Trading with Tomorrow in Mind as Risk Adverse Emotions Grow

Speculators by nature have to be optimistic about perceived outcomes. As risk adverse conditions hit global markets both financial institutions and traders are still engaged with tomorrow and the days ahead. Tomorrow is definitely going to happen. Calmer heads at some point will prevail. Current nervousness will subside. Thus far today relatively tranquil trading has been seen as prices remain within known technical equilibriums.

Gold Six Month Chart as of 2nd October 2024

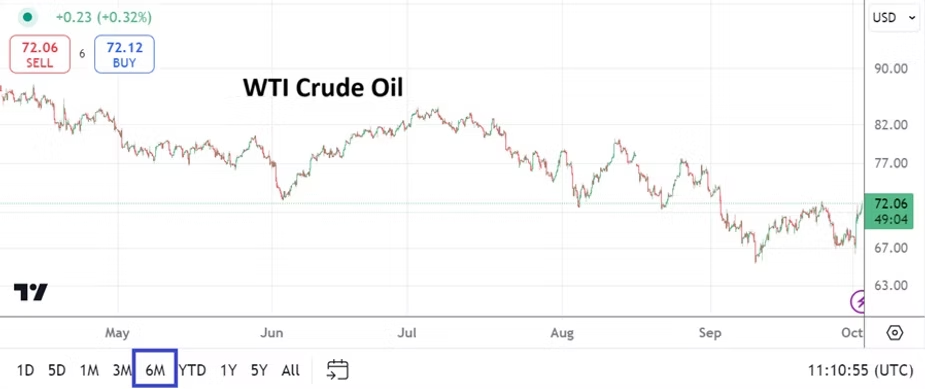

While people contemplate the tensions from the Middle East the markets remain quite active. Gold as of this writing is near 2,650.00 USD per ounce. And WTI Crude Oil is trading around 72.00 USD per barrel. The value of Gold has been in a strong bullish trend the past year it could be argued, and WTI has been bearish throughout the mid-term.

WTI Crude Oil Six Month Chart as of 2nd October 2024

While saber rattling in the Middle East threatens to escalate, financial institutions are still gearing towards Friday’s Non-Farm Employment Change numbers. The data is expected to come within the grasp of last month’s hiring figures, but Average Hourly Earnings are expected to drop slightly. If the jobs numbers come in weaker this could spark USD centric weakness. That is if risk adverse trading moderates.

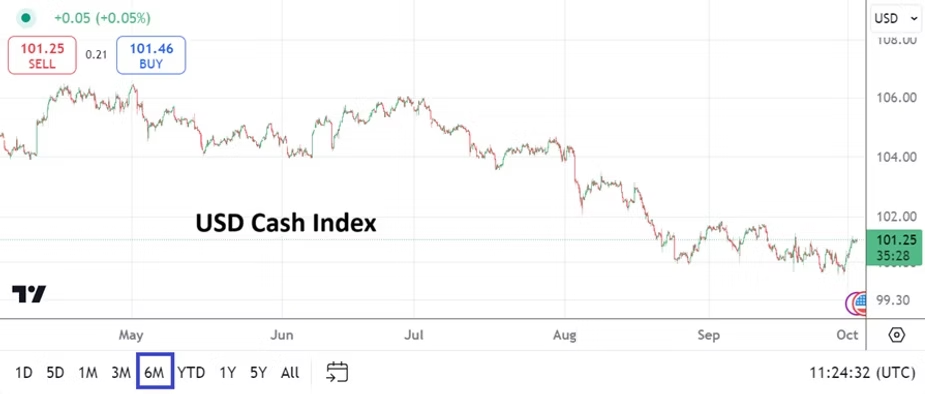

USD Cash Index Six Month Chart as of 2nd October 2024

The past day has seen heightened nervousness, but it must be pointed out that value realms are still maintaining rather optimistic outlooks regarding the Fed’s ability to remain dovish. What needs to happen now for the markets to turn tranquil are jobs reports on Friday to confirm outlooks, and for Israel and Iran not to engage in an all encompassing war. A look at the USD Cash Index shows a slight uptick, but it is definitely maintaining lower realms.

While risk adverse trading can be blamed for the results seen in the markets the past couple of days, it should also be pointed out that cautious perspectives are being practiced by some financial institutions who simply may believe values via USD centric weakness may have been overdone in the near-term. While many financial houses certainly believe the USD is bound to be weaker mid-term because of the Federal Reserve, do not mistake their short-term trading with their long-term outlooks.

Many people believe banks do not bet on the direction of Forex. But a look at the cash forward trading that banks do for their commercial clients demonstrates banks have skin in the game, and are trying to protect themselves via a multitude of layered hedging which still amounts to speculation.

Leaving us with the final point, day traders need to protect their accounts too by understanding market conditions. Volatility in the near-term is almost a certainty. Speculators should be careful not to get caught up in the amplitude of fear that is being generated by media sources looking to gain viewers. Betting blindly on outcomes because of fear will lead to costly mistakes. Eliminate the noise.

Optimistic attitudes frequently win. Day traders need to remain patient, keep an eye on developing news from the Middle East, but understand that U.S economic data results still provide the most navigable winds. Impetus will move gold, WTI Crude Oil, the USD, and equity indices via dynamic thrusts over the next few days.

Fed Plays Catch Up and Sets a Calm Table for Day Traders

The Fed essentially played a game of catch up on Wednesday when they cut the Federal Funds Rate by 0.50%. The interest rate cut was bigger than AMT expected because of the Fed’s rather cautious stance the past handful of years. However, the move by the FOMC was certainly justified and welcomed, and now financial institutions have been given what most thought was bound to happen, a roadmap to at least a 0.75% Federal Funds Rate cut over the next six months. Longer term many believe the Fed will continue to be aggressively dovish if U.S economic conditions cooperate.

USD/JPY One Year Chart on the 20th of Sept. 2024

Traders certainly seem to be leaning into the notion another 0.25% will be trimmed by the Federal Reserve in November. And this sets the table for day traders to now face potentially calmer market conditions that react solely to economic data, geopolitical events and the occasional flashes of news. The U.S presidential election will certainly be a big event on the 5th of November. Long-term investors are likely feeling rather tranquil and have not been surprised. Behavioral sentiment over the next month should be easier to gauge.

USD Cash Index One Year Chart on the 20th of Sept. 2024

So what happens near-term? The Bank of Japan today, like the BoE yesterday, stood in place. The USD/JPY is trading near 142.300 as of this writing. The GBP/USD is near 1.32890. Gold is hovering near 2,600.00 and WTI Crude Oil is approximately 72.00 USD. Perhaps short-term traders should keep one eye on the Middle East this weekend, but for the moment it doesn’t appear a major escalation is about to ignite in the region. Yes, there is saber rattling, but composure may actually prevail. Those looking for a sudden emergence of a strong USD trend may find that headwinds keep the greenback within the lower realms of the USD Cash Index.

Gold One Year Chart on the 20th of Sept. 2024

Next week’s U.S GDP numbers on Thursday the 26th, and the Core PCE Price Index results on Friday the 27th will get plenty of attention. What the Fed and financial institutions would like to see are stable economic numbers which do not spark fears of a recession. The almighty ‘soft landing’ being pursued by the Federal Reserve is likely being hoped for too by financial institutions via their mid-term outlooks.

The Federal Reserve is supposed to be an independent entity not associated with the Executive Branch of the U.S government regarding oversight. There has been some bantering about the potential that the Fed cut by 0.50% before the U.S elections and Powell proclaimed the U.S economy is doing well to help the Democrats, but this is unlikely. Conspiracy thinking aside, the broad markets are now going to be a barometer regarding economic outlook based on data such as growth, jobs numbers and inflation; clarity regarding a more dovish Fed has been delivered in many respects, data has to justify their decision moving forward.

Day traders may have the ability to follow their technical charts and gather behavioral sentiment perspectives over the next month serenely by watching barometers like gold and U.S Treasury yields. As the U.S election draws closer financial institutions may start to position for potential outcomes, but with polls indicating a tight race currently they would be foolish to bet on one particular outcome. Meaning the broad markets including equity indices, Forex, U.S Treasury yields and even commodities may be moving within fairly priced equilibriums for the moment.

As the Dow 30 and S&P 500 move within record heights, the Nasdaq 100 is slightly below its all-time highs. Yet, it should be remembered the Nasdaq 100 still has done remarkably well the past year and although not at an apex level has the potential to scale upwards quickly. Optimism for the moment seems to be driving the financial markets and day traders should keep this in mind. However, speculators should remember risk management is essential, not over leveraging ideal, and keeping realistic price targets remains always important.

Nervous? Central Banks Cautious, FX and Asset Equilibrium

Sometimes when looking for ideas regarding a risk analysis article it is difficult to find a timely subject. Exaggeration is often used to grab attention. This week and next will not be one of those times. Equities, Forex and commodities have produced nervous results since last Monday. The broad markets appear to be in search of equilibrium, but price velocity while higher than normal hasn’t produced a volcanic surge of pain. Financial institutions were presented less than inspiring jobs data this past Friday and day traders hopefully had their risk management working. Everyone will need to be paying attention this week too.

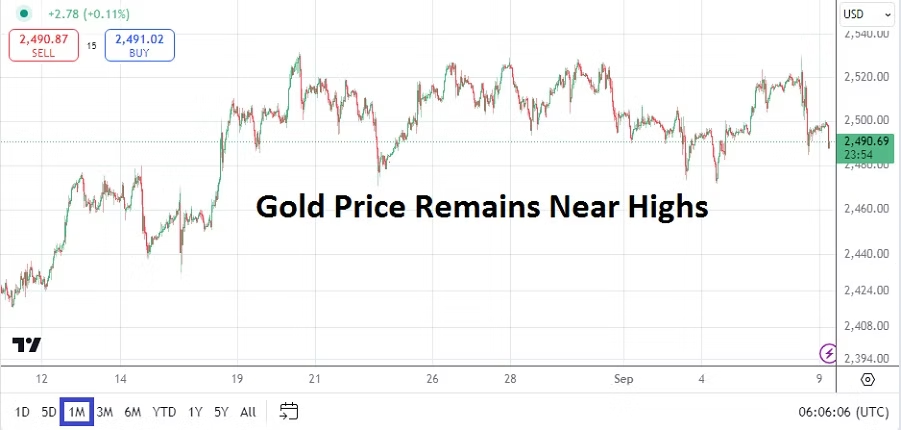

Gold One Month Chart as of 9th Sept. 2024

Gold has hovered around the 2,500.00 level and while it certainly is a short-term speculative asset for day traders, the precious metal also serves as distinct barometer of behavioral sentiment and long-term guidance regarding inflation. Recent economic data has created concerns in financial institutions about the potential for a stronger than anticipated U.S downturn. The volatility and sell off in equity indices last week is a clear sign investors would like the Federal Reserve to be more aggressively dovish.

This coming week is packed with a variety of risk events which will keep all market participants engaged. Long-term investors may feel calm as they rely on their outlooks which extend over a handful of years, but anyone who needs a firm grasp on short and mid-term viewpoints might not be comfortable. It is important not to cry wolf too often, but based on the trading results seen the past week it is worthwhile to point to the turbulent outcomes and issue a warning that more volatility could develop.

Nasdaq 100 One Month Chart as of 9th of Sept. 2024

Some analysts may apply the thought that what we have seen was profit taking, and this can certainly be debated. The coming two weeks have plenty of noteworthy events on the calendar. Besides the listed risk highlights noted below, the Fed will release its FOMC Statement on Wednesday the 18th, the BoE will follow on the 19th and not to be outdone the Bank of Japan will step onto center stage on Friday the 20th of September.

While long-term investors likely believe all variables will return to known price realms and that central banks sooner or later will fall into their proper places regarding monetary policy, day traders who are gambling on short-term momentum must try to figure out where behavioral sentiment is leaning. One of the ways speculators without deep pockets can put the odds in their favor concerning potential profits, is to make sure they are practicing rock solid risk management and not stepping into Forex trades, equity indices via CFDs wagers, and commodities bets when they are displaying rough conditions without being prepared.

Monday, 9th of Sept., China Consumer and Producer Price Index – the inflation reports from China both came in below their estimates earlier today. While some may believe that less inflation than predicted is a good thing, it isn’t when the economy is suffering from deflationary pressures. Lackluster spending from consumers in China continues to highlight negative sentiment about prospects for growth. The USD/CNY is near the 7.1125 ratio as of this writing.

Tuesday, 10th of Sept., U.S Presidential Debate – while not an economic data event, investors might want to pay attention to the answers given by Vice President Kamala Harris and former President Donald Trump. The race for the White House appears to be close according to various polling. It could prove interesting for financial institutions if Harris is questioned about her ideas regarding taxing unrealized capital gains.

USD Cash Index One Month Chart as of 9th Sept. 2024

Wednesday, 11th of Sept., U.S Consumer Price Index data – the inflation reports will certainly get the attention of financial institutions. If the annual CPI report comes in weaker than the previous outcome, this could spark more USD centric weakness in Forex. All asset classes will react to the inflation numbers because they are likely to play a major part in the Fed’s FOMC decision in one week’s time. The USD Cash Index is still lingering near lows, but for it too resume a more bearish trajectory, financial institutions will need to believe the Federal Reserve is going to become increasingly dovish.

EUR/USD One Month Chart as of 9th Sept. 2024

Thursday, 12th of Sept., European Central Bank Main Refinancing Rate – The ECB is definitely going to cut its prime borrowing interest rate, the question is how much of a haircut they are going to provide. A 0.25% cut has certainly been traded into the EUR/USD, but many financial institutions believe there is a possibility to see a 0.50% basis cut. Can the ECB and Christine Legarde be aggressive? The European Union remains under recessionary pressures and inflation data is starting to show signs of erosion. The amount of the interest rate cut from the ECB will also be a telltale sign regarding what will happen via the Federal Reserve on the 18th of September. The EUR/USD will react to the European Central Bank’s decision, and global assets in far off places may react too because behavioral sentiment among investors may shift according to the rhetoric provided. Prediction: The ECB will stay cautious and cut by 0.25%, while saying a November rate cut is likely if economic data remains under pressure. Having said the above, the ECB should cut by 0.50% this Thursday, if they do not – financial institutions will not be pleased unless ECB President Legarde sounds very dovish during her Press Conference.

Thursday, 12th of Sept., U.S Producer Price Index – more inflation data from the U.S will provide investors an other opportunity to glance into the Fed’s looking glass. But if these PPI numbers meet or are near the anticipated results, financial institutions may be reacting to the ECB’s rate decision more because they might believe it is a better clue regarding the Fed’s Federal Funds Rate decision which will come in a handful of days.

USD/JPY One Month Chart as of 9th Sept. 2024

Friday, 13th of Sept., Japan Revised Industrial Production – this number may not get much attention, but because the Bank of Japan will release its Policy Rate on the 20th, the outcome could impact existing sentiment in the USD/JPY. The Japanese Yen has continued its bearish trajectory and traders who are wagering on more downside should not bet blindly on selling positions because intraday trading remains very choppy. The USD/JPY is now touching values last seen in a sustained manner in early January of 2024, lower values were seen in December 2023, and lower ratios that traversed the 138.000 realm and proved choppy occurred in the spring of 2023.

Saturday, 14th of Sept., China New Home Prices, Retail Sales, Industrial Production – this parade of data from the nation will be important. Foreign investors remain concerned about China’s economic prospects. The deflationary winds that have been blowing in the Asian giant have been well documented. The results from these three reports are expected to be lackluster.

USD/INR: Consolidation Might Come to an Abrupt Conclusion

The USD/INR is trading near the 81.9750 ratio as of this writing and its price action since the 13th of July has produced a tight price range. On the 12th of July the USD/INR was trading around the 82.3000 region, this after being able to incrementally decline when a high of nearly 82.7900 was reached on the 6th of July.

Prior to the apex value of July, the USD/INR had traded in a rather consolidated mode from the middle of June until the first few days of July, essentially within a price realm the currency pair now lingers. Speculators must constantly fight the slightest of reversals if they are using too much leverage, but the USD/INR over the mid-term has produced interesting behavioral sentiment and this can be seen on technical charts.

While day traders may believe the current price ratios will hold and the potential interest rate hike from the U.S Federal Reserve has been digested into the USD/INR for this coming Wednesday, they might want to reconsider their thinking. No, the world is not coming to an end, Forex has dealt with U.S central bank decisions before and experienced traders understand the sudden potential of the USD/INR changing direction. The rather tight price range of the USD/INR could vanish in the coming days if the Federal Reserve begins to change their tone within the FOMC Statements.

USD/INR One Month Chart as of 24th July 2023

U.S Federal Reserve is Likely to Raise the Federal Funds Rate but Perhaps Shouldn’t

The USD/INR may not get hit too hard when the U.S Federal Reserve delivers the anticipated 0.25% addition to the Federal Funds Rate. However, the FOMC Statement which talks about the Fed’s outlook might cause a change to what have been calm seas recently in the USD/INR. Recent U.S economic data has been rather troubling, but inflation does actually seem to be creeping lower. The Fed has been pretty adamant in their recent ‘whispering’ about raising interest rates in July, and the potential of raising again later this year.

Time for the U.S Federal Reserve to Start Sounding Dovish

Yet, recent data suggests the Fed should likely not even raise rates on the 26th of July and continue its pause. But having expressed plenty of verbiage on the subject, the Fed may not want to surprise financial institutions and may have to raise, even if they do not really have to this week. And here is where it gets interesting – the FOMC Statement may have to express this notion of becoming more dovish. Think of this potential hike to the Federal Funds Rate this week as the last dose of medicine for a patient who already feels better, the doctor (the Fed) is insisting that to make sure the ‘sick’ is cured another teaspoon consisting of an interest rate hike is necessary.

If the FOMC Statement sounds more dovish than expected the USD/INR might start to see selling ignite and a downturn generate. There are no guarantees and certainly the Fed’s actions this coming Wednesday are not known. Yet, if the Fed hints that it will not raise interest rates over the mid-term and wants to see if inflation continues to lower that it may consider the potential of no more hikes, the USD will start to get weaker across the board. In other words, this last dose of medicine from the Fed may give them the feeling to tell the patient (U.S economy) that they no longer need to visit the doctor’s office for a while.

Other central banks are watching too. Inflation in Europe and elsewhere remains high. The complications of weaker domestic currencies against the USD have hit many economies including India where inflation has been rather strong. If the Fed can now start to become less aggressive, the effect will be quick and start helping the USD/INR trade lower if healthy economic mechanics allow this to happen.

Support levels for the USD/INR near 81.8000 to 81.7500 should be watched, if these levels begin to see challenges and sustained prices remain nearby, the USD/INR may be signaling that another downturn is about to happen. If the U.S Fed delivers a cautious, but more optimistic FOMC Statement this coming Wednesday, the USD/INR may deliver a new cycle of selling.

Anticipated Federal Reserve Shop Talk to be Delivered Today

For what it’s worth, here is my prediction regarding what the Federal Reserve will do today. The Federal Funds Rate will remain unchanged in my opinion. The FOMC Statement may show that the vote actually was debated and not unanimous. The statement is likely to warn that inflation remains stubborn and potentially problematic, meaning the Federal Reserve continues to believe it may have to raise the Federal Funds Rate over the mid-term and again before the end of 2023.

The Forex market has seen the USD get weaker against many major currencies since late May. While financial institutions have seemingly positioned for no increase from the Federal Reserve today, this move has also likely been priced into Forex. Day traders need to understand institutional traders will not be betting on what took place the last three weeks, but are trying to anticipate what will happen into early July and beyond regarding their Forex positions.

GBP/USD One Month Chart as of the 14th June 2023

Many financial institutions may still be betting the Fed will remain more dovish than the U.S central bank wants to admit, but this is a dangerous perception and could prove costly. Financial institutions are concerned about the Fed because they know the central bank has painted itself into a corner it may not be able to maneuver freely within. The battle to conquer inflation while trying to fuel economic growth is not an easy one. Mixed sentiment abounds regarding the U.S economy depending on who is asked.

Talk of a soft landing and a small recession continues to be heard, this while some analysts warn about a hard drop and darker days ahead. Folks, it is all about timelines and their interpretations, experts warning about brighter or darker days ahead have a tendency to be vague regarding exact moments in time. Everyone has an opinion, and people often have more than one.

In my opinion – my one opinion, the Fed is likely to say that it is not going to raise rates today, but may have to do so in the mid-term. If these were normal times and economic conditions were not suffering from huge spending running amok in Washington and the corporate banking sector wasn’t fragile, the Fed may actually have raised the Federal Funds Rate today to continue to battle inflation deliberately. However, a pause for the moment seems like the logical choice, this while ‘hoping’ inflation continues to diminish. And hope is a key word here. Everyone seems to be hoping. The question financial houses and traders need to decide after the FOMC Statement takes place today is how seriously do they consider the Fed’s remarks.

If they believe the Fed will have to continue to remain neutral regarding its mid and long-term interest rate policy, the USD may soften and incremental selling might be demonstrated. Human instinct tends to be optimistic, which means financial institutions and maybe even the Fed wants to believe inflation will ebb lower. If this happens the USD would weaken further. However, the Fed may have to sound more aggressive than people want, but that would damper the mood of financial institutions – so look for optimistic interpretations to abound with rose colored glasses, even if they are wrong in the long-term.

Gold One Month Chart as of the 14th June 2023

For evidence of outside barometers, traders may want to look at Gold which has essentially traded between 1940.00 and 1975.00 with a few outliers since the last week in May. The price of Gold has seemingly situated within a consolidated framework the past few weeks. The precious metal may produce a strong move if the Fed shows more dovish behavior today, particularly if financial institutions show more optimism via behavioral sentiment in Forex – meaning if a weaker USD trend continues momentarily Gold could traverse higher.

My prediction and $1.00 USD may get you on a bus. As always caution will be needed if you are trading immediately before and after the U.S Federal Reserve’s rate decision. I advise using a seat belt today consisting of entry price, stop loss and take profit orders via solid risk management, but then again these cautious attitudes should always be practiced by day traders.