EUR/USD and German Elections: Saying Quiet Thoughts Out Loud

The German Federal Election is taking place today and an expected shift to the right is being anticipated via the German voting public. The EUR/USD will react to the trading results tomorrow on Monday, and speculators who do not have deep pockets may want to remain on the side and simply watch the volatility as it develops.

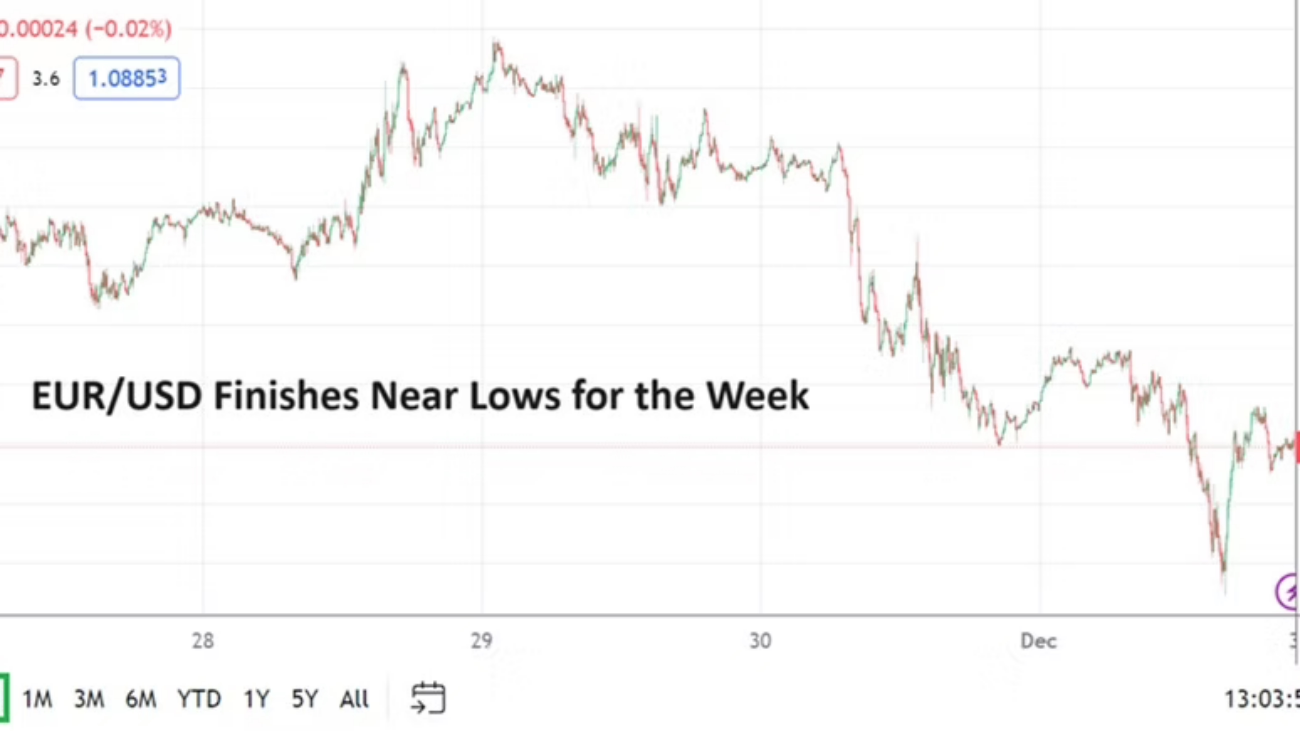

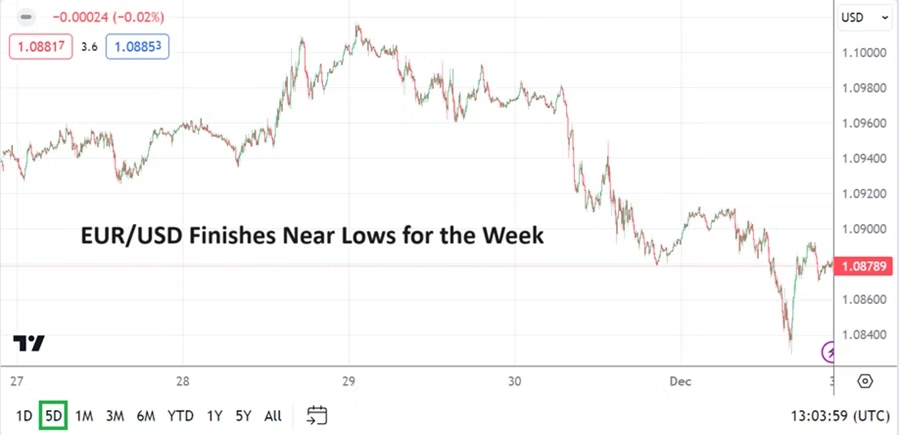

After touching highs late last week which brought the 1.05000 vicinity into focus, also challenging the highs seen in the previous week, traders started to sell the EUR/USD going into this weekend. Financial institutions will react to the results from the German vote and if the Christian Democratic Union wins with strong results, and the AfD (Alternative for Deutschland) takes more seats than some anticipate this will cause an immediate reaction in the EUR/USD.

Voting publics in the U.S and elsewhere are showing signs of voting for more conservative leadership. Germany has seen lackluster economic results manifest for a long time and their public is certainly yearning for more GDP growth and less inflation. It is no secret that in nations such as Canada, Australia and countries in Europe that conservative voices are becoming louder when unbiased polling is conducted. Prime Minister Trudeau of Canada has already admitted his defeat via his decision to step aside.

The United States saw a very strong election result for Donald Trump and Republicans in November, and it would not be a surprise to see a similarly strong outcome for conservative candidates in Germany as results are announced late tonight and tomorrow. Voters seem to be expressing frustrations they feel they are not allowed to say out loud in polite circles. The results from Germany will likely mirror this consideration.

So what will the EUR/USD do if the voters in Germany elect a vastly more conservative government? Early results will be choppy, but a logical wager is to believe financial institutions will begin to look at the EUR/USD with a more bullish attitude, this if they believe a government is going to take power that is business friendly. Day traders should not bet blindly on EUR/USD upside. But looking for the 1.05000 level and higher to become a focal point for buyers is a legitimate outlook near-term.

The selloff in the EUR/USD this past Friday may have had a bit to do with financial institutions believing the upside had been overdone before the results of the German election were known. But that is likely a false narrative.

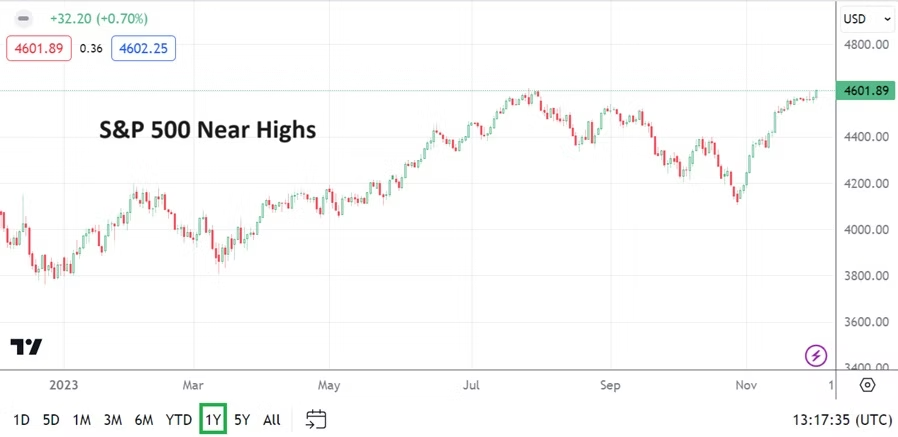

There is a better chance the sudden selloff in the EUR/USD on Friday which developed and saw fast velocity downwards, happened because Wall Street equities produced declines on its open and the selling continued going into the weekend. Forex is never easy, many complexities exists for speculators to consider.

The results from the German Federal Election today will influence major currency pairs this coming week and the EUR/USD will be centerstage. If Wall Street begins to show signs of stability this will also help the EUR/USD. Day traders should be extremely careful early tomorrow as financial institutions start participating and react to the results from Germany.