Inflation Data and Fed's FOMC Meeting Minutes This Week

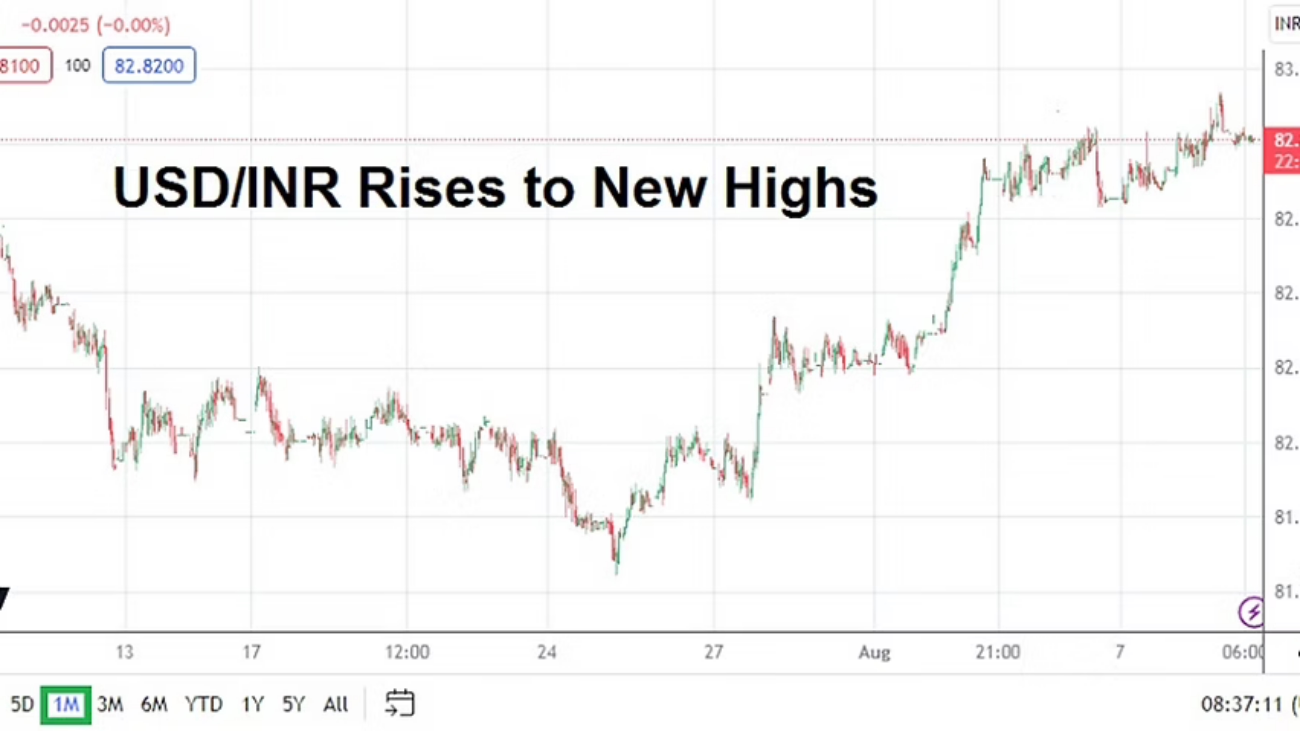

Last week’s economic data ended with rather tantalizing headline jobs numbers as the U.S showed more hiring than expected, but while this grabbed media soundbites in many circles – the Average Hourly Earnings numbers came in below expectations. The broad Forex market proved dynamic with a stronger USD in many cases, but intriguingly equity markets in the States generated upwards momentum on Friday too. U.S Treasuries were mixed regarding their yields, and the 10-year bond while finishing up for the week was below its highs.

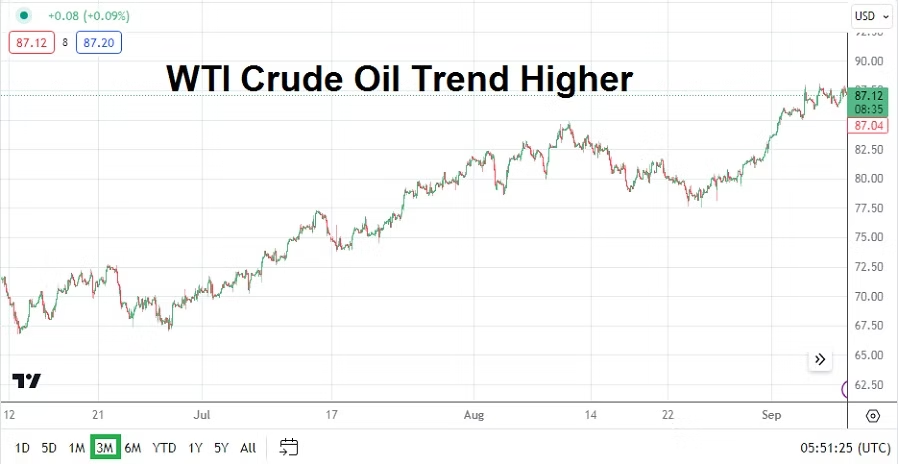

The coming week will likely continue to produce nervousness, but outlook will be helped via a couple of U.S inflation reports and the FOMC Meeting Minutes report. Crude Oil prices should be watched as news from the Middle East unfolds. Gold remains under pressure.

Cryptocurrency speculators should keep their eyes on Binance Coin as it battles important lows. Bitcoin has remained relatively stable, but BNB/USD is near crucial support that could signal another wave of pressure is developing within the Binance exchange.

Monday, the 9th of October, International Monetary Fund – week-long meetings get underway and investors who participate in global stock markets and bonds should pay attention to the chatter.

Tuesday, the 10th of October, Central Bank Officials speaking – ECB President Lagarde will be speaking at the IMF conference. Federal Reserve officials will be speaking at meetings in the U.S. While the chatter may cause some nervous reactions briefly in financial institutions, it is unlikely the central bankers will say anything that is surprising.

Wednesday, the 11th of October, U.S Producer Price Index – the broad and core reports should be watched. Last week’s lower Average Hourly Earnings numbers were slightly surprising, but the recent higher energy costs could factor into the PPI results. The broad report is anticipated to show a decline. If the Producer Price Index statistics come in weaker than expected this could help the USD lose some strength.

Wednesday, the 11th of October, U.S FOMC Meeting Minutes – the publication is expected to follow the rhetoric already voiced by the Fed at their last press conference. However, insights regarding dialogue could move the needle in Forex. The U.S central bank is widely expected to raise the Federal Funds Rate in November, but what comes beyond this anticipated move is still in question. Expect the key word in the FOMC report to be ‘inflation’.

Thursday, the 12th of October, U.K Gross Domestic Product – the growth numbers from Great Britain are expected to show a slight rise in GDP. If the gains match expectations or come in better it could help bolster the GBP/USD which has been struggling against the USD for the past three months.

Thursday, the 12th of October, U.S Consumer Price Index – these reports will be crucial and will impact Forex and equities immediately after their release. While the Core CPI number is expected to match last month’s outcome, the broad reports are anticipated to be weaker. If the inflation numbers are stronger than expected the USD could gain strength, if the results are weaker it could help build selling momentum in the USD.

Friday, the 13th of October, China Consumer and Producer Price Index – the two releases will be watched carefully by investors. China’s economic data has been weak and financial institutions have become concerned by deflation. The USD/CNY may be impacted upon the publication of the reports.

Friday, the 13th of October, U.S Consumer Sentiment via the University of Michigan – following the CPI numbers from the U.S on Thursday, these numbers will show the attitude of U.S consumers and their spending habits. Financial institutions will monitor these numbers and correlate them to the U.S inflation reports seen earlier.