10. Ellis Park, Johannesburg: The Springboks will face the All Blacks on Saturday in round three of the Rugby Championship. One of the greatest rivalries in sports will match South Africa who is looking to cement their current team’s legacy as one of the best rugby squads ever, versus New Zealand who is looking for revenge having lost to the Springboks in the World Cup Final in October 2023.

9. Labor Day: Short-term speculators should be mindful that today’s volumes may be thin due to U.S financial institutions allowing employees to leave early for a long weekend. While all the major U.S exchanges will be operating, transaction volumes will become lackluster as the day progresses with the last U.S summer holiday approaching.

8. Precious Future: Gold is traversing around 2,520.00 USD per ounce this morning, as Bitcoin is near 59,500 USD as of this writing. The precious metal was around 2,000.00 much of February, while Bitcoin began flirting with 59,000 and 60,000 in late February after starting that month near 43,000 USD. While influencers proclaim the future is digital with Bitcoin, Gold continues to shine and has a historical track record as a store of value.

7. Pavel Durov: The CEO of Telegram was released on Wednesday after posting 5 million EUR as bail, he must stay in France and faces a handful of charges. Russia, the UAE and high profile people, including Elon Musk, have publicly criticized France for Durov’s arrest last Saturday. Free speech advocates are largely against the arrest of Durov, while France contends Durov has not been forthcoming about data which has been shared on Telegram to conduct criminal enterprises. Julian Assange was arrested in 2019 in Britain and was only released in June of this year, promptly leaving for Australia.

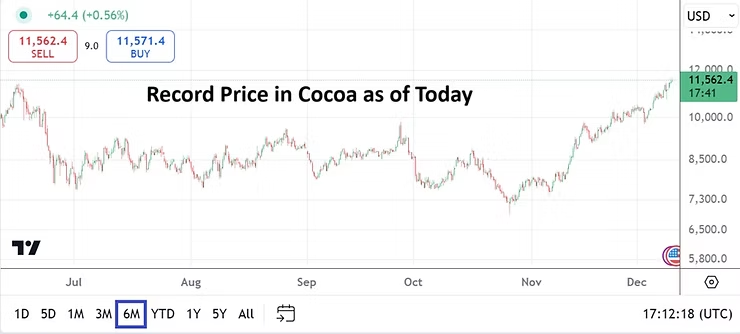

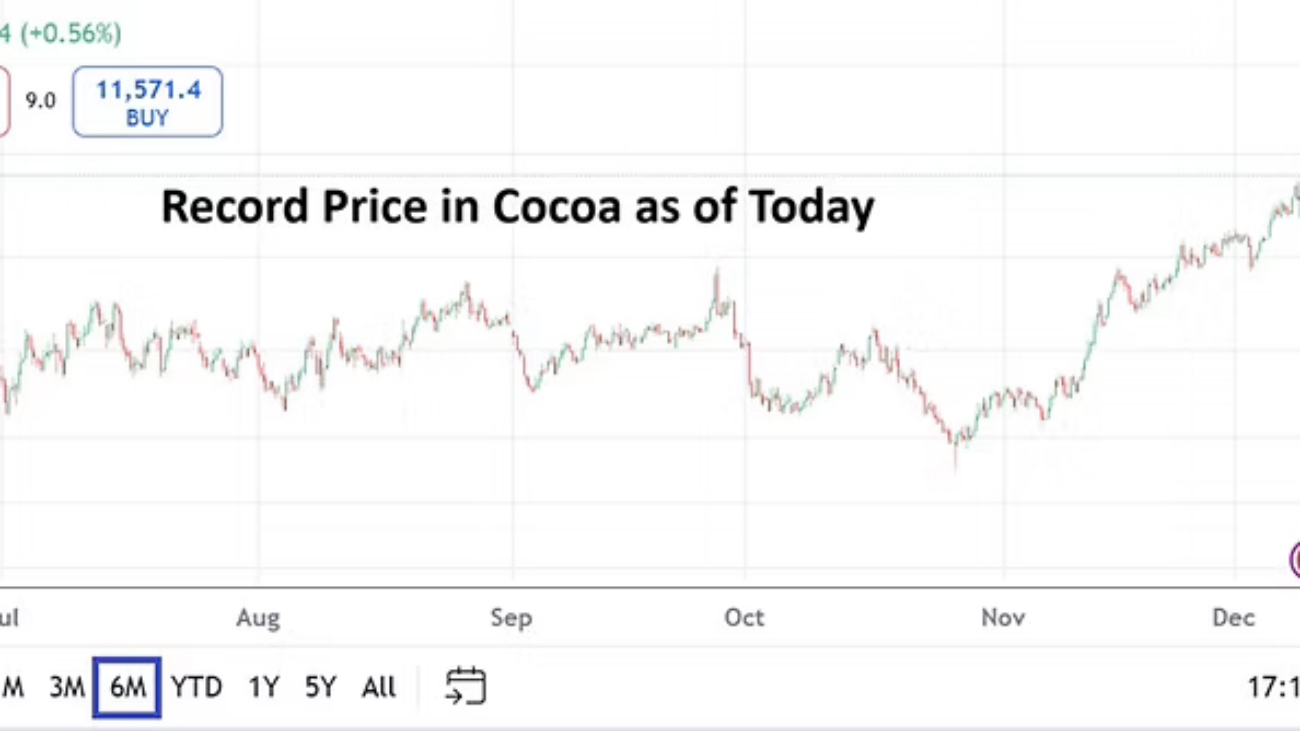

6. Commodities: The price of WTI Crude Oil is near 76.00 USD and remains in a fairly stable range, Cocoa remains within sight of 9,000.00 as it trades around 8,950.00 this morning. And the prices for Coffee via Robusta and Arabica continue to flirt with apex highs. Day trading wagers on these commodities should be done carefully before the U.S holiday.

5. Art of Speaking: Kamala Harris is being criticized for her reliance on teleprompters as some pundits wonder loudly when she will sit for an unscripted interview. Donald Trump faces continued scrutiny for speaking extemporaneously, and everyone knows this characteristic is not going to change. The race for the White House appears tight. The televised debate between the candidates remains on the schedule for the 10th of September and its format may present the opportunity for verbal fireworks.

4. Eastern Europe: The Russian-Ukrainian war has been escalating the past few weeks as both sides appear to be working with the belief they need to create facts on the ground over the next few months. The potential of a victory by Donald Trump in the U.S may be pushing Russia and the Ukraine into a mode which hopes they can bolster their respective negotiating positions, this if the newly elected U.S President can get the warring sides to discuss an endgame.

3. China: The nation faces difficult economic circumstances and tries to maintain stability via Yuan and bonds interventions. Also, the foreign policy stance of China is growing tensions with the Philippines. The long standing disagreement about Taiwan’s sovereignty is well documented, but Chinese naval activity in the South China Sea is raising alarm bells among some political analysts. Manufacturing PMI results will be published by China early on Saturday. Economic data from the nation is being inspected by foreign investors carefully who are looking for long-term yields, but are troubled about transparency and the potential of sudden policy changes.

As an aside, APEC will conduct its annual meeting in November from the 10th until the 16th in Peru. Both Joe Biden and Xi Jinping will attend. Depending on Biden’s health and the outcome of the U.S Presidential Election on the 5th of November, this Asian-Pacific Economic Cooperation Forum will prove important.

2. U.S Data: Jerome Powell’s capitulation last Friday via his public statement that the Fed needs to cut interest rates fueled a weaker USD. Forex has seemingly priced in a combined 0.50% basis cut via the Fed for September and November. Yesterday’s stronger than anticipated U.S GDP growth and inflation reports however created headwinds, which caused outlook jitters. Today’s Core Personal Consumption Expenditures Price Index monthly gauge is expected to come in with a gain of 0.2%. If the inflation report can match the anticipated result this may calm Forex, equity indices, and Treasury yields before going into the long holiday weekend. Next Friday U.S Non-Farm Employment Change numbers will be published. Today’s trading may be muted because of thin volumes, but day traders should expect volatility to increase starting next Tuesday.

1. Competition: Nvidia was valued around 47.50 USD per share this time last year, as of today the price is near 117.60. Intel’s value was approximately 34.50 USD this time last year, as of today the price is about 20.13 per share. Intel appears to be valued as a commodity supply company nowadays by some investors, while Nvidia’s outlook remains within the auspices of a highly anticipated technological future. Where will both companies values be this time next year?