Things Unlikely To Get Easier for Retail Speculators Remainder of Week

I would like to offer day traders encouragement under the current market circumstances. However, the reality is that the next handful of days will remain difficult for retail traders who do not have comfortable amounts of cash to absorb when intraday chaos occurs. On the other hand as an ex-risk manager for a brokerage house, I can state that CFD providers are singing joyfully because they are making profits from the wild fluctuations in equity indices, Forex and commodities.

Gasoline and Burning Cash Continues

A case in point are the results via the future markets, this via CFD offerings by brokers’ platforms yesterday for the S&P 500 and Nasdaq 100. Early nervousness saw an electric amount of selling get demonstrated and then suddenly a reversal higher, this as President Trump caused a thunderous optimistic reaction as he spoke about the potential of a deal with Iran in the coming days. The dose of optimistic risk taking lasted a couple of hours.

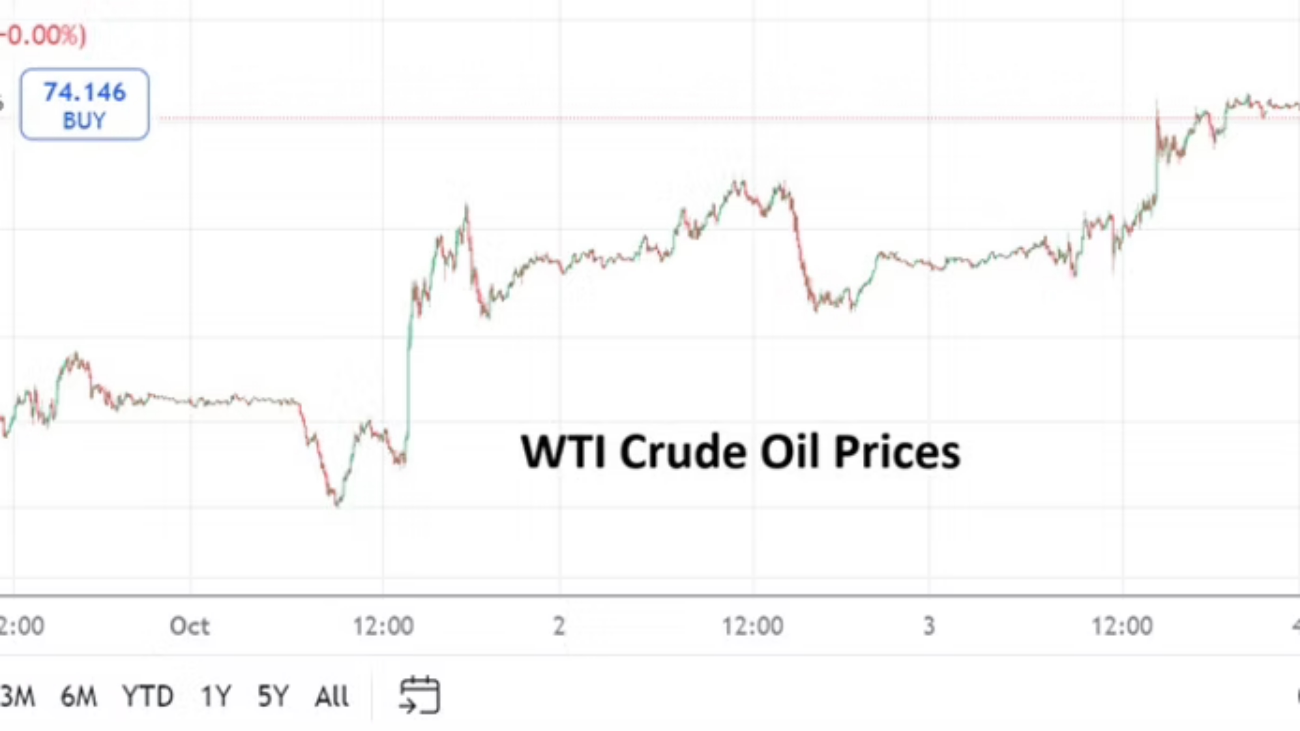

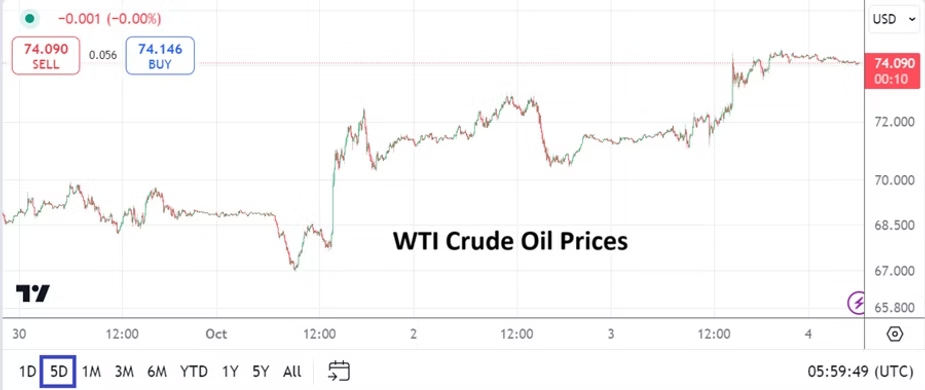

Not only did U.S equity indices bolt higher, but WTI Crude Oil prices slid lower, and Forex suddenly saw the USD losing strength. Here’s the thing, some day traders certainly made money as waves of momentum carried their wagers into positive terrain, but many speculators were likely knocked out of the their trades with sudden loses. CFD trading using leverage has always been a casino, this is not going to change. But the volatility seen the past three weeks has likely not created great wealth for retail traders. Some have gained certainly, but I can guarantee you brokers are making more money via the intraday swings and volatility that knock smaller traders out, this as leverage causes fluctuations that expose too much risk and cause folks to lose money.

Again, this is the nature of the beast. Day traders wanting to participate in the markets have to acknowledge the risks that will confront them. It is a warning worth noting once again as a war rages in the Middle East.

Markets in the best of times are difficult. Risk management is constantly needed. While the thrill of trading is fantastic, without solid tactics speculating equates into gambling. Think of brokers as bookies, they gear the market via wide spreads, transaction fees including overnight charges to favor themselves. Brokers are certainly glad to pay out winners so others are enticed and bring more business, but strategic day traders who use well practiced methodology are watched closely by brokers – because these folks (good traders who are careful) are a threat for brokers bottom lines – profits are king.

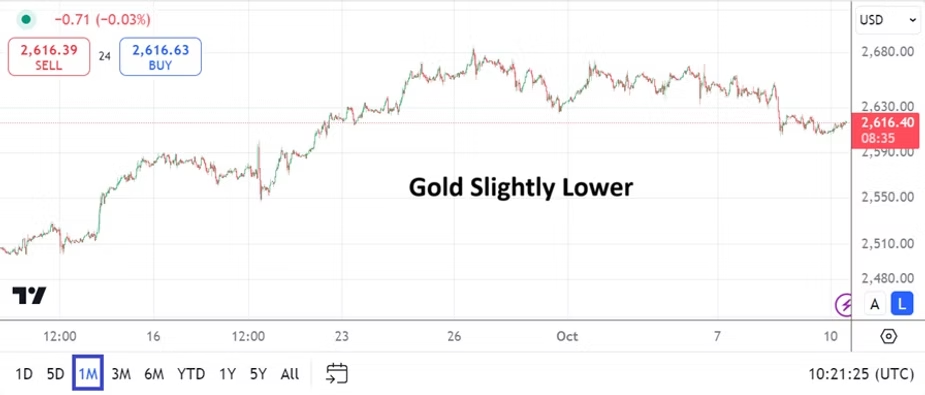

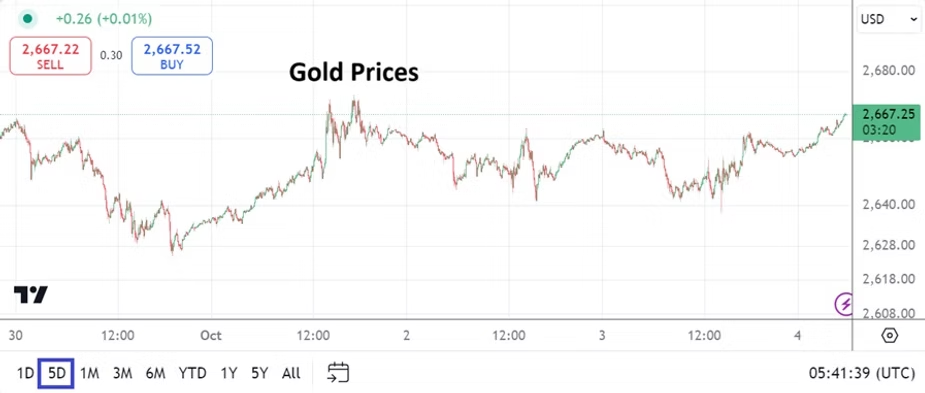

Trading and fundamental notions are proving dangerous too during these loud times. Gold for instance which was trading at all-time highs in January (along with silver – but that is another speculative story) is now traversing near $4,425.00. The precious metal was testing the $5,600.00 vicinity in late January. So how did this long heralded safe haven metal actually see a selloff become stronger since the start of the Iranian war when it was around $5,200.00 on the 27th of February?

IMO, it shows that speculative fervor in gold was fever pitched in January, and even though a war has broken out and caused widespread anxiety in the broad markets (which in theory is supposed to make gold more valuable), the volatile nature of wagering – yes gambling – on the markets including gold, often is a crapshoot. Folks who bought gold as a speculative endeavor have now cashed out their profits, those who believe gold is a safe haven and are buying based on this belief will need another round of speculative fuel to induce significant gains like those made in January. The market sometimes runs out of participants when things get too cautious. In other words, if there are not enough buyers, selling momentum takes over.

And to put a finishing touch on this piece, let there be no doubt that brokers were likely relieved that the one way avenue upwards for gold (and silver) seen into January has now turned into a volatile betting battle. The point here, if I am able to make one is this, market conditions are rough and will remain extreme in the coming days. Folks need to be cautious, the markets are not your friend, they are a tool for making money (or losing it).