India Insider: Manufacturing Strategy to Create Rural Jobs

Across much of India’s rural landscape, manufacturing remains scarce and finding a solution for this remains a priority. While some towns do have small scale industries that offer jobs, this is still limited. As of financial year 2023, agriculture accounts for only 16% of India’s GDP, down sharply from around 35% in the 1990s, due to a structural shift toward services and manufacturing.

A large share of rural families still depend on agriculture, often engaging in farming and irrigation with modern equipment. However, marketing their produce remains a persistent challenge. Meanwhile, many rural workers are engaged in low-wage trade and commerce, often in informal settings such as small shops and roadside businesses. These roles typically offer limited income and little upward mobility. Falling real wages have pushed many to migrate to India’s urban centers or venture overseas to Singapore, Malaysia, and the Gulf countries in search of better livelihoods, aided by favorable exchange rates.

Capitalism and Efficient Manufacturing

Adam Smith, in his seminal work The Wealth of Nations wrote that, ‘it is not by gold or silver, but by labor that all the wealth of nations is created’. This fundamental idea underpins the modern economic thought that wealth is not derived merely from money, but from the productive capacity of people.

When capital is invested in a capitalist enterprise, it generates profits for the owner, provides wages for employees, and delivers returns (such as dividends) for shareholders. But this cycle of value creation depends on active and efficient enterprise, particularly manufacturing which has been missing or underdeveloped in many parts of rural India.

Unlike countries such as the United States, where people readily relocate across States, India faces some unique challenges. Like the European Union, India is a union of diverse linguistic and cultural regions. It is uncommon for a small business owner from Himachal Pradesh to directly access markets in Tamil Nadu or Karnataka due to language barriers, cultural differences, and logistical constraints. These frictions further isolate rural producers from wider markets.

Strategic Solutions and the Role of State Governments

To revive rural economies, business people along with their state governments must identify and invest in strategic sectors that create jobs and add value. Kerala is a fine example: as one of India’s top spice-producing States, Kerala has the potential to establish local industries focused on spice processing, packaging, and export. Coordination between agriculture and manufacturing can generate employment, stimulate local economies, and enhance foreign exchange earnings.

Albert Hirschman, a development economist, highlighted this approach through his theory of unbalanced growth and economic integration. He argued that certain industries have strong reciprocal connections with other parts of the economy. By prioritizing sectors with good synergy potential, developing countries can achieve significant growth even with limited resources.

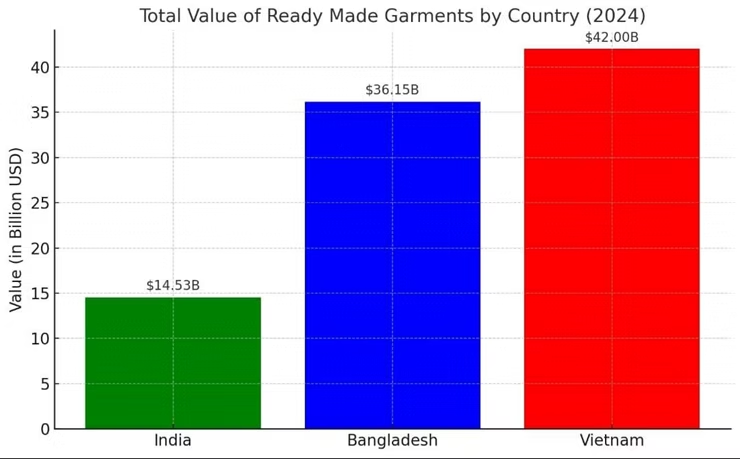

Growing competition from countries like Bangladesh and Vietnam which both enjoy favorable trade agreements do pose new challenges, this must be taken seriously by India and create a focus on forward looking international commerce. There will always be competition from distant enterprises and nations, this must be accepted and planned for via commercial insights.

Within India is Tiruppur, a city in Tamil Nadu, known as the ‘Manchester of South India’ due to its vibrant textile industry. The city has created an ecosystem of manufacturing that consistently offers higher real wages compared to other towns in the region. It has successfully shifted labor from agriculture to industry, thereby increasing productivity and income. It is a bright example and defines one way to make progress.

Protecting New Industries and Creation of Success

In his book How Rich Countries Got Rich and Why Poor Countries Stay Poor, economist Erik Reinert argues that nations develop not just by doing what they are currently good – such as agriculture or mining, but by nurturing industries that can become more productive long-term. Typically manufacturing and technology sectors lead to greater innovation and economic resilience.

Reinert provides numerous examples, like South Korea’s emerging growth in steel and its automotive industries, and Ireland’s rise in information technology where specific protections and support for young industries has led to long-term prosperity.

India’s rural transformation cannot rely on New Delhi alone. State governments along with business people must take the lead by identifying sectors that have the potential to foster high growth and employment. Helping to create local value chains, investing in infrastructure, training, and market access will build resilience in these communities. By encouraging small-scale manufacturing and leveraging regional strengths, the country’s rural areas can become engines of economic growth.