AMT Top Ten Miscellaneous Postings for the 5th of April 2024

10. Petrichor: The pleasant smell after a rain has fallen following a long dry spell which elicits earth’s fragrance. The Fed is likely hoping for this sensation via ‘weaker’ Non-Farm Employment Change numbers today. In December the Federal Reserve spoke about data signals needed in order to cut interest rates. If jobs statistics are stronger than anticipated, there will be no ‘petrichor’ for the Fed.

9. Underreported: Five engineers from China on their way to work for the Dasu dam project they participated, were killed in a ‘suicide’ terrorist attack in Pakistan on the 26th of March. Terror attacks in Pakistan on Chinese involved with infrastructure ‘Economic Corridor’ work have been increasing.

8. Qubits: Microsoft and Quantinuum recently announced they have made breakthroughs regarding quantum computing research reliability. Results have shown 14,000 ‘test routines’ without errors. The emergence of quantum technology approaches.

7. Intrinsic Value: Cocoa is near 9640.0 USD per metric ton as of this morning and remains speculatively energetic. Bitcoin is slightly below 67,000 USD and continues to ‘beat’ the notion that intrinsic value is important.

6. Precious: Gold prices have ‘fallen’ below 2300.00 USD per ounce, and is near 2289.00 for the moment, but the metal is shining as crowds admire its ability to create a safe haven.

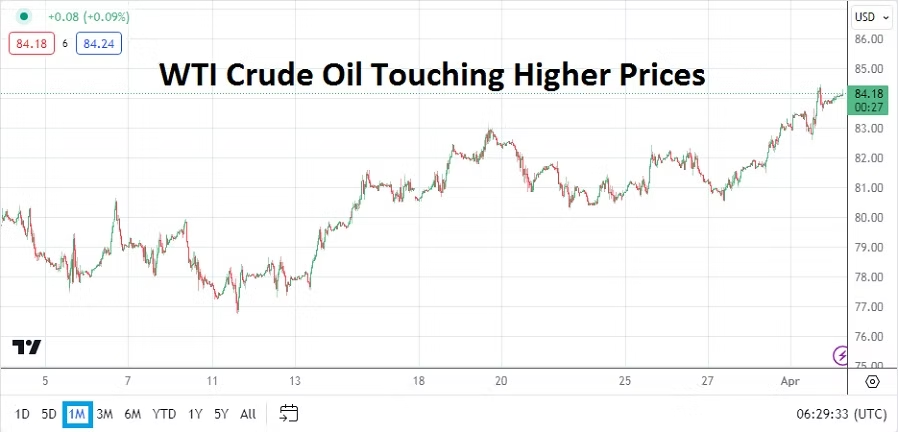

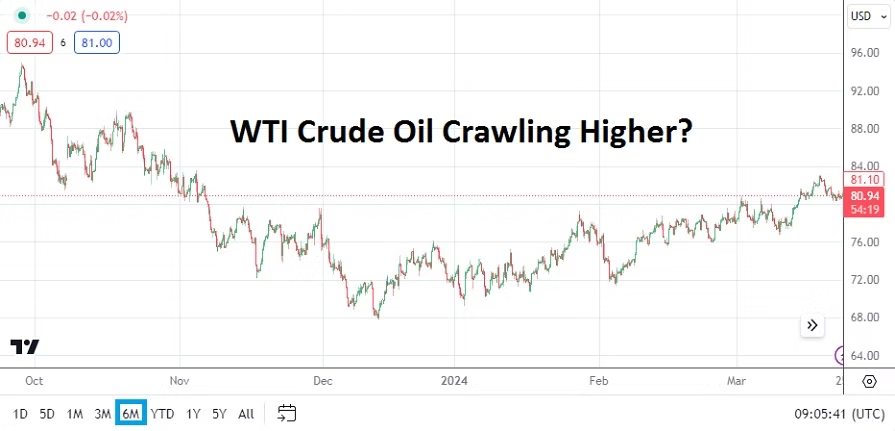

5. WTI Crude Oil: Middle East news is rumbling and hyperbole is resonating, the price of the commodity is over 86.40 USD per this writing. A calm weekend, and peaceful end to Ramadan this coming Tuesday might help calm nerves. Higher oil prices will not help global inflation.

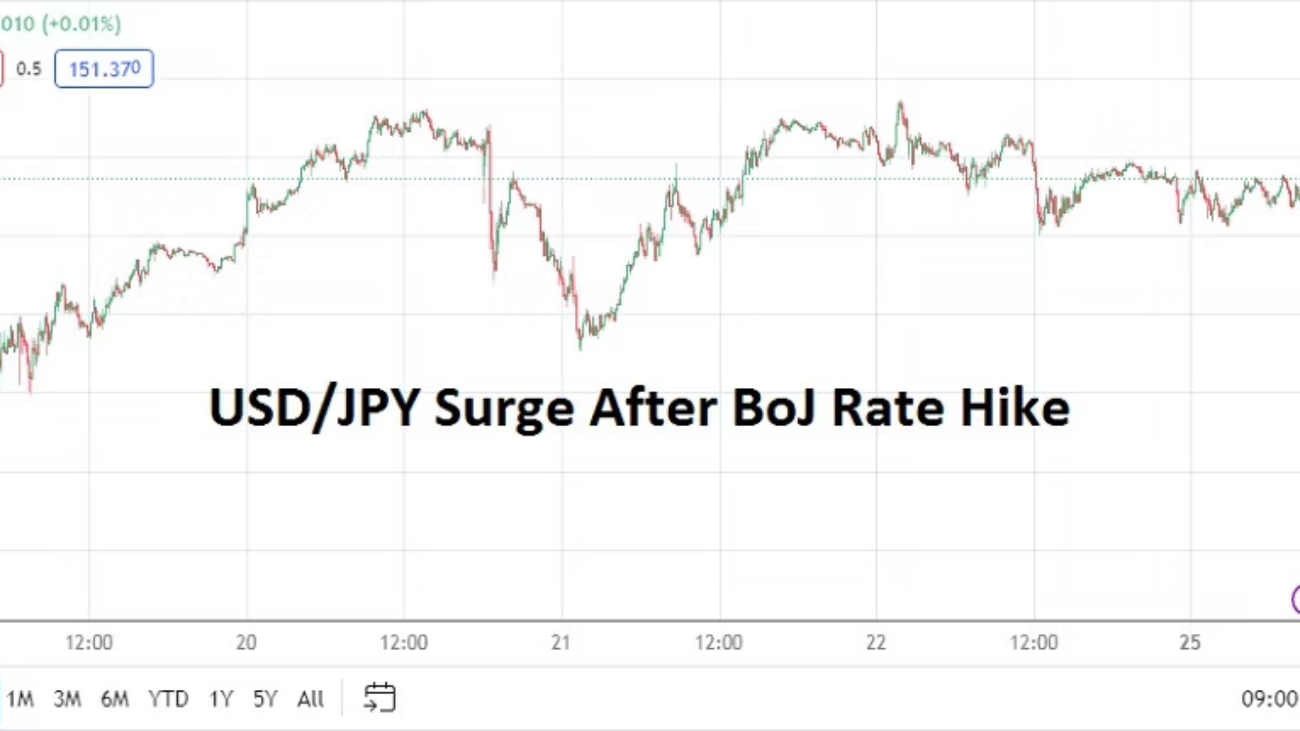

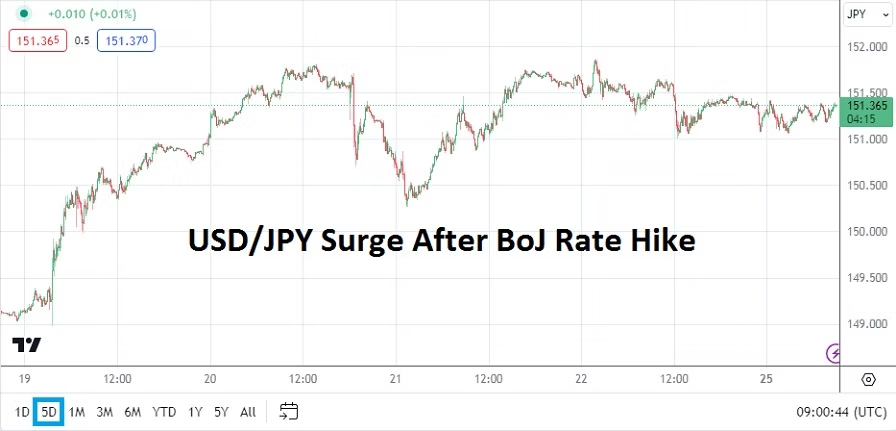

4. Forex: The USD/JPY has started to experience waves of volatility and has recently challenged long-term highs. Bottom line is the notion that large players are positioning for today’s U.S data which will affect all financial assets as USD centric power resounds.

3. Equities: The U.S major stock indices are beginning their day near lows not seen since the 15th of March for the Dow 30, and the 19th of March for the S&P 500 and Nasdaq Composite. Nervous?

2. Bonds Watch: U.S Treasuries need to be monitored as the 5, 7, and 10-Years Notes respond to nervous investors and fears of a new ‘inversion’. Having come off of high yields a couple of days ago, doesn’t mean all is well as values languish near late September 2023 technical realms.

1. Data: Recent chatter from many Fed FOMC members have created anxious investors. Vivid reactions will occur after the Non-Farm Employment Change and Average Hourly Earnings. Bluntly, today’s jobs reports are crucial and the Fed would like the results to be weaker than anticipated in order to consider cutting interest rates. However, if hiring comes in stronger, it would be a sign of a resilient U.S economy and would ignite more USD strength. The first half hour following the jobs numbers may look counter-intuitive regarding price action as financial institutions adjust their trading positions.