10. Three P’s: Pragmatic and populist politicians are clashing in a world that seeks to try and sell utopian visions from all sides, instead of admitting realities that should be understood and defined, thus creating a more dangerous world. It would be funny if it weren’t so serious.

9. Investment: Pasqal, a quantum tech company located in France founded in 2019, and IBM have announced a collaboration to integrate efforts on creating quantum centric supercomputing architecture. The quest for fully functioning applications appears to be years away as theories such as neutral atoms are studied and applied, and cooling systems are pressed to their limits. However, a transition into working research continues to build momentum. Accelerated investment paths for those seeking the quantum golden goose are flourishing.

8. Three C’s: Cocoa, Coffee and Copper are creating speculative storms for traders as volatility has seen apex values, then dramatic drops, followed by violent reversals higher in the commodities. Cocoa is back above 10,100 USD per metric ton as of this writing, and Coffee Arabica and Copper have been delivering huge profits and staggering losses for large players and day traders who continue to wager.

7. India: Narendra Modi has retained power after a hard fought voting outcome has diminished some of his power. However, fears that turned the Nifty 50 index sharply lower earlier this week, also created a market discount for long-term investors. Foreign investors continue to have a positive economic outlook for the nation. It will not be a surprise to see the Nifty 50 back to pre-election levels and challenging record highs soon, yet again delivering a lesson for day traders who are speculating on the short-term instead of being patient.

6. South Africa: Coalition government discussions are ongoing and will grow in noise in the coming days as a deadline to conclude an agreement approaches. The ANC is said to be talking seriously with the Democratic Alliance, but the Congress of South African Trade Unions which is strongly aligned with the ANC is against the move. It has recently been reported that South Africa’s ports are among the least dependable in the world by the Container Port Performance Index. Poor infrastructure, corruption and a lack of transparency are hurting South Africa. The ANC decision in the coming week regarding a coalition is vitally important. Either it will decide to make concessions and bring the DA in as a working government partner and hopefully build a bridge towards a better South Africa, or the ANC will decide on a hard-left coalition which could potentially bring it to a Venezuela or Zimbabwe type of outcome. The USD/ZAR will react.

5. Conservatives: The U.K election is less than one month a way, and Labour appears set to take power and control Parliament with a large majority. The failure of the Tories to create the perception of successful economic, foreign, and social polices that resonated with the public, appears to be easing the way for a ruling Labour government which has not been seen since since 2010.

4. Carry Trade: The EUR/USD will become an interesting test ground for carry trade fundamentals in the coming weeks and months. The ECB cut its Main Refinancing Rate as anticipated yesterday by 0.25%, but said it is neutral about more cuts. The ECB explained it was able to cut interest rates yesterday, because current inflation levels have dropped enough that a modification of interest rates was needed, but that it remains cautious about inflation in the future. This statement and policy could potentially allow for the Federal Reserve to become the more dovish central bank over the mid-term and lead to a stronger EUR/USD. How much will financial institutions wager on this notion in the near-term?

3. USD/JPY: Serenity now should be the new mantra for the BoJ. The Bank of Japan seems to be waiting on the Fed to sound more dovish, which could stop the need for the BoJ to intervene again. The USD/JPY remains high and is currently testing the 155.000 to 156.000 range in a fairly steady manner. The Bank of Japan will release its Monetary Policy Statement on the 14th of June. While Forex tranquility has been demonstrated the past couple of days, conditions may change rapidly later today and day traders should brace for price velocity.

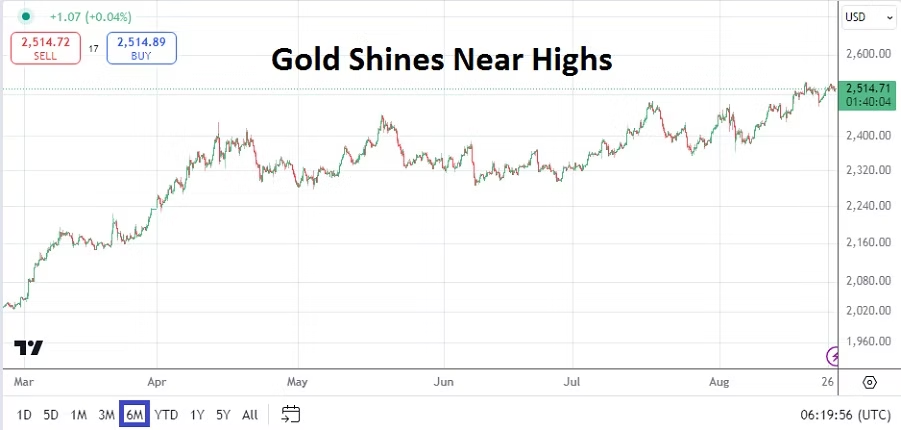

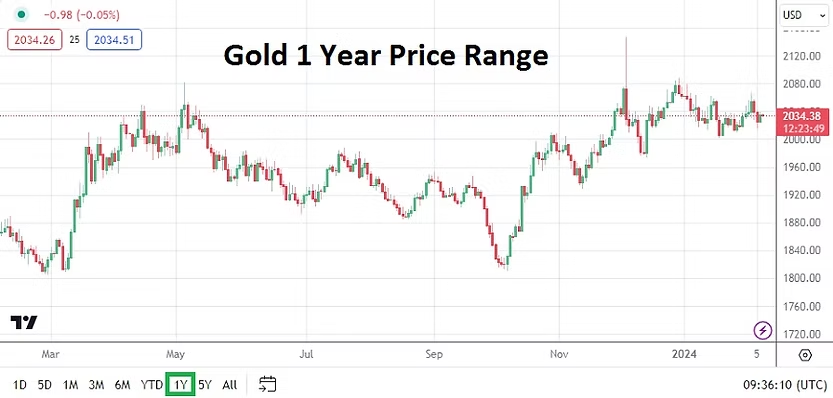

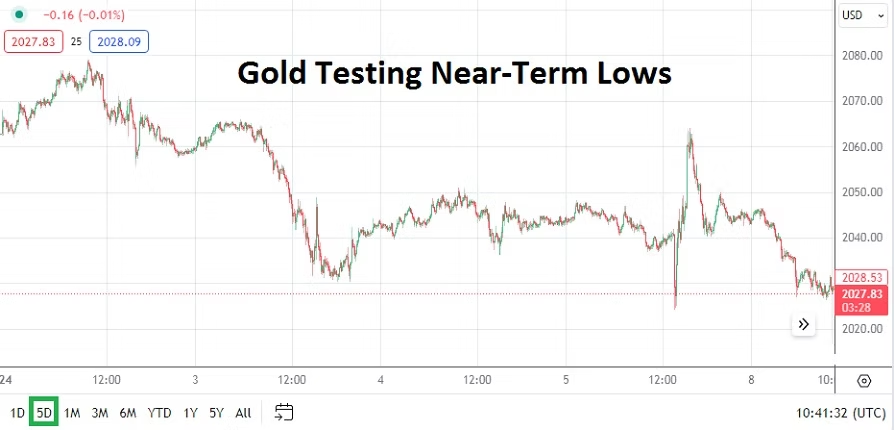

2. U.S Indices: Equity values have recovered in the Nasdaq and S&P indices, and while the Dow 30 is below apex highs it is still within sight of the 40,000 level touched on the 20th of May. Treasury yields have traded slightly lower this week which has ignited risk appetite again. Gold is trading below the 2,400.00 USD ratio, but still comfortably above 2,300.00 for the moment. If Treasury yields continue to experience a downturn, institutional investors are likely to funnel cash into the stock market.

1. Data: U.S jobs numbers via the Non-Farm Employment Change and Average Hourly Earnings figures will be published today. The result will certainly set the path for the Federal Reserve’s June 12th FOMC meeting. Yesterday’s weekly Unemployment Claims came in weaker (more claims filed) than expected and other jobs data was weaker the past few days via JOLTS and the ADP statistics. All financial assets will react to the U.S data today. Weaker jobs numbers would create more confidence among institutional investors that the Fed will have to sound dovish rhetoric regarding potential cuts to the Federal Funds Rate in the coming months. Fast trading conditions are coming today.