India Insider: Strategic Balancing Act Comes with Risks

On the 15th of August, India’s Independence Day, Prime Minister Narendra Modi announced a large reduction on Goods and Services Tax rates to boost domestic consumption. The Indian economy is certainly slowing, this as lackluster domestic consumption has prompted the Reserve Bank of India to cut the repo rates from 6.5% to 5.5% in 2025.

As trade deal discussions with Washington flounder, New Delhi is being forced to shift economic considerations towards China. The diplomatic relationship between India and China has grown colder, particularly since they clashed on the eastern border region in 2020.

Relying on China also comes with challenges for New Delhi. Since 2021, the trade deficit with China has expanded from $73.3 billion to $99.27 billion USD, showing that India still depends increasingly on China for significant importing needs.

According to Bloomberg, India’s major conglomerates have already established excellent relationships with Chinese suppliers of lithium ion batteries and EV components, although they try to discreetly tread under the radar in order to avoid the wrath of New Delhi government.

The fact is India can sustain its economy and maintain its geopolitical posture of non-alignment by practicing a multi-polar stance with Washington and Beijing. But despite clinching trade deals with the U.K and reviving trade negotiations with the E.U, New Zealand & Australia, and its deepening bilateral relationships with many central Asian nations and within BRICS, New Delhi’s major trading partner for exports remains the United States. Around 18% of India’s exports go towards the U.S, while 15% of imported goods come from China. The numbers do demonstrate an intriguing balance.

While India’s negotiations with the U.S have stalled and appear postponed indefinitely, other Southeast Asian countries, including Vietnam, Indonesia and the Philippines have secured lower tariffs with the Trump administration making them more competitive in the U.S. market. These nations are using the U.S for economic and military security, but they also rely on China for manufacturing and logistical needs.

India Faces Additional Challenges with Washington and Beijing:

Indian IT companies derive nearly 57% of their export revenues from U.S clients, making them heavily dependent on that market. And rapid advances in AI and the erosion of legacy outsourcing models are putting India’s traditional profit engines under pressure.

Meanwhile, China is not keen on helping India achieve expertise and manufacturing competitiveness which would threaten its own business model. China wants to make inroads by selling goods to the world’s largest consumer market, rather than technology transfers which would allow India to attain manufacturing supremacy.

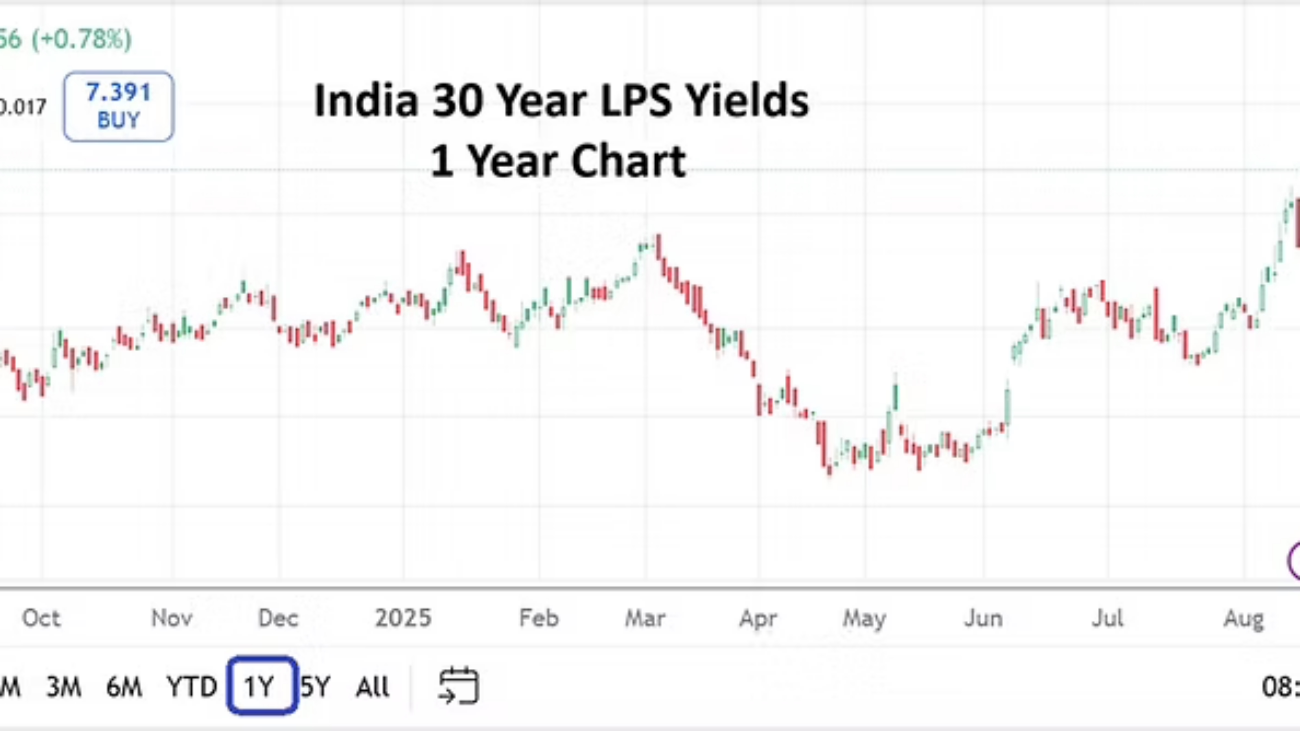

Some economists warn that India’s own plans for mitigation of its current circumstances will likely be disinflationary. India’s bond results via yields clearly express concern about potential fiscal costs and difficulties. New Delhi’s focus has shifted towards appeasing domestic consumers, while trying to deal with uncertain foreign partners. Government capital expenditures have been declining since last year, signaling that both corporate and public investment confidence remains weak.

India’s neutrality is welcomed. It’s not anti-Western or pro-Western, and attempts to balance between the U.S and China while trying to forge new trade agreements and ties are a constant high-stakes game capable of creating strains economically and politically. The path forward with the U.S and China will remain complex and it must be worked on with precision in order to help achieve success.