To Risk or Not to Risk that is the Speculative Question

Last week U.S equity indices demonstrated a rise in value. The highs achieved in the Dow Jones Industrial Average, the NASDAQ Composite and the S&P 500 by the end of last week only touched values seen in the middle of October. And while their ratios remain below the highs of early August and falling values seen in September, the move upwards was certainly welcome by financial institutions and day traders who hold optimistic viewpoints.

U.S Treasury yields declined last week. While incremental decreases were made through Thursday, the U.S Non-Farm Employment Change and Average Hourly Earnings reports both coming in below expectations on Friday, created a stronger dose of lower yields. The 5, 7, 10 and 30 year U.S Treasuries are now trading near mid-September values. The 2 and 3 year notes are moving around early September numbers.

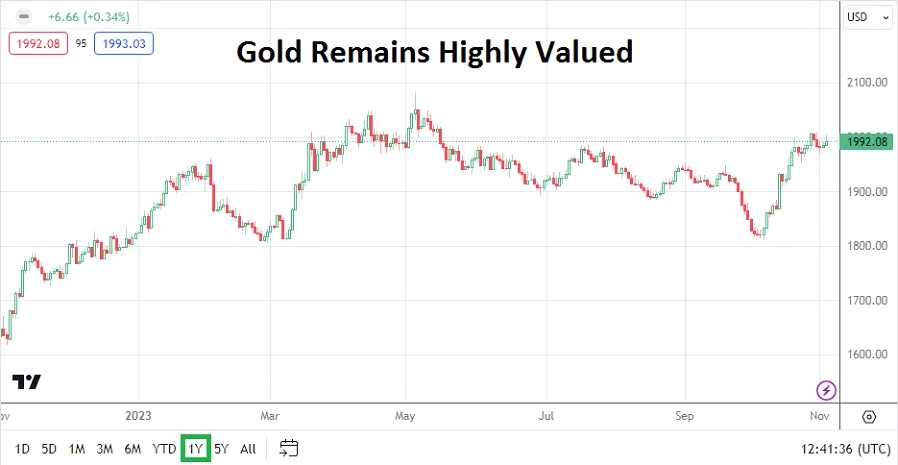

The USD grew weaker in slight movements against many major currencies last week, but upon the weaker jobs numbers found increased selling price velocity. Gold however remains suspiciously strong, which brings up the notion that risk adverse ‘insurance’ is still being held closely by investors who remain nervous.

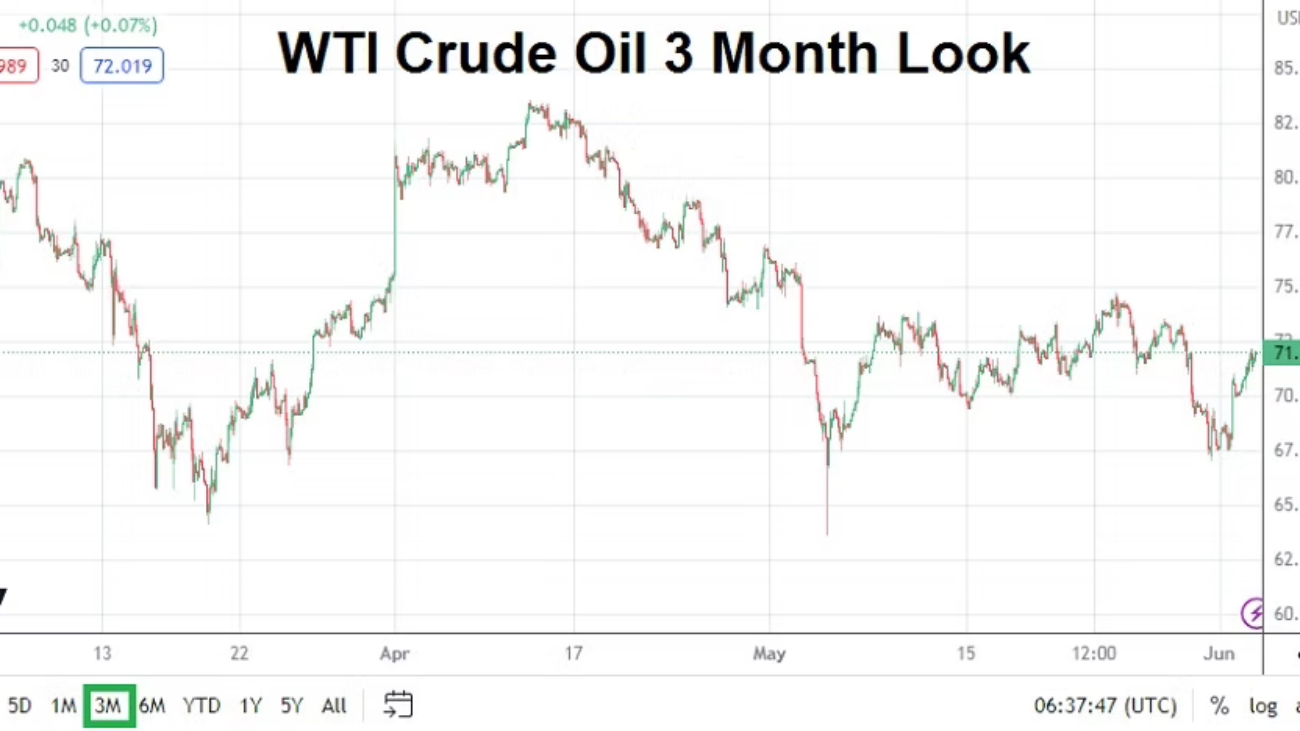

The Middle East crisis is ongoing in Israel against Hamas and to a limited extent Hezbullah, but financial institutions have seemingly been able to digest the news and remain tranquil and vigilant. Another sign of calm coming into the global financial markets is the price of WTI Crude Oil which finished the week under 81.00 USD per barrel.

Economic data will be relatively light this coming week, and behavioral sentiment appears to be the potential larger factor until Friday regarding impetus for day traders and financial houses. Certainly loud global developing news could suddenly erupt and cause nervous investors to falter, but last week’s trading results showed signs of improving risk appetite.

The U.S Federal Reserve met expectations last Wednesday and didn’t raise the cost of borrowing. The mid-term seems to indicate interest rates will remain high, but that the U.S central bank will not raise the Federal Funds Rate anytime soon. The lower than expected inflation report via the Average Hourly Earnings before going into the weekend helped highlight this thinking, although it remains a consideration that is still speculative.

Officials from the major central banks including the BoJ, BoE and Fed will be speaking this week and could cause turbulence with their rhetoric. However, no major surprises will likely come from their mouths. Although the Bank of Japan may rattle the prospects of intervention to keep USD/JPY traders on their toes.

Monday, the 6th of November, Germany Factory Orders – the result is expected to be negative and highlight the nation remains within recessionary conditions. The Sentix Investor Confidence reading will also be released slightly afterwards for the European Union and a worse number than last month’s outcome is anticipated. But the EUR/USD is likely to remain mostly USD centric, even though these reports could cause momentary fluctuations.

Tuesday, the 7th of November, Australia Cash Rate – the Reserve Bank of Australia is expected to raise its interest rate by 0.25% to 4.35%. Will the RBA take a gamble and not raise the interest rate due to other major central banks holding their rates in place, or will the increase go ahead to fight stubborn inflation while trying inspire some confidence in the AUD? A hike seems to be the direction the RBA will decide upon, having said that, the Australian central bank have surprised financial institutions before.

Wednesday, the 8th of November, U.S 10-year Bond Auction – the results from this sale and the yields that develop within U.S Treasuries will have an affect on Forex. Lower yields than anticipated could signal a weaker USD. However, risk adverse elements will need to be calm for the bond auction to produce tranquil results.

Thursday, the 9th of November, China CPI and PPI – the data from these inflation reports will be watched closely. Chinese economic numbers has shown some signs of stabilization the past few weeks, both of these publications are expected to have negative outcomes. Concerns about the financial pressures domestic consumers are facing regarding housing market values in China and the way in which they spend due to lackluster prospects are concerning. The USD/CNY will be affected in the wake of these statistics, and the USD/SGD could see momentary volatility too if the results prove to be a surprise.

Friday, the 10th of November, U.K Gross Domestic Product – last month’s number came in with an unexpected positive gain of 0.2%, this GDP report is anticipated to show no change. The GBP/USD jumped in value on Friday and financial institutions will be geared towards behavioral sentiment most of this week, but the British GDP data could cause a reaction before going into the weekend.

Friday, the 10th of November, U.S Preliminary Consumer Sentiment via the University of Michigan – the reading is expected to be slightly below last month’s outcome. U.S consumers remain a strong point of light for the U.S Federal Reserve. American consumers have remained spenders, although they have seemingly curtailed purchases of large ticket items such as cars and big appliances. If this data comes in weaker than expected it could propel more selling of the USD. A stronger number than anticipated could spook financial institutions and cause a slight surge in buying of the USD.