Forex Calm After the Storm? Volatility and Coming Holidays

The weakness of the USD was anticipated last week, this as the Federal Reserve essentially admitted its aggressive interest rate hikes policy has come to an end. While Fed Chairman Jerome Powell tried to sound neutral, most financial institutions reacted to the FOMC Statement and the Fed’s Press Conference last Wednesday with a rather demonstrative amount of USD selling, largely showing they were prepared to react.

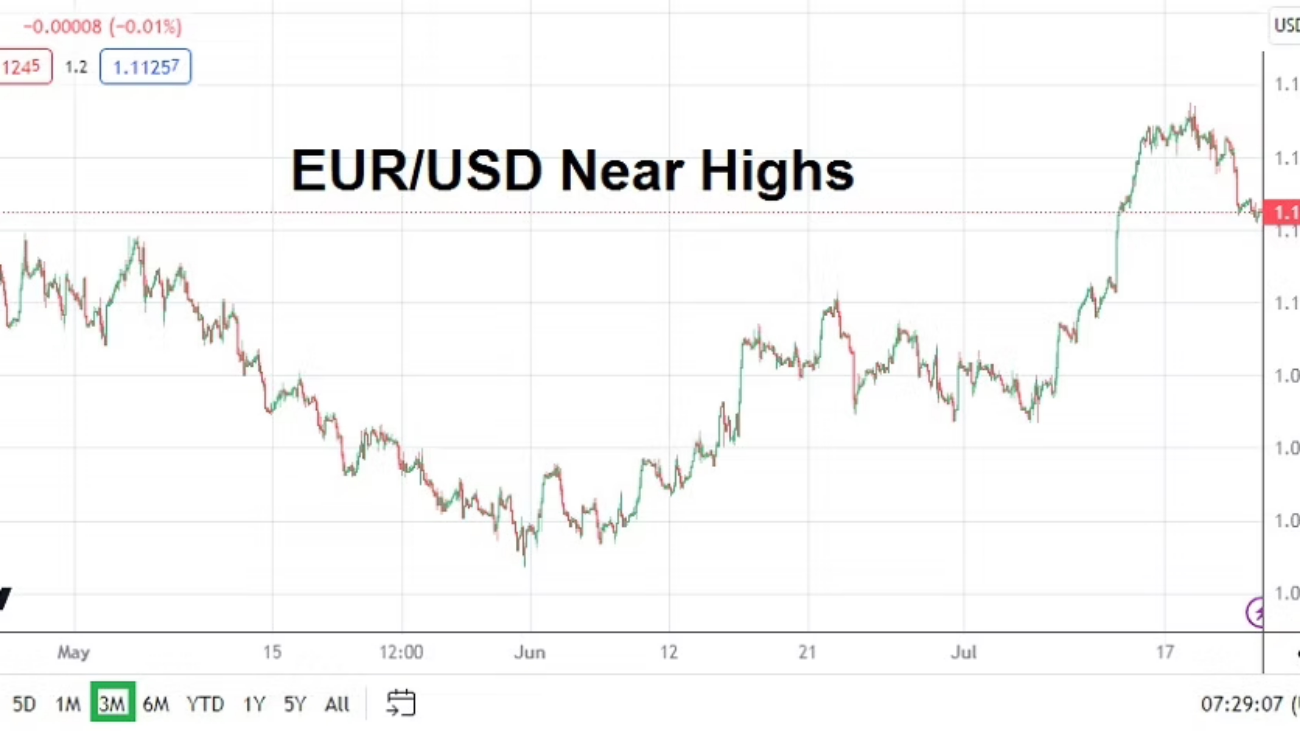

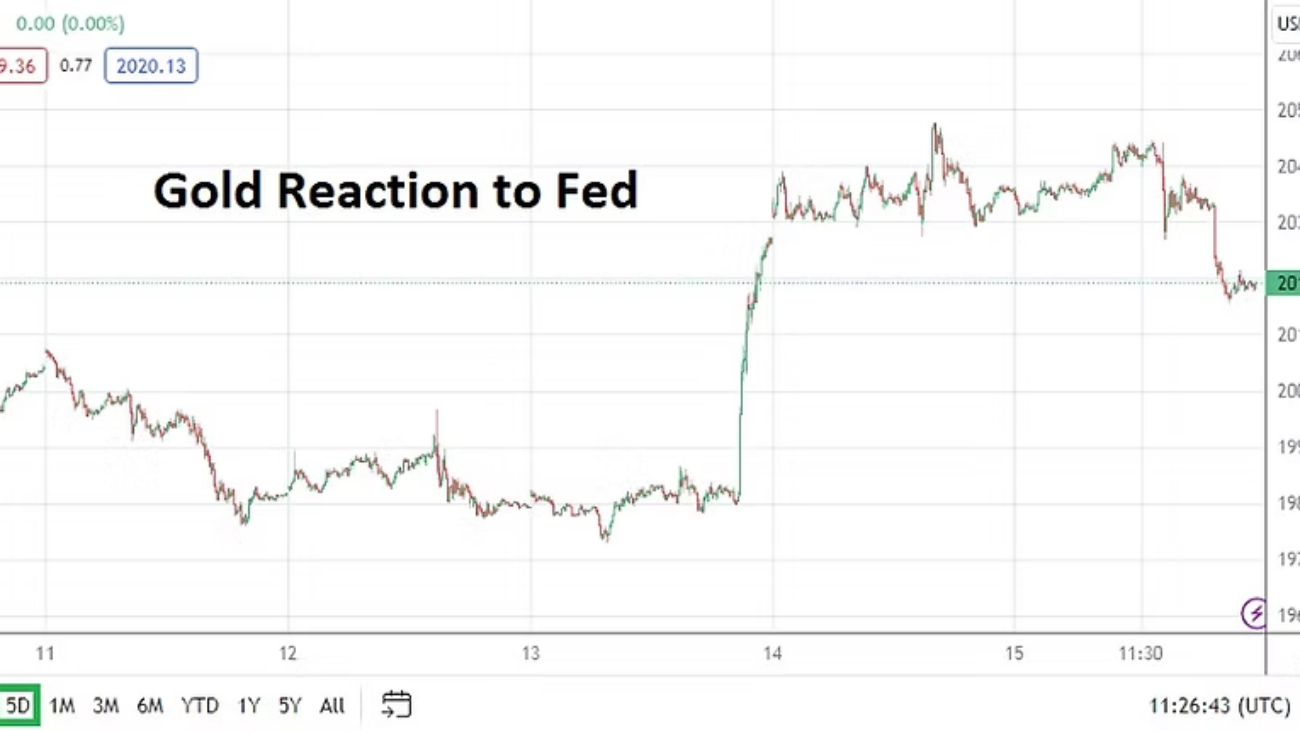

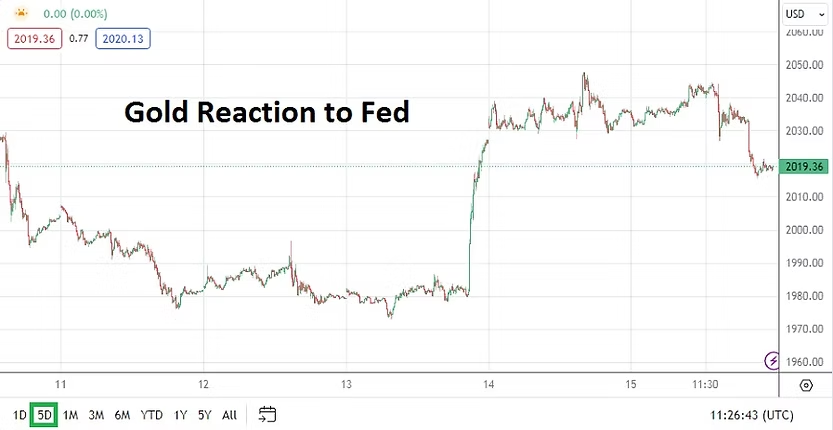

The EUR, GBP and JPY all gained, and many other currencies added value against the greenback too. Gold flourished upwards and even WTI Crude Oil came off its lows. However, after producing strong gains late Wednesday and into Thursday, gold and major Forex pairs did reverse slightly lower on Friday as the USD gained some footing.

Risk appetite likely has enough positive behavioral sentiment influence to continue its desire for dynamic buying on U.S indices. The Dow Jones Industrials will start Monday at record heights, the S&P 500 and Nasdaq Composite are approaching one year highs.

Yes, potential headwinds can develop, so day traders should not bet blindly on bullish gyrations to mount without reversals being expected too. As the GBP and EUR gave back some of their gains on Friday, financial institutions may have been reacting to the notion price velocity higher had been too robust in the near-term. Speculators received another reminder that one way trends tend to meet with reversals that can still cause harm.

Risk adverse traders who have their eyes on global affairs should monitor the situation in the Red and Arabian Seas. Houthi extremists continue to fire at international ships sailing in the areas, and this may generate a reaction at some point from allied navies which are supposed to protect vessels and commerce. If the U.S Navy reacts to the Houthis in a strong manner this could deliver a cold short-term shiver into markets.

Speculators also need to understand this is the last ‘full’ week of trading before the Christmas and New Year holidays, which can cause a massive decline in volumes. This Thursday’s trading will begin to decrease from norms, and Friday’s price action will likely be affected by offices around the world starting to shutter as employees disappear for extended vacations. Day traders who want to participate in Forex, commodities, and equities via CFDs should be prepared for the emergence of quiet markets the end of this week with occasional volatility disrupting technical charts.

However, this Monday and Tuesday will pose questions regarding possible reactions to the weaker USD which has emerged, and U.S equity indices showing signs of speculative zeal. U.S Treasury yields continued to trend lower last week, and U.S bonds should be watched early to see if market participants continue their optimistic paces, or show signs of becoming more passive as the holidays approach. Traders with strong convictions regarding directions may feel inclined to remain active throughout this week and cannot be blamed, but some caution should be practiced.

Monday, 18th of December, Germany ifo Business Climate – the reading is expected to show a slight improvement over the last month. EUR/USD traders may believe they should react to the results from this report, but the EUR is likely to stay within a USD centric mode driven by existing outlooks. The ability of the EUR/USD to hit the 1.10000 level late last week confirmed positive mid-term bullish outlook. The reversal lower on Friday may ignite speculative buying positions early this week, but day-traders may want to be conservative.

Tuesday, 19th of December, Bank of Japan Monetary Policy Statement and Press Conference – the BoJ is not expected to raise their interest rates quite yet. However the end of the BoJ’s negative monetary policy may be coming to an end in 2024. The BoJ bet on the notion that inflation would come down eventually, even it maintained a negative interest rate policy – this seems to have been proven correct. The USD/JPY has reacted the past month with a rather incremental decline. Perhaps Japanese financial institutions have been positioning for a stronger JPY over the mid-term. The USD/JPY trajectory lower remains intriguing for speculators.

Wednesday, 20th of December, U.K Consumer Price Index – the BoE sounded more dovish than many folks expected they would this past Thursday. Inflation numbers coming this week should be watched. The British economy remains lackluster, but sounds about ‘weaker’ inflation have been heard. The data from the CPI is expected to be slightly lower than the previous month. The GBP/USD could react to this report. The British Pound has delivered upwards momentum since late October. Traders should be careful regarding potential short-term reactions from the GBP/USD, and understand Forex volumes may start to decrease on Thursday and Friday which could affect results.

Thursday, 21st of December, U.S Final Gross Domestic Product – growth in the U.S has been better than most anticipated. While many analysts are still predicting a slowdown, the GDP number is expected to show a 5.2% gain. The inflation report via the GDP Price Index is anticipated to be 3.6%. While the broad markets typically would react to these statistics in a strong fashion, trading might be somewhat muted as financial institutions begin to focus more on the coming holidays.

Friday, 22nd of December, Canada GDP – a slight gain of 0.2% is expected regarding the growth statistics. Markets will be quiet and while the USD/CAD could see a momentary increase in trading, behavioral sentiment from earlier this week will likely have had a bigger effect.