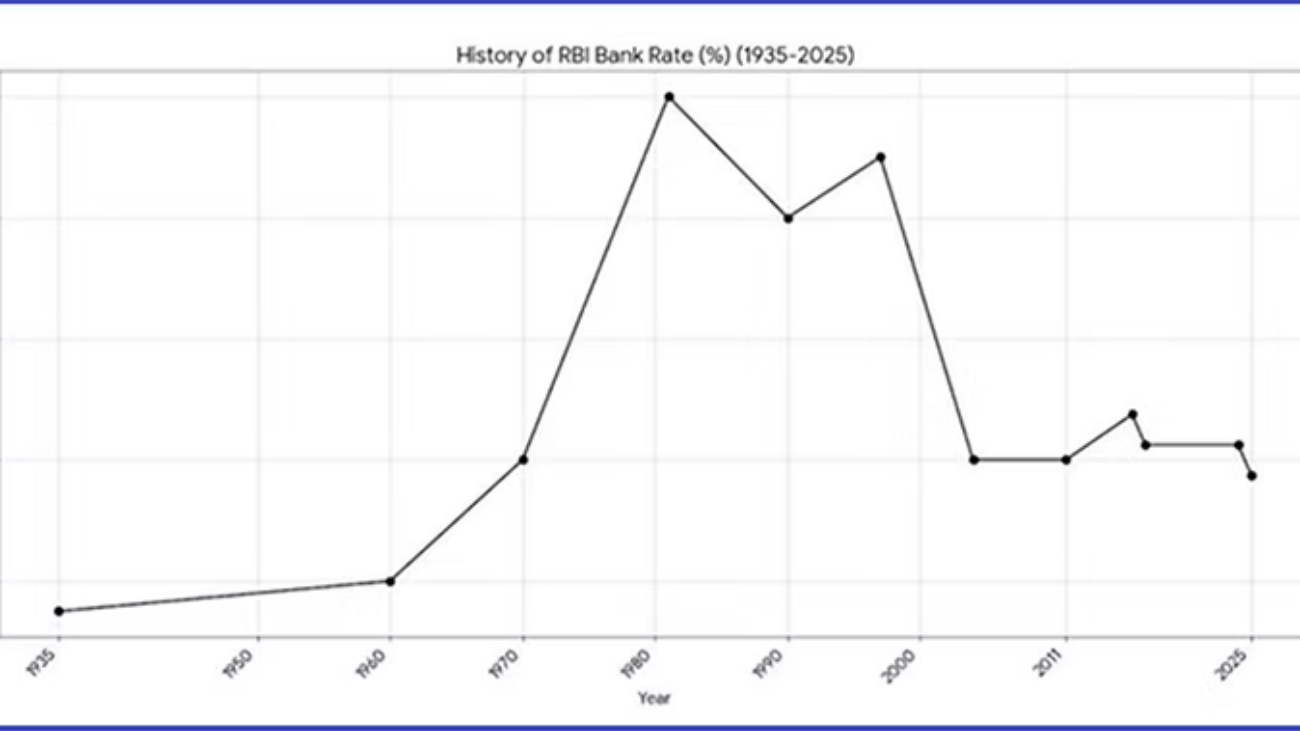

When the U.S suffered a severe credit crunch in the early 1990s, the triggers were clear: the collapse of the leveraged buyout (LBO) boom, commercial real estate price corrections, and the failure of Savings and Loans (S&L) Associations, created the need for a $160 billion taxpayer bailout. Regulators, determined to act tough, declared many banks undercapitalized. The result was a nationwide squeeze from 1991 to 1993, where capital shortages – not liquidity, froze credit markets.

Fed Chairman Alan Greenspan slashed the Federal Funds rate to 3%, but banks couldn’t lend without capital. The unique twist was that, even as lending slowed, competition among borrowers pushed prime lending rates to 6%. This gave banks a fat 3–4% spread. Greenspan let this persist for nearly three years, enabling banks to earn profits equal to more than 10% of assets. With capital requirements at 8%, the windfall repaired balance sheets. By 1994, the U.S had exited the crisis and returned to strong growth.

India’s trajectory was very different. For decades, the country ran structurally high interest rates, which in theory should have allowed banks to recapitalize through spreads, just like the U.S. However, the reality was distorted by governance failures. Public sector banks (PSBs) , which dominate the system did not use their spreads to strengthen capital. Instead, politically connected lending to oligarchs and large industrial houses left the banks saddled with non-performing assets (NPAs).

I witnessed the aftermath up close in 2019 while working at Edelweiss Brokerage. Shadow banks were stressed, some private banks were crumbling, and PSBs were finally forced to acknowledge their bad loans. The selloff in the banking stocks were brutal that year, Catholic Syrian Bank’s IPO, one of the prominent South Indian banks went undersubscribed. To counter the slowdown, the government slashed corporate taxes from 30% to 22% to stimulate capital expenditure.

Unlike the U.S, India’s stress was on the asset side. Corporates were dragged into Insolvency and Bankruptcy Code (IBC) proceedings, where assets were monetized through painful restructurings. Piramal Finance bought DHFL at 30 cents on the dollar, and ArcelorMittal acquired Essar Steel at 90 cents. This was the hard clean up the system had avoided for years.

The NDA (National Democratic Alliance) government made the right call in restructuring the banking sector. Weak public sector banks were merged with stronger ones. Yes, it was costly. Households bore the burden via higher taxes, hidden charges, and high borrowing rates. But at least the problem was confronted.

The contrast is striking. The U.S endured a sharp three-year crunch, recapitalized its banks through spreads and market discipline, and bounced back quickly. India endured nearly a decade of paralysis, requiring taxpayer recapitalizations, corporate asset fire-sales, and systemic restructuring. The eventual stability allowed private sector banks to quietly capture market share from their weaker state-owned peers.

The lesson is simple: interest rate spreads can heal banks only if governance is strong. Without accountability, as India’s PSB saga shows, high rates merely tax households and businesses without fixing the system.