Cautious Trading as Key Data and Outlooks Await Impetus

The start of trading this week could prove to be slightly adventurous for speculators as financial institutions return to the markets and start to take positions for their clients. Having survived the past two and a half weeks of holiday season trading, market action will now focus on immediate, mid and long-term goals and outlooks depending on time frames and targets. Slightly nervous trading was on display last week, but some traders may believe their is plenty of room for more optimism and may be suspicious of the results delivered.

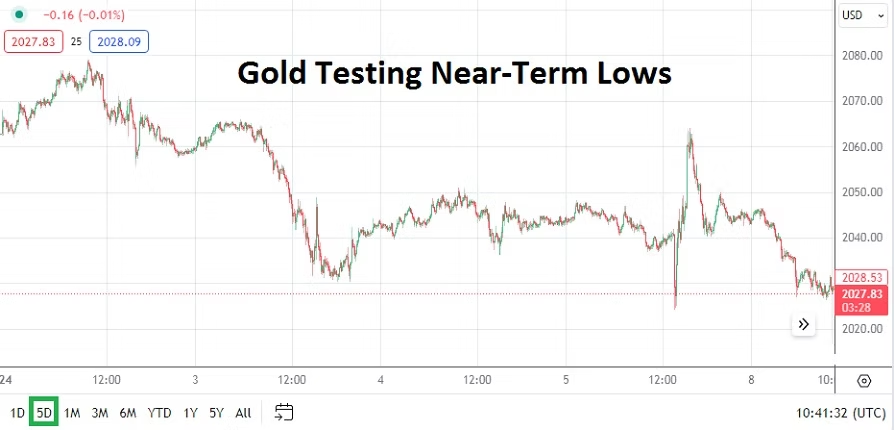

Day traders should look at some barometers before they participate in the near-term. Gold has come off highs seen late last week, but remains within the higher elements of its six month price range. Its selloff from apex values last week perhaps correlates to U.S equities and USD turbulence which has also been experienced.

Last Friday’s reaction to the U.S jobs numbers was fascinating. The numbers delivered an initial shock to folks who wanted to react quickly. Hiring the last month increased more than expected, which might have caused the momentary bullish surge in the USD. Only to be confronted swiftly by further investigation of the jobs data which showed previous months statistics had been revised downwards. This acknowledgement set off selling of the USD and technical whipsaw results.

Day traders participating in Forex this past Friday likely experienced a range of emotions. If the market correlations are correct regarding the USD and the reactions seen, trading in gold also seemed to mirror the price action. Interestingly, gold touched a low of nearly 2024.00 USD on Friday in the wake of the jobs report, surged higher to around 2064.00 and then reversed lower again.

The notion that gold is trading within sight of Friday’s lows is interesting for both the precious metal and trying to understand where USD sentiment will lean early this week.

Behavioral sentiment remains rather optimistic, however nervous headlines during the holiday season may have caused cautious shadows to grow darker, particularly as light trading volumes affected results. Today and tomorrow will prove interesting in the broad markets, this as financial institutions return in full and as they brace for U.S inflation numbers later this week.

Nervous short term trading is likely today and tomorrow as price equilibrium is sought. U.S equity indices have backed away slightly from their flirtations with all-time highs, but even as selling developed the past week highs are still in sight and are likely still being dreamed about by many institutions. U.S Treasury yields will also be a good indicator for Forex traders early this week regarding how comfortable financial institutions are with their current outlooks.

Monday, 8th of January, Germany Factory Orders – a slight gain of 0.3% was reported today, which was below the 1.1% expectation. The German economy is starting to show signs of economic growth, but has major hurdles to still climb. The lackluster German numbers may keep the ECB in a rather neutral stance for the mid-term. Which might help a bullish EUR/USD outlook if the U.S Fed is seen as the first major central bank which will have to cut interest rates.

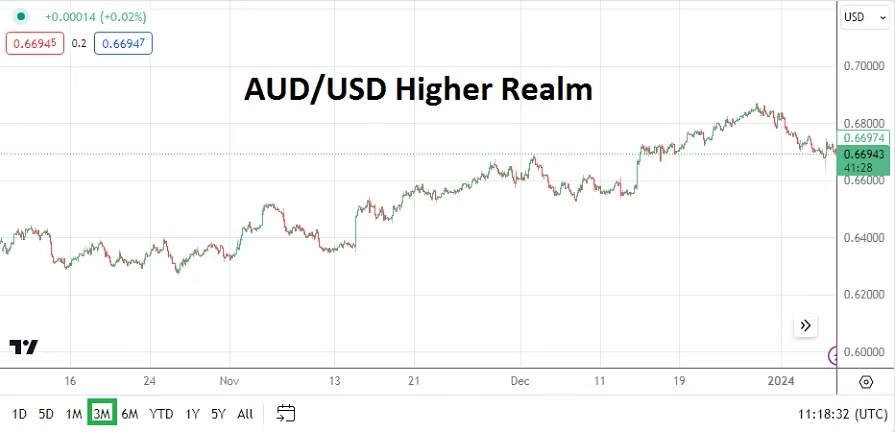

Tuesday, 9th of January, Australia Retail Sales – the anticipated climb of 1.2% is significantly higher than the negative -0.3% result from last month. A good outcome via the Retail Sales could help the Australian Dollar reignite some positive momentum. CPI data will come from Australia on Wednesday, which will certainly affect the AUD/USD too.

Wednesday, 10th of January, U.S Ten-Year Bond Auction – though day traders may not be too involved regarding the sale of U.S Treasuries, the results from the auction will have an affect on Forex. U.S Treasury yields should be monitored.

Thursday, 11th of January, U.S Consumer Price Index – a slew of CPI results will get the attention of financial institutions. The inflation data is expected to show a slight decrease in the Core CPI result, but show a slight gain in the broad number. This will likely be the most heavily traded day since the third week of December. There will be a reaction from the inflation reports. If the numbers come in around the estimates this may help the bearish mid-term outlooks for the USD. If the results are shockingly stronger, the USD would turn bullish. Day traders need to be careful in the midst of the Consumer Price Index publications because volatility is expected.

Friday, 12th of January, China CPI – a decrease is expected from the Asian giant. Deflationary concerns are shadowing China’s economy. The expected number of minus -0.4% would actually be an improvement compared to the last reading which was minus -0.5%. The USD/CNY has been rumored to have been experiencing some ‘hands on’ management from China. Investors continue to be nervous about China’s economic outlook and would like to see signs of improvement.

Friday, 12th of January, U.K Gross Domestic Product – a gain of 0.2% is being anticipated. Any growth from the U.K GDP would be welcomed considering the recessionary data which has been lingering. The GBP/USD will react to the results and bullish momentum in the currency pair could be sparked by a better than anticipated number.