AMT Top Ten Miscellaneous Intrigues for the 17th of May 2024

10. Georgia and Slovakia: It would we wise to pay attention to Tbilisi demonstrations, and also cast an eye on Bratislava after the assassination attempt of Prime Minister Fico. Russia is certainly paying attention.

9. Superconductivity: Origin Quantum Computing Technology of China is making solid advancements and has announced they are ready to domestically produce a 72 qubit capable microwave module known as ‘Origin Wukong’. The battle to create efficient quantum components and operating systems between China, the U.S and others is real.

8. Secretary of Music: Anthony Blinken’s naive decision to play guitar in a Kiev nightclub this week is comparable to Nero playing music while Rome burned. U.S foreign policy continues to raise concerned eyebrows from friends and foes alike.

7. South African Election: The coming vote on the 29th of May is less than two weeks away. USD/ZAR as of this writing is near 18.22000, where will it be on the 30th of May?

6. Biden and Trump: The potential for debates between the two presidential candidates is growing. One question observers may be wondering is if there is adequate supply of caffeine to keep Joe energetic and ample enough hairspray for Donald to look under control?

5. GameStop: Yet another market manipulation of GME is causing massive losses for day traders. The price for the stock finished near $27.67 yesterday, this after touching a high above $56.00 on the 14th of May. GME was close to $10.00 on the 15th of April. Buyers that get in too late to these betting schemes created by frenzied crowds tend to go bust as the early manipulators cash out their profits.

4. Commodities: Cocoa is near 7560.0 USD per metric ton, and Coffee Arabica is traversing slightly below 200.00 USD. Speculative forces remain powerful in both and while they are likely still overpriced, risk management is imperative for those pursuing lower values.

3. Federal Reserve: After the weaker than anticipated CPI numbers printed this Wednesday, and last week’s eroding GDP growth statistics, financial institutions are increasing their risk appetite as they watch U.S Treasury yields decline and consider a mid-term outlook which is allowing for the contemplation of actual Federal Funds Rate cuts.

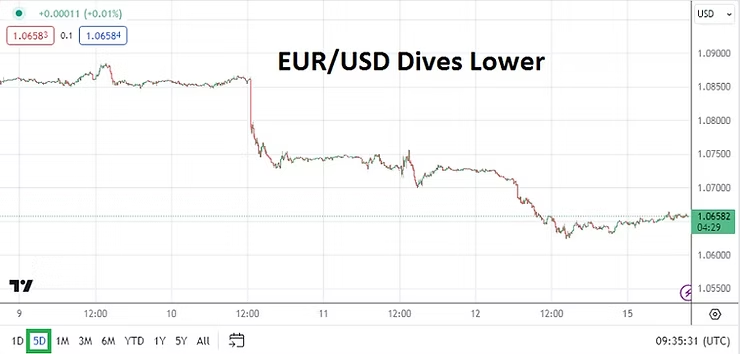

2. Forex: The EUR/USD is back above the 1.08000 level comfortably, and the GBP/USD has found sustainable trading beyond the 1.26000 ratio. While the major currencies versus the USD have pulled back slightly from near-term highs, large commercial traders are exhibiting risk appetite. A weaker USD centric notion is coming into vogue again.

1. Apex Equities: The three major U.S indices are all near record territories as solid earnings reports from corporations, amidst hopes the Federal Reserve will be able to cut rates a couple of times this year has combined to allow optimism to grow in the S&P 500, Dow 30 and Nasdaq 100. While the U.S public is starting to show they are losing confidence because of escalating consumer prices, financial institutions are wagering on solid returns via economic outlooks. Day traders looking to join the indices parade should make sure they limit their exposure, particularly if they are using CFDs and relying on short-term climbs which can suffer from sudden reversals lower.