Last week finished with another reminder that inflation cannot be easily scoffed at by investors who continue to believe higher prices will eventually slowdown. Average Hourly Earnings last Friday came in above the expectation and this was enough to rattle Wall Street again, which saw the major equity indices decline and bond yields incrementally rise. Inflation ‘talk’ will remain important this week because of coming U.S data.

Real Estate including REITS becoming a Topic of Discussion as Mortgages Rise

Market watchers should also pay attention to news regarding mortgages on residential homes, and listen for troubles from the commercial real estate market, as these sectors deal with rising interest rates in the U.S and U.K. Increased nervousness within these markets could have an affect on behavioral sentiment. Let’s remember the catalyst for the financial crisis of 2007 was the real estate sector.

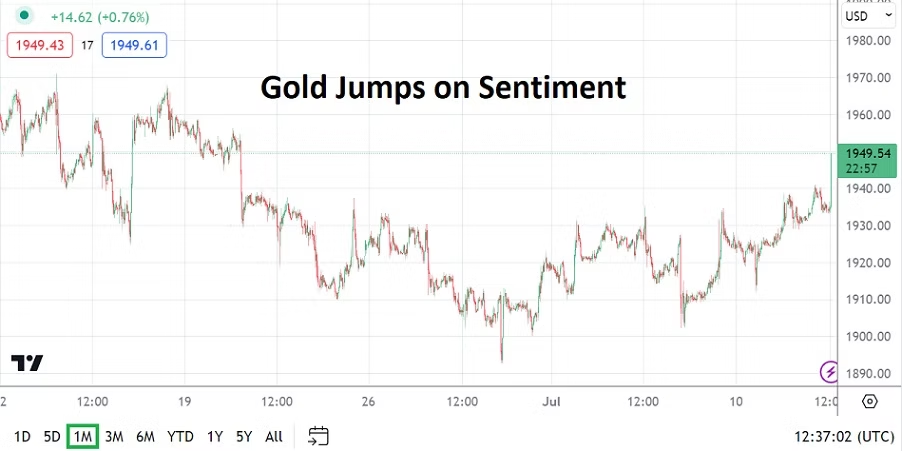

Which brings us back to inflation and the growing acceptance among investors the U.S Federal Reserve may be ‘forced’ to hike the Federal Funds Rate on the 26th of July, if price data continues to come in ‘hot’. Some investors will likely be heard saying an increase of 0.25% has already been factored into marketplace, but the prospect of another hike in late 2023 could be problematic. Forex, gold and bonds dynamics will tell us a lot when this week concludes regarding outlooks.

BNB/USD Price Should be Monitored as Binance Trembles

An outside source of financial and speculative news is likely to come from cryptocurrency. If you are gambling on this asset class (or should we say commodity based on hot air) and like the adventure of wagering, please continue to pay attention to Binance which is showing signs of duress. If the Binance cryptocurrency exchange shows additional signs of pressure on its BNB (Binance Coin), trading waters within the world of crypto could trigger additional drowning victims. If you thought the Sam Bankman-Fried story made interesting news last year regarding fraud and other criminal activity, the FTX saga could prove to be only the tip of the iceberg.

Data Events Ahead to Watch

Monday, 10th of July, China CPI and PPI – the inflation data could prove important for investors who correlate economic statistics from China into their global forecasts. Traders within India should pay attention to these Chinese price reports, because global investors are starting to shift their assets into the Nifty 50 and other NSE equities because of risk and reward equations.

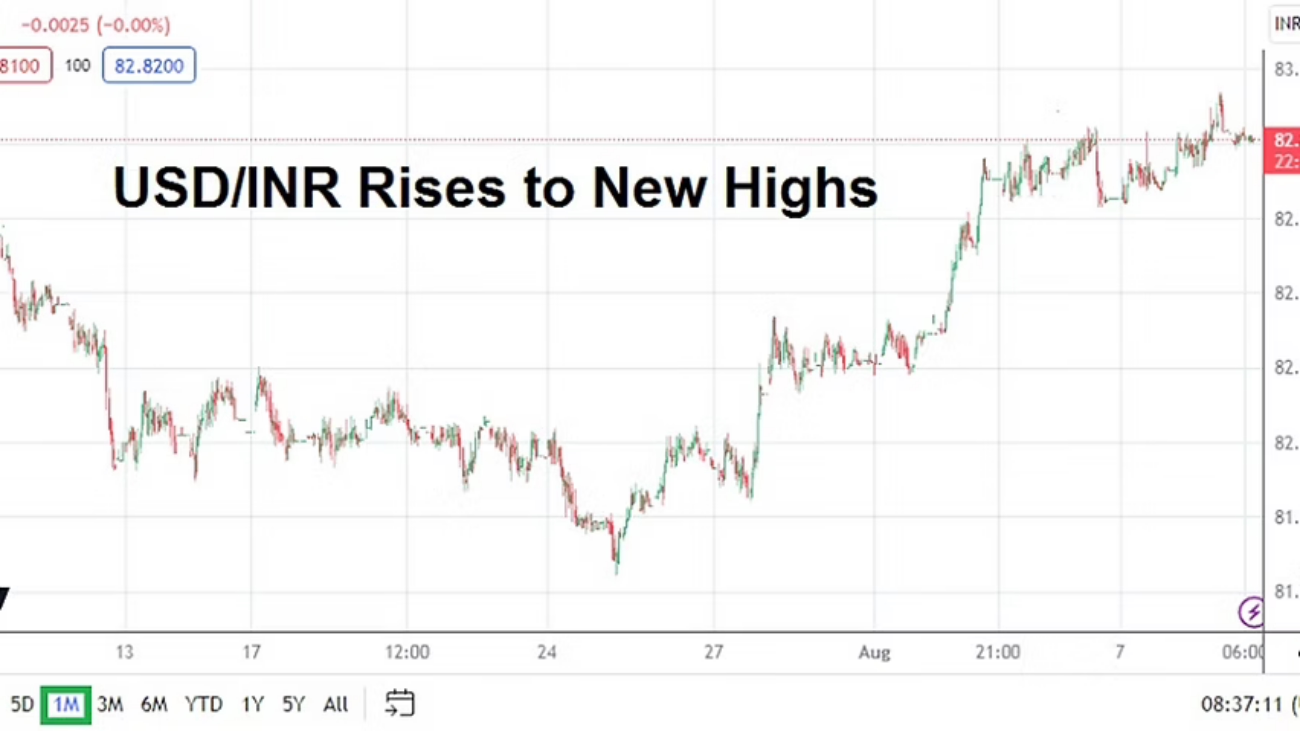

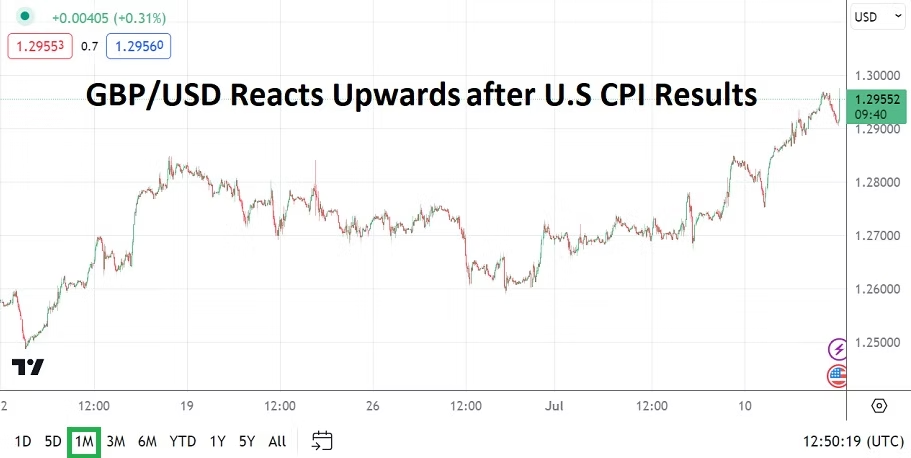

Tuesday, 11th of July, U.K Claimant Count Change and Average Earnings Index – the numbers need to be watched by GBP/USD speculators. The results from the U.K will be intriguing because of employment results, but more importantly for inflation concerns and the knock-on effects. Bank of England Governor Andrew Bailey is speaking a few times this week, and this includes Wednesday the 12th of July, when he will talk about the Financial Stability Report. The GBP/USD has moved towards monthly highs recently.

Wednesday, 12th of July, New Zealand RBNZ Official Bank Rate – NZD/USD day traders will want to pay attention to the central bank’s Rate Statement. While no increase of interest rates is predicted, the Reserve Bank of New Zealand at a minimum will likely have to admit inflation remains a concern.

Wednesday, 12th of July, U.S Consumer Price Index – the inflation reports from the States will have all eyes on the outcomes of the monthly and annual comparisons, including the Core numbers. The results from these inflation statistics will certainly cause momentary volatility within Forex with the USD as the focal point.

Wednesday, 12th of July, Canada BoC Overnight Rate – the Bank of Canada is expected to hike its interest rate by 0.25% to the 5.00% mark. USD/CAD will react to the BoC Rate Statement based on its outlook.

Thursday, 13th of July, U.K Gross Domestic Product – the ‘growth’ numbers are not expected to be positive. A drop of minus -0.3% is the expectation. Talk of recessionary pressures in Great Britain will be heard. Unfortunately, the discussion about a struggling economy, mixed with stubborn higher prices for consumers and mortgage rates that are rising will not make for calm stomachs. U.K equity results via the FTSE 100 Index should be monitored.

Thursday, 13th of July, U.S PPI – the Producer Price Index figures will be the last cog within the important inflation data for the week. Stubborn prices for wholesale goods are a concern, because the costs to consumers becomes more expensive when there are higher price pressures.

Friday, 14th of July, U.S Consumer Sentiment via the University of Michigan – if the Consumer Sentiment readings from the UofM report improves, and the U.S inflation data which was released earlier this week has proven stubborn, this could become a source of pain for investors who may be forced to consider the Fed will not only raise the Federal Funds Rate late July, but later in 2023 also. Short-term traders should monitor this report accordingly.