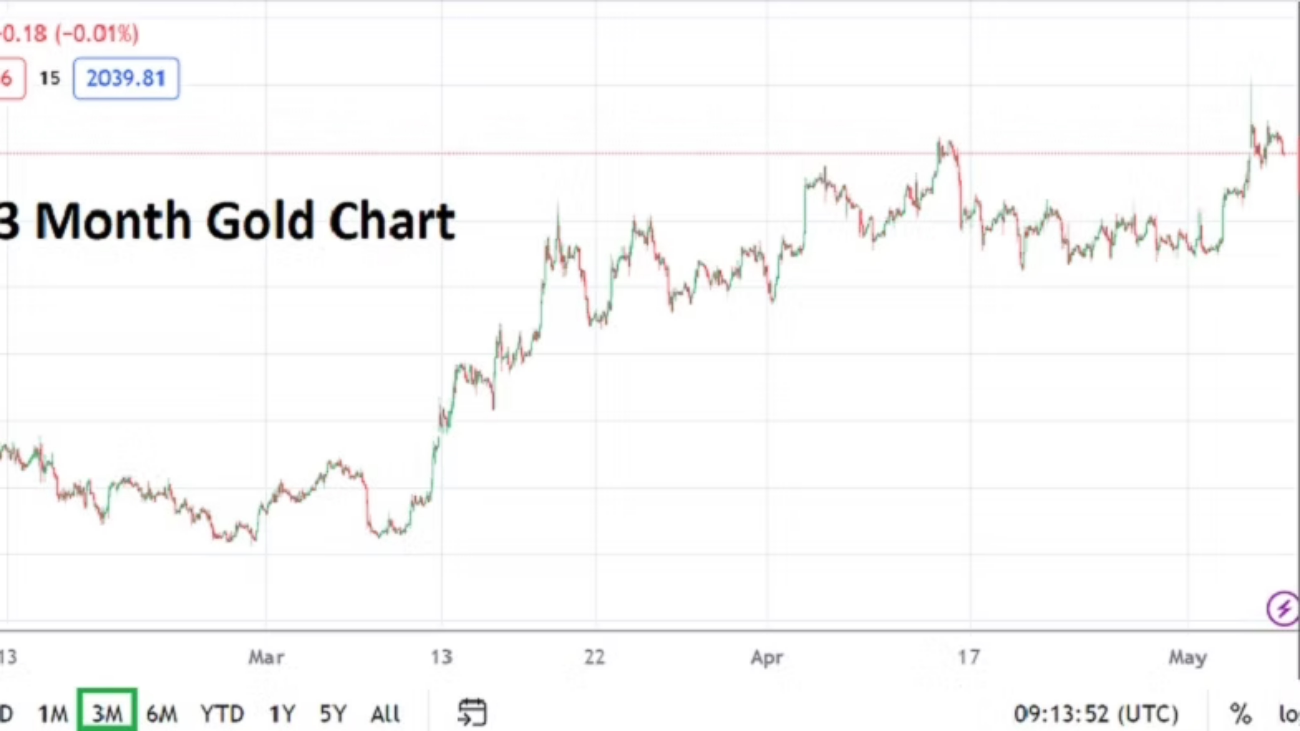

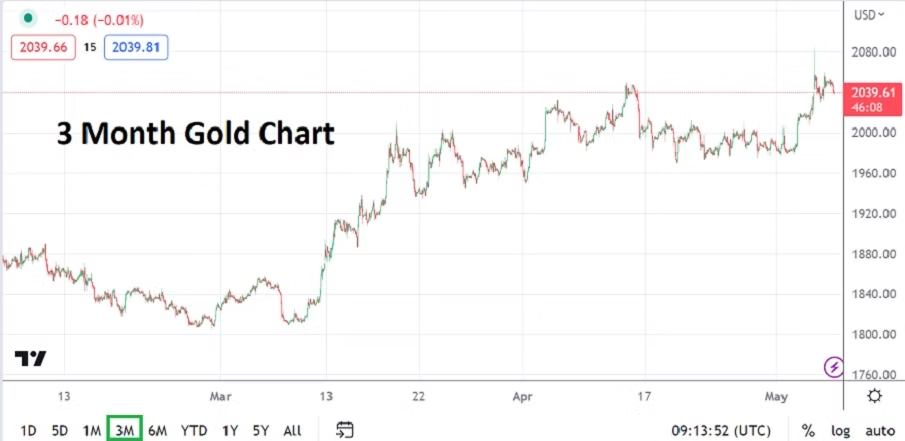

Last Week Caught Many by Surprise, as Fed Looms Wednesday

The ECB obviously decided to highlight how seriously they want to fight inflation last Thursday, when they increased their Main Refinancing Rate by a quarter of a point. The move was not only a surprise to many financial institutions, but displayed a large ‘miss’ by most analysts. While some point out the European Central Bank is powered by Germany who have a historically bad memory regarding inflation, it would also be correct to acknowledge the ECB is trying to protect their own currency against the potential volatility the Federal Reserve could cause with a rather aggressive monetary policy stance this coming Wednesday.

Another broad market influence as this week begins remains the high price of Crude Oil which has now surpassed 90.00 USD per barrel. The higher energy price will certainly not calm inflation anxiousness. Higher energy costs equate into costlier logistics, manufacturing, and agricultural production – this is not a problem central banks wished upon their plates as the final quarter of 2023 gets set to start in a couple of weeks.

Monday, 18th of September, Canada Housing Starts – the housing market in Canada is important to its economy and the nation has enjoyed a housing price bubble for a couple of decades. The past two months have produced higher than expected Housing Starts numbers which is intriguing because Canada is suffering from lackluster growth. The USD/CAD could move slightly on this result, but unless there is a profoundly surprising number from this report, the currency pair will remain focused on ‘other’ things to come.

Tuesday, 19th of September, Canada Consumer Price Index – last week’s CPI and PPI numbers from the U.S came in stronger than anticipated, and Canada’s projected estimates for Tuesday’s results nearly match the nation’s total from last month. Leaving the suspicious notion that inflation could possibly come in stronger in Canada like it did in the U.S last week since these two economies often mirror each other.

Wednesday, 20th of September, China One and Five Year Loan Prime Rates – China continues to be watched closely as investors point out potential dark shadows creating headwinds for the nation economically. The results regarding the loans taken by household and businesses are a solid barometer for outlook if the data is transparent.

Wednesday, 20th of September, U.K Consumer Price Index – the anticipated numbers expects an inflation result of 7.1%, which would be remarkably high and not treated kindly. The results will create havoc in the GBP/USD because not only is the Fed is waiting literally in the wings after this report, but the BoE is going to respond on Thursday.

Wednesday, 20th of September, U.S Federal Reserve Funds Rate – one week ago this day didn’t look like it would cause that much excitement. This all changed last Thursday when the ECB raised its borrowing costs and put financial institutions into a full state of alarm. Yes, the ECB may have acted on its own, but some suspect they know what the Fed is planning on doing already. The Fed is not expected to raise interest rates, but they will certainly sound aggressive and point out inflation remains a danger. Here’s the thing, the ECB sounded quite confident last Thursday, that it will not raise its interest rates again in the mid-term, essentially saying they were done. Did the ECB base this on knowledge that the Fed could do the same thing? What was perceived as a potentially sleepy and quiet Fed meeting and FOMC Statement has now taken on major importance. Forex, U.S Treasuries and global equities will move based on the Federal Reserve’s action and rhetoric. How will the Fed react to higher inflation data?

Thursday, 21st of September, U.K Bank of England Official Bank Rate – the BoE is widely expected to raise the borrowing rate by a quarter of a point. If the Fed did not raise rates the day before and the BoE acts as expected, this could in theory help the GBP/USD gain. However, it should be pointed out following the ECB’s interest rate hike last week, the EUR/USD traded into this past weekend weaker.

Friday, 22nd of September, E.U, U.K and U.S Services and Manufacturers PMI – Europe, Great Britain and the U.S will all release this data on Friday and all expect rather lackluster results. While this data is important, the broad financial markets will likely still be reacting to the actions of the major central banks and the credit crunch problems they are causing globally for consumers and businesses who are facing cash shortfalls and costlier loan expenditures.