A Case for Higher Interest Rates In India

As the Rupee remains under pressure and oil prices continue to rise amid tensions in the Middle East, the debate has shifted towards what the Reserve Bank of India (RBI) should do next.

Economist Janak Raj has argued that raising interest rates to defend the Rupee comes with significant costs. Higher rates increase the cost of capital for businesses, reduce investment activity, and compress equity valuations. In theory, this could even accelerate foreign outflows from equities rather than attract fresh capital. Yet the RBI may soon find itself with limited options.

USD/INR One Year Chart as of 11th of June 2026

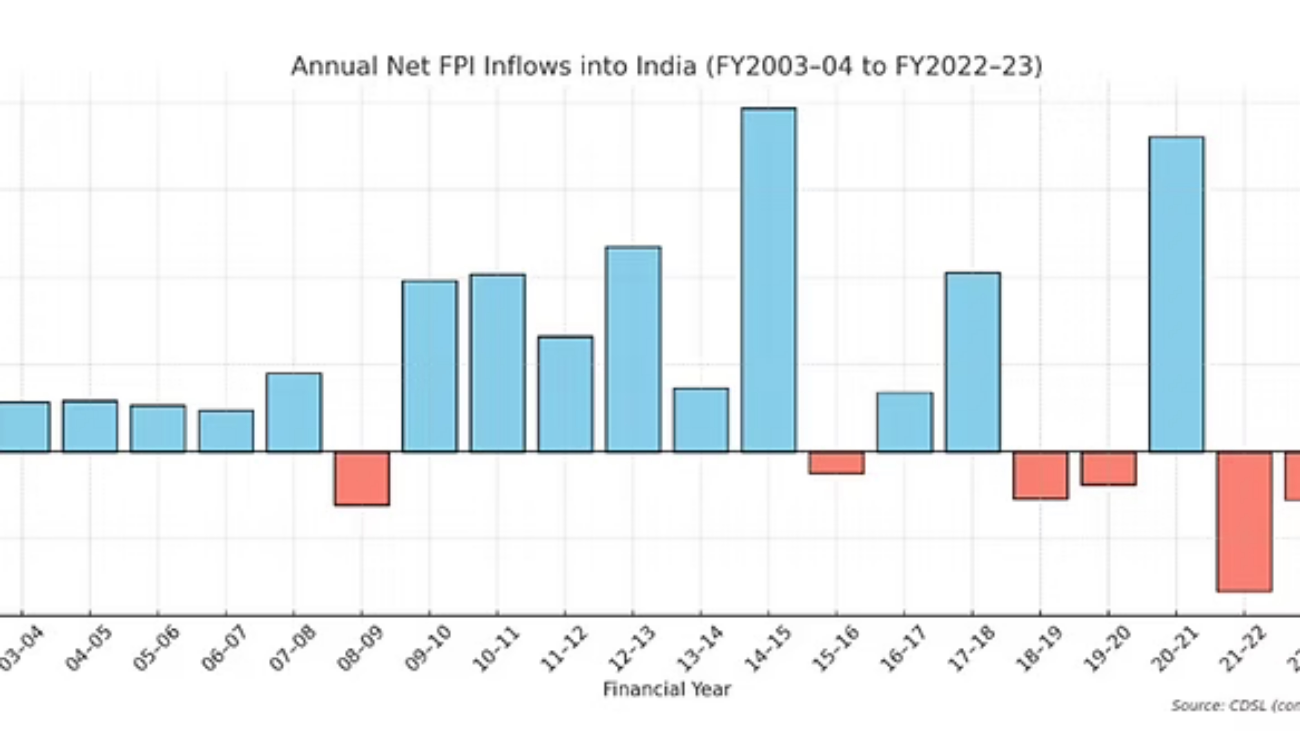

Foreign Portfolio Investors (FPIs) were net buyers of Indian equities for most of the period between 2004 and 2024, with only a few exceptions such as 2011, 2018 and 2022. However, the trend has changed. FPIs sold approximately $19 billion USD worth of Indian equities in 2025 and another $24 billion USD so far in 2026.

Question: Why are Foreign Investors Selling

One reason is that global investors today have alternatives. The growth of Artificial Intelligence related companies in the United States has created significant investment opportunities. At the same time, U.S Treasury yields hovering around 4.6% offer attractive risk-free returns in a strengthening dollar environment.

For many global investors, earning high returns in Dollar assets is preferable to taking exposure in emerging markets that face current account pressures from rising Crude Oil prices and other energy costs.

Taxation is another factor. India taxes foreign investors at 20% on short-term capital gains and 12.5% on long-term gains. Meanwhile, competing financial centres such as Singapore, Hong Kong, Malaysia and Thailand generally do not tax foreign investors’ capital gains.

Some global funds have argued that India should move closer to international norms, where capital gains are usually taxed in the investor’s home jurisdiction rather than the country where the investment is made. Higher post-tax returns would undoubtedly make Indian assets more attractive.

A stable Rupee would also reduce hedging costs, lower currency-risk premiums and improve the overall risk-reward profile for overseas investors. However, tax cuts alone cannot solve India’s problem.

The Real Issue is Balance of Payments

As Business Line columnist Lokeshwari Mam has pointed out, a significant portion of equity outflows consists of short-term speculative capital. Long-term capital tends to remain invested. This is why the decline in net Foreign Direct Investment (FDI) should concern policymakers more than short-term fluctuations in portfolio flows.

Net FDI has fallen sharply from $28 billion in FY 2022-23 to just $7.7 billion in the year ended March 2026. This is a worrying trend because FDI is the most stable source of external financing. Unlike portfolio flows, it creates factories, jobs, exports and long-term productive capacity.

India therefore needs more than tax incentives. A genuine single window clearance system, reduced bureaucracy, easier business regulations and reforms in manufacturing remain essential. Attracting long-term capital should be a national priority.

The recent foreign buying of Indian bonds after tax cuts is encouraging. But relative to India’s current account financing requirements, it remains a small drop in the ocean.

For example, in FY 2025, the current account deficit was 0.6% of GDP. And in Q4, the current account became a surplus. Is it really that difficult to finance it’s small current account deficit?

India’s external vulnerability is determined not merely by a current account deficit, but by whether the capital account can be comfortably financed. A modest current account deficit still creates currency pressure if foreign capital inflows weaken (which we are seeing), while a larger deficit may be sustainable when capital inflows remain strong. The risk of sustained higher oil prices could widen the deficit, increasing India’s dependence on foreign capital at a time when global liquidity is tightening and U.S Treasury yields are rising.

Furthermore, hedging costs continue to erode much of the yield advantage that Indian bonds offer over U.S Treasuries. In that sense, active global money is likely to prefer Dollar assets over emerging-market debt or equities

India’s repo rate currently stands at 5.25%. The RBI’s decision to raise its inflation forecast to 5.1%, while lowering its GDP growth projection to 6.6% reveals where the shock from the Iran conflict is likely to be felt via higher inflation and weaker growth. For an economy that remains heavily dependent on imported oil, a depreciating Rupee only compounds the problem by increasing the cost of energy imports.

In such an environment, the Monetary Policy Committee is unlikely to focus solely on growth. Currency stability, inflation expectations and the availability of foreign capital to finance India’s external requirements could become increasingly important considerations. If these pressures persist, the RBI should raise the repo rate, in the same manner other Asian central banks have done in recent weeks.