AMT Top Ten Miscellaneous Salvos for the 29th of September

10. Profit: OpenAI has announced plans to become a money making corporation. Founded in 2015 the artificial intelligence company had the stated goal of creating ‘safe and beneficial’ technologies via its foundation, and now will face the slings and arrows of investors and potential critics. The AI boom the past two years has produced many new competitors. Can Sam Altman, the CEO of OpenAI, sustain the momentum generated or will negative organizational impetus turn the company into an also-ran?

9. Softs: Cocoa, Coffee and Sugar all remain volatile and playgrounds for day traders who like casino experiences via CFDs. Cocoa is again over 9,000 USD, Sugar touched February highs this past week as it shows signs of extreme speculation, and Coffee Arabica surged to record prices on Thursday and Friday. Over exuberance however is not being created by day traders, it is the work of large institutional traders who are in control. While the ‘softs’ may look overbought it would be unwise to bet against trends while big players pursue bullish notions. Massive money is being made in these commodities, but losses are also being felt by those who wager incorrectly.

8. Escalation: Risks in the Middle East have become a focal point, this as the region appears to have generated more must watch television. The noise which the media seemingly craves is hard to escape. Market participants cannot be blamed for maintaining vigilance as sabers rattle, especially after Friday’s events in Beirut when Hassan Nasrallah, the Hezbollah leader, was eliminated by Israel. However, experienced traders who are also strategic analysts have seen this show before and may turn the channel knowing there will be reruns in the future.

7. WTI Crude Oil: Prices closed within the lower elements of the commodity’s long-term depths. Traders did have a chance to react to Friday’s developing news from Beirut, but the energy sector remained calm. The price of WTI was around 68.57 going into this weekend, after trading at highs earlier in the week. For all the talk about fear of escalation from the Middle East, the price of Crude Oil remains within a remarkable bearish stance as large traders appear to be more concerned about lackluster economic growth globally.

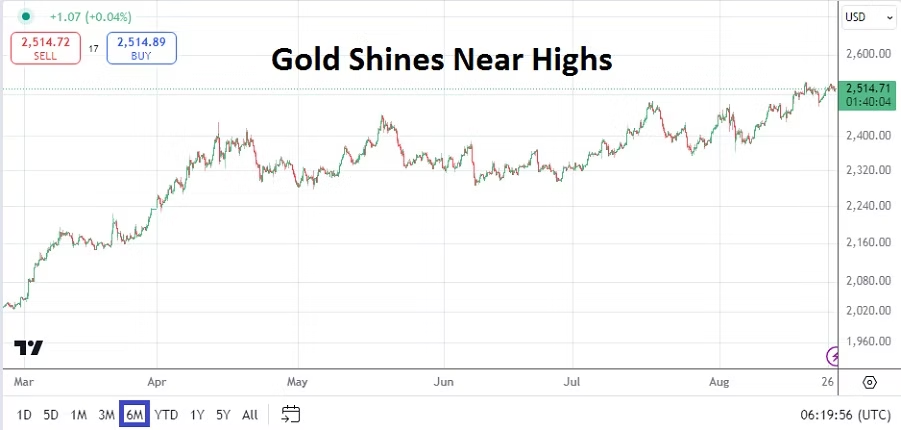

6. Apex Gold: The price of the precious metal flirted with 2,685.00 momentarily on Thursday. The price of gold going into this weekend finished near 2,658.00 USD. Sustained highs have certainly continued to catch the attention of short-term speculators, but they need to be aware the commodity does remain susceptible to sudden spikes. While alluring, gold remains dangerous for day traders.

5. Countdown: The U.S Presidential vote is slightly more than 5 weeks away. Interestingly, the Fed will announce their Federal Funds Rate decision only two days after the election results. Will the outcome of the vote change the Fed’s perspective on interest rates? Financial institutions will definitely brace for the outcome of the U.S vote. Cautious winds will start to prevail as the 5th of November draws closer.

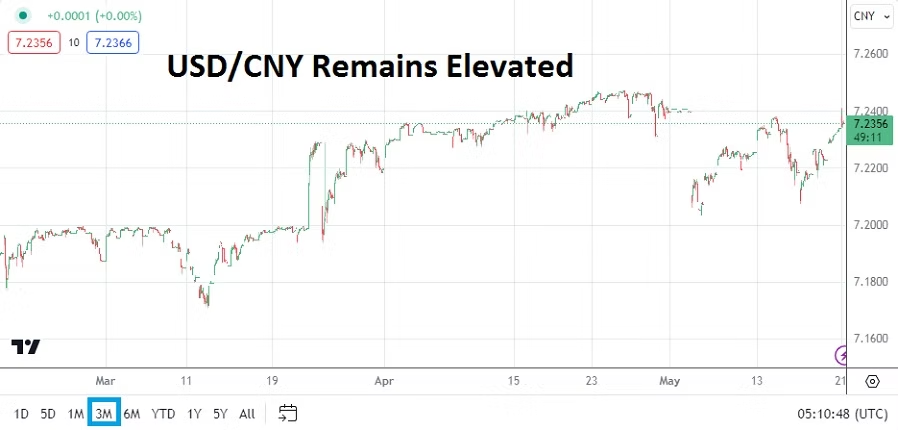

4. China: A huge stimulus package from the Chinese government has been initiated, but talk regarding potential effects and outcomes are being debated. The notion that the Chinese economy is be driven too much with a top to down centralized approach is being vocalized by some worried ‘outside’ observers. The USD/CNY is trading near 7.0105. The Shanghai Composite is near 3,087, this after massive gains via a reversal upwards which was sparked from lows around 2,691 which were seen on the 18th of September.

3. Risk Appetite: U.S equity indices continue to challenge record values in the Dow 30 and S&P 500. Yes, the Nasdaq remains beneath its highs, but is still within sight of all-time heights. Trading this week will work under the shadow of the jobs numbers coming this Friday. Financial institutions have produced rather positive behavioral sentiment and do not seem like they are ready to back away from this stance. Are some large market participants starting to quietly bet on the possibility of a Trump victory which they believe would be good for U.S stocks?

2. Forex: USD centric notions remain the impetus in foreign exchange. The USD Cash Index is within the lower boundaries of its long-term values as it trades near July 2023 realms. If the USD Cash Index moves lower it would then start to technically be within price calculations not seen since the spring of 2022. Action in the USD/JPY and GBP/USD, and other major currency pairs have been volatile, choppy conditions should be expected this week for traders leading into Friday’s key data.

1. Jobs Numbers: Last week’s GDP statistics met expectations, while inflation numbers via the Core PCE Price Index came in slightly below estimates. The growth and inflation outcomes set the table for the Non-Farm Employment Change and Average Hourly Earnings which will be reported on the 4th of October. If the employment numbers continue to trend lower and there are additional negative revisions this coming Friday, this could propel USD selling. Financial institutions are trying to figure out if the Fed will cut by 0.25% or 0.50% in November. The Fed was aggressively dovish when they cut the Federal Funds Rate by 0.50% on the 18th of September, but the U.S central bank might want to be cautious in November following the election and wait for all the dust to settle and cut by only 0.25%. Thus allowing for another interest rate cut in early 2025 if needed. The broad markets are in a reflexive mode for the time being, this Friday’s data will be important and cause an immediate reaction that day traders will notice.