Valuations and Drinking, Bad Storms and Politics Amidst the Resilient Nature of People

10. Resilience: The Western Cape of South Africa endured strong storm conditions last week. One of the hardest hit areas was the Cape Winelands District, but electricity and water have been widely restored. And a collective of people have proven working together can produce solid results when needed.

9. Spencer Who: The Los Angeles mayor race is growing intriguing. A reality star turned social influencer threatens to become an influenza for his opponents. This as Spencer Pratt’s campaign gets noticed for its entertaining social media videos. This has caused many folks to ask what has happened to the state of politics and meaningful policy. But if NYC can elect a socialist, why can’t L.A elect an influencer and make some people feel sick?

AMT Top 10 Miscellaneous Insights for the 18th of May, 2026

8. Two Trillion: SpaceX early investors have agreed to allow a five for one stock split, meaning the company (and Elon Musk) are now aiming for a potential doubling of its worth when its IPO is initiated – on Nasdaq – in the second week of June. Some very serious accountants will be kept busy trying to show how SpaceX will produce enough revenue over the next twenty years in order to make a 2 trillion USD valuation palpable to future investors.

7. Drunk: Brown-Forman Corporation will begin its trading near $26.28 on the NYSE today. The company is the majority owner of Jack Daniels and other alcohol related enterprises. The value of Brown-Forman Inc. in June of 2021 was around 80.00 per share. The sobering phase of the public – particularly among young drinkers – to avoid bars and clubs, and instead stay on their mobile phones has hurt share values in many alcohol related companies. There are also concerns that too many drink companies now exists. Before Brown-Forman becomes the life of the party again, it appears some competition will have to go dry.

6. Deals: Prime Minister Modi visited Abu Dhabi a few days ago, and one of the results was an agreement to purchase and store energy reserves on a large scale in the United Arab Emirates. Modi also confirmed India’s strong connection to the UAE politically. While always trying to maintain a non-aligned stature, India appears to be moving closer to an increasingly important alliance with the UAE – which has also aligned with Israel strategically. The potential of these three nations acting together will ruffle feathers in a few noteworthy Middle Eastern and Asian countries.

5. Populists: President Trump’s tendency to say outlandish things and then suddenly turn around and show a willingness to negotiate terms has always been part of his art of the deal composite. However, saying what people want to hear and then turning on a dime and not delivering is also a symptom of populism. Trump isn’t the only politician suffering from this flaw. What do politicians really think, and how differently would they act if a they didn’t need votes for themselves or backers to remain in power?

4. Wall Street: After attaining apex highs early last week, the three major indices have taken a step backwards. Near-term concerns are effecting outlook as financial institutions balance risk averse tactics to long-term belief that sunnier days will prevail. While the Dow 30 didn’t set a record last week, the ability of the index to climb above 50,000 was noticeable. Equity markets appear tentative as this week begins and folks seemingly wait for more thunder and its potential effects.

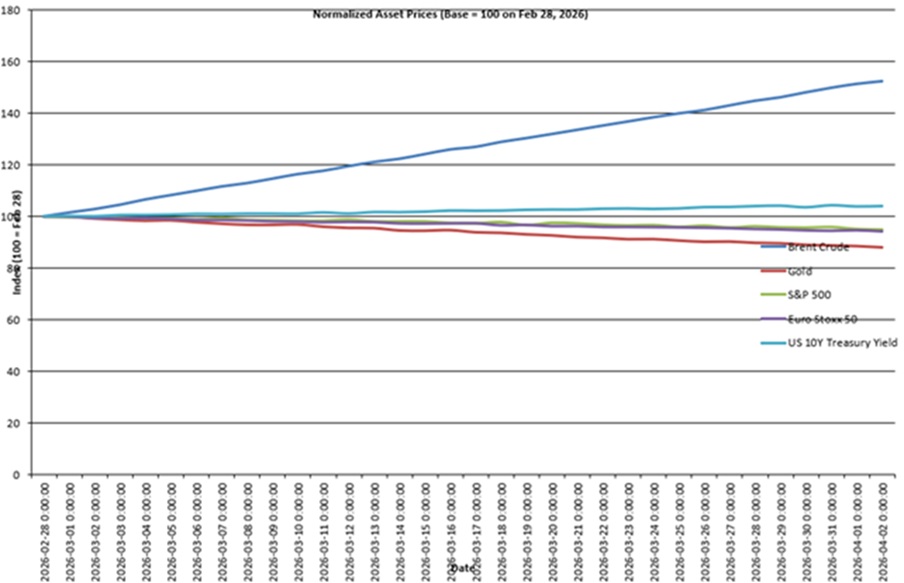

3. Emirates: The UAE was attacked by drones yet again yesterday, this time at the Barakah nuclear facility. The hit has been downplayed, but highlights that military conflict with Iran remains very possible across the region. It is doubtful conversations are being conducted with polite undertones behind closed doors. The U.S, Israel and other nations are watching Iran – and Iran is watching them. The price of WTI Crude Oil remains a key barometer regarding the markets and concerns about the war igniting in full once more. Prices of oil remain sustained above $101.00 per barrel in the futures markets. The UAE might not want to be a focal point, but it isn’t backing down either.

2. Hawkish: The U.S Federal Reserve may have to actually consider raising interest rates before they can realistically discuss the notion of cutting borrowing costs, particularly if energy prices remain elevated and spark a sustained inflation threat over the mid-term. The USD started to show renewed strength the past few trading sessions in Forex, this as financial institutions compare their near-term anxiousness to growing concerns about mid-term ramifications regarding higher fuel costs.

1. Ego vs. Hubris: The U.S and China summit held largely in Beijing this past Thursday and Friday matched competing politicians and ideologies. In one corner U.S President Trump spoke with a rather inflated sense of himself while he detailed policy objectives and his perspectives. In the other corner Xi Jinping, the President of China, might have displayed some hubris as he warned the U.S about the Thucydides Trap. Xi expressed his belief that China is the emerging super power and that the U.S is a declining nation. However, China’s economy is known to be suffering because of a myriad of complex reasons, and could face more headwinds if energy prices and supplies remain hard-pressed.