December Cheer, Full Volume, Considerations for Coming Week

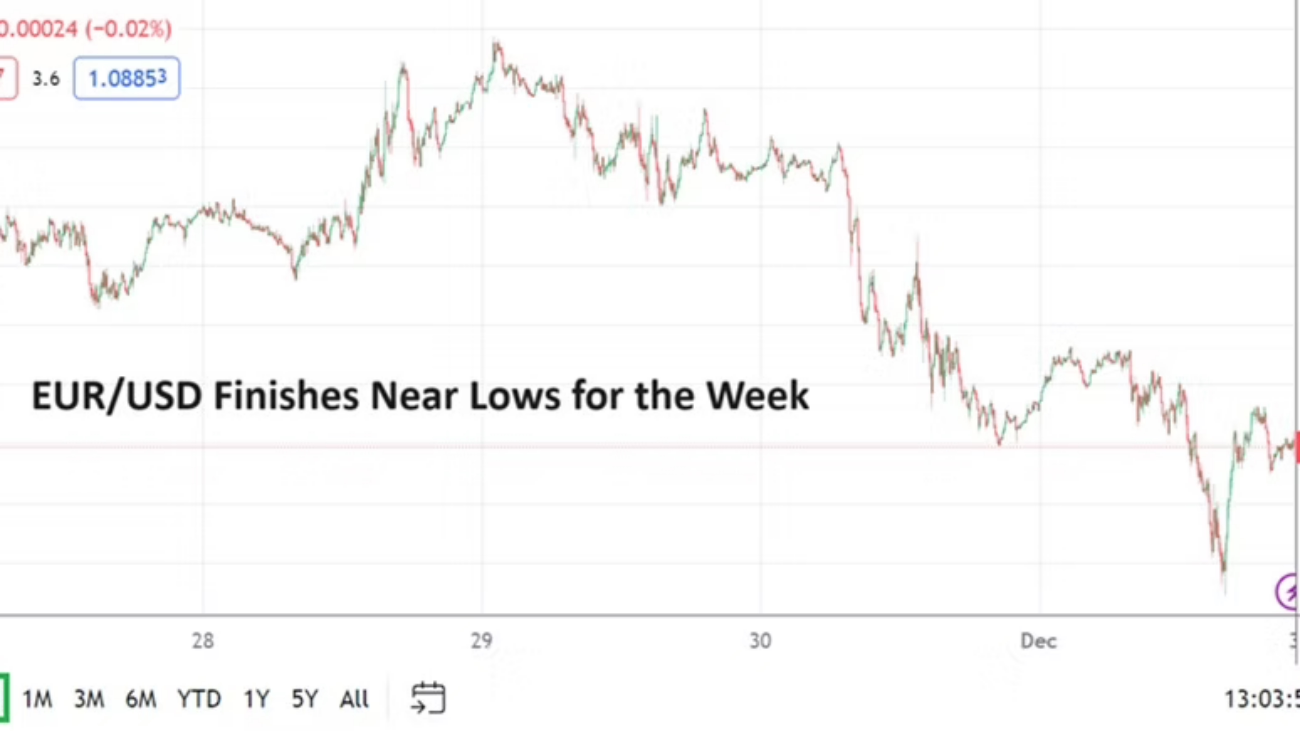

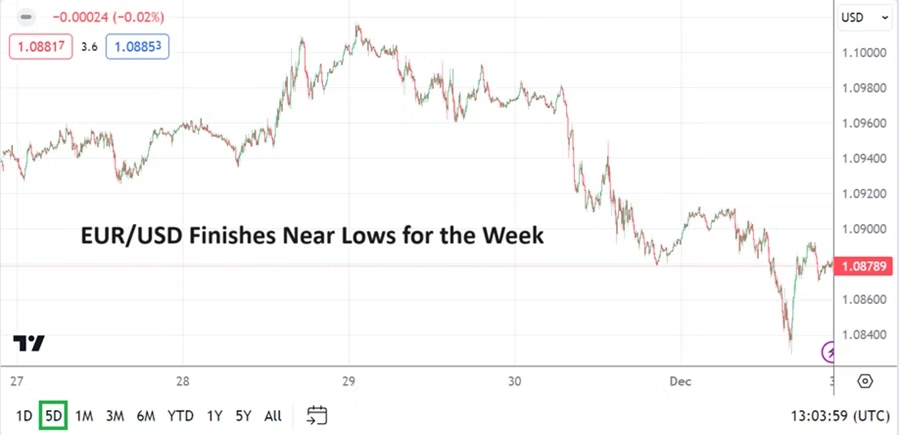

The EUR/USD finished the past week of trading below its starting point essentially closing this Friday around the 1.08790 mark. While the slight downturn may have hurt bullish day traders who kept on looking for higher ground in the short-term, the EUR/USD did trade above the 1.10000 on late Tuesday and held its ground briefly on Wednesday before starting to trend lower. A depth of nearly 1.08310 was momentarily challenged on Friday with solid price velocity, but the EUR/USD did exhibit some buying before going into the weekend.

Speculators who were looking for a higher finish for the week from the EUR/USD may have been disappointed, but the end of the trend upwards may not be finished. U.S Fed Chairman Jerome Powell sounded optimistic on Friday regarding Fed policy and mentioned a ‘soft landing’ and indicated interest rates at their current level will still need a bit of time to have their full effect. U.S growth numbers via the Gross Domestic Product came in stronger than expected on the 29th of November, but inflation data continues to show a slight erosion.

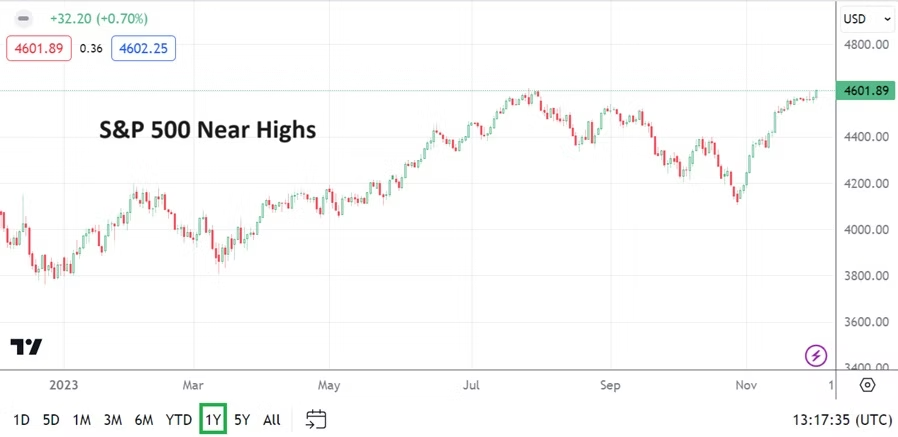

This puts the U.S Federal Reserve in position to actually sound rather neutral when the FOMC Meetings conclude in a week and a half. And if global events do not cause any sudden alarms to ring, it appears risk appetite is within a rather optimistic state. U.S equity indices continued to roll along merrily and the 3 big indexes are challenging highs. The S&P 500 and Nasdaq Composite are challenging July values, and the Dow Jones 30 is trading at ratios last seen in January of 2022.

While U.S Treasury yields have also continued to erode and are near mid-term lows, the USD/JPY continued to create a bearish trend for the week and is trading at values last seen in the second week of September. The GBP/USD finished the week within sight of highs attained on Tuesday and Wednesday, this as the currency pair also trades near values last seen in late August and early September. The EUR/USD is the outlier among the three major currency pairs and speculators may look at the EUR as potentially being in oversold territory as the week gets set to begin. Risk management as always is essential for wagering on Forex.

The next two and a half weeks of trading will see full volumes, this before holiday trading starts to hit the broad marketplace. The upward moves in U.S equity indices may be seen as overdone by many analysts, but the trend has been strong and trying to step in front of the ‘optimism’ within the indexes may prove expensive in the coming days and weeks. Day traders should make sure conservative leverage is being used if they are attempting to climb aboard the moving train.

Some analysts are pointing out correctly, that if it weren’t for a few ‘workhorse’ corporations in the U.S equity indices, declines would have been seen. But day traders who are wagering on CFDs via their brokers and financial institutions investing in the three major stock indices are likely enjoying their profitable returns.

Monday, the 4th of December, E.U Sentix Investor Confidence – the reading is expected to come in with a negative result, but slightly better than last month’s outcome of minus -18.6. About a hour and a half before this European survey, German Trade Balance numbers will be released. The EUR/USD may be affected by this data, but the currency pair is likely moving within the shadows of behavioral sentiment which is USD centric. Europe is struggling with recessionary conditions, but it is outlook which drives the marketplace. If the EUR/USD can find durable support it may prove that its bullish trend has not come to an end.

Tuesday, the 5th of December, U.S ISM Services Purchasing Managers Index – an improvement is expected compared to last month’s outcome. Recent data from the manufacturing sector came in less than expected, thus the services sector will be watched closely, but as long as the result is around the expectation this will not hinder broad market sentiment. Meaning the report could be a non-factor.

Wednesday, the 6th of December, Canada BoC Overnight Rate – traders will be keen to see what line of rhetoric is taken within the Rate Statement from the Bank of Canada. No change to borrowing costs are expected. The rate is anticipated to remain at 5.00%. The economy of Canada has been struggling as recessionary clouds are shadowing, but recent GDP data was slightly better than expected and inflation has shown signs of weakening. The USD/CAD went into this weekend near its lows and in sight of values seen in late September.

Thursday, the 7th of December, China Trade Balance – economic numbers via the manufacturing sector last week came in below expectations. The lackluster China data may be a factor in the weaker WTI Crude Oil prices, but perhaps that is only speculative. Some investors participating in China are worried about outlook over the mid-term. Analysts will comment on the Trade Balance numbers, but traders should make sure they separate the ‘noise’ which may be delivered from biased perspectives depending on ‘world view’ compared to actual outcomes and genuine insights.

Friday, the 8th of December, U.S Non-Farm Employment Change and Average Hourly Earnings – the jobs numbers will be looked at attentively by market participants. The data will be correlated to existing behavioral sentiment and risk appetite that has sustained a weaker USD, higher U.S equity indices, lower yields on U.S Treasuries and the high price of gold. If the jobs data comes in around expectations that will likely be enough for investors to remain calm and look forward to the 13th of December, this is when the U.S Federal Reserve will release its FOMC Statement – which may keep risk appetite strong.