USD/ZAR Considerations as Water Flows and Political Concerns are Compared

As a guest of South Africa (because of a personal relationship) and having been coming here frequently during the past four plus years it is easy to love the nation. Early last week a severe storm which brought high winds and plenty of rain hit a lot of the Western Cape knocking out electricity and water in a variety of towns. Having experienced hurricanes in the past, the wind was not quite comparable, but the consistency of the gusts over two days caused major damage.

Electricity and water have been restored to most people now. Wifi remains a problem for some, but folks are surviving. The damage to homes, infrastructure in towns and agriculture will keep individuals busy for a while. However, the Western Cape because of good political leadership and the stoic mannerisms of the people have worked together to move forward. So what does this all have to do with the South African Rand?

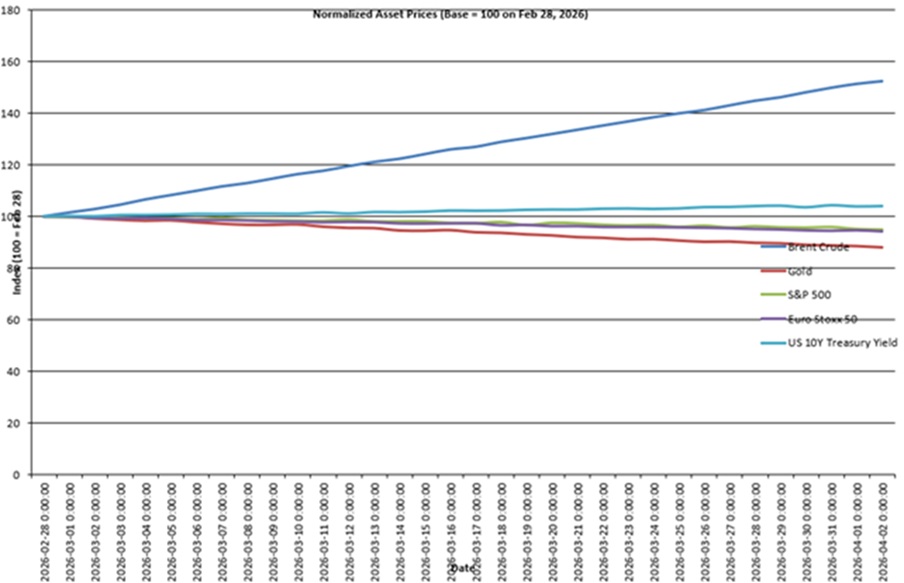

USD/ZAR Five Year Chart as of 20th May 2026

The USD/ZAR is traversing within a higher price realm since the start of March because of the Iranian conflict. The currency pair flirted with depths below 16.00000 in the middle of February. The value of the USD/ZAR at this time is close to 16.70000 depending on bids and asks. The Rand is correlating to the broad Forex market as USD centric strength has emerged recently, this as U.S 10 Year Treasury yields increase and threaten to become sustained. The U.S Federal Reserve is suddenly dealing with threats of inflation becoming sticky over the mid-term because of escalating energy costs. The U.S has plenty of WTI Crude Oil, but nations which had counted on energy from the Middle East are suddenly U.S customers and increased demand is going to cause WTI to remain elevated until the Iranian situation resolves.

The USD/ZAR was in a bearish trend since early August 2025 when values were above 18.00000. The highs in early August of last year were caused by concerns the U.S White House sparked because of tariffs. South Africa is still facing tirades from the Trump administration about some policies being practiced in South Africa, but financial institutions have looked elsewhere regarding impetus for the Rand and its correlation to global Forex is the chief influencer.

While South Africa and its people and culture are easy to embrace, there are issues that remain problematic in the nation. Politics around the world often appear to be a complex myriad because certain people and partisanship are transfixed on power. Corruption globally is an issue in many nations that causes not only fiscal problems but inflation. South Africa suffers from these complications too. These matters can only be fixed with transparency and patience, and importantly – for citizens to demand better.

Politically the current coalition government on the surface appears to be working. Yet, the potential for fractures to grow over the next handful of months as municipal elections approach – the Johannesburg mayoral and city council results will prove fascinating, will be crucial for South Africa. Johannesburg has been facing a water supply crisis for a while and its consequences are a stark contrast to the Western Cape’s ability to repair and replace infrastructure in a matter of days after the recent storm.

The USD/ZAR is likely to correlate to USD centric price action near and mid-term, but there is a chance heightened political rhetoric and voting outcomes in a handful of months could shift impetus for a short while. Higher energy costs in South Africa now and into the mid-term will cause inflation. Food costs do appear to be incrementally rising in supermarkets.

Yes, gold and platinum values will be looked at by some analysts and pointed to as reasons for the stronger South African Rand, and this influence may be real – to a degree. However for the moment, the USD/ZAR remains transfixed within the lower realms of its long-term price range mostly because the coalition government here is viewed positively, and the USD was weaker globally.

The U.S Fed does have inflation concerns arising. As much as President Trump would like the new Fed Chairman, Kevin Warsh, to be dovish the reality for the U.S central bank and financial institutions judging outlooks lacks clarity for the moment. Sideways choppy price action in Forex and for the USD/ZAR may prevail in the coming days and weeks. And if the Iranian situation grows more boisterous, USD centric strength could grow.